Yes Bank Business Model Canvas

Yes Bank Business Model Canvas: Strategic Blueprint for Investors & Executives

Unlock the full strategic blueprint behind Yes Bank’s business model—this concise Business Model Canvas exposes how the bank delivers customer value, scales revenue streams, and navigates regulatory and competitive challenges; ideal for investors, consultants, and executives seeking actionable, company-specific insights to guide strategy and investment decisions.

Partnerships

Strategic Fintech Collaborations

Yes Bank partners with 40+ fintechs, integrating payment rails and niche lending stacks that drove a 28% YoY rise in digital-originated loans to INR 6,200 crore in FY2024; these alliances enable BNPL, API payments, and SME underwriting plug-ins that cut customer onboarding time to under 24 hours. By end-2025, fintech tie-ups are central to retaining market share amid India's digital credit growth forecast of 20% CAGR (2023–2026).

Institutional Investors and Promoters

Yes Bank depends on major backers—State Bank of India (SBI) and global PE firms Carlyle and Advent International—whose capital injections helped restore CET1 capital to about 12.5% and total capital adequacy to ~16.0% by FY2024, giving regulatory comfort and funding headroom. Their governance oversight and committed support are essential for market confidence and to finance strategic expansion, including targeted credit growth of 12–15% annually.

Technology and Infrastructure Providers

Partnerships with cloud providers and cybersecurity firms give Yes Bank scalable hosting and 99.95%+ uptime for mobile/net banking; in 2024 the bank reported 40% digital transaction growth and cut outage incidents by 65% after cloud migration. These vendors lower operational-risk metrics and support compliance with RBI and ISO 27001 controls, reducing expected loss from cyber incidents by an estimated 30%.

Bancassurance and Third-party Distributors

Yes Bank partners with top insurers and mutual fund houses to distribute life, health, and investment products, generating fee income—reported bancassurance fees of INR 320 crore in FY2024—while expanding customer lifetime value through holistic financial planning tools.

These third-party channels drive cross-sell: 48% of retail CASA customers hold at least one third-party product, boosting share-of-wallet and engagement.

- INR 320 crore bancassurance fees (FY2024)

- 48% retail CASA customers hold a third-party product

- Fee income diversifies net interest margin pressure

Corporate and MSME Ecosystems

Yes Bank partners with industry bodies and trade associations to serve MSMEs, enabling sector-specific credit programs and supply-chain finance; by 2025 the bank reported ~INR 18,500 crore in MSME loans and a 24% YoY growth in supply-chain financing (FY2024-25).

- Alliances with trade bodies for tailored credit

- Supply-chain finance grew 24% YoY (FY24-25)

- MSME book ~INR 18,500 crore (2025)

- Integration with corporate value chains boosts deal flow

Yes Bank's fintech push fuels INR6,200cr digital loans, CET1 ~12.5% and 24% SCF growth

Yes Bank's 40+ fintech tie-ups and insurer/MF distributors drove digital-originated loans to INR 6,200 crore (FY2024), bancassurance fees INR 320 crore (FY2024), MSME book ~INR 18,500 crore (2025) and 24% YoY supply-chain finance growth (FY24-25); SBI, Carlyle, Advent support restored CET1 ~12.5% and total CAR ~16.0% (FY2024).

| Metric | Value |

|---|---|

| Digital loans | INR 6,200 cr (FY2024) |

| Bancassurance fees | INR 320 cr (FY2024) |

| MSME loans | ~INR 18,500 cr (2025) |

| Supply-chain finance growth | 24% YoY (FY24-25) |

| CET1 | ~12.5% (FY2024) |

| Total CAR | ~16.0% (FY2024) |

What is included in the product

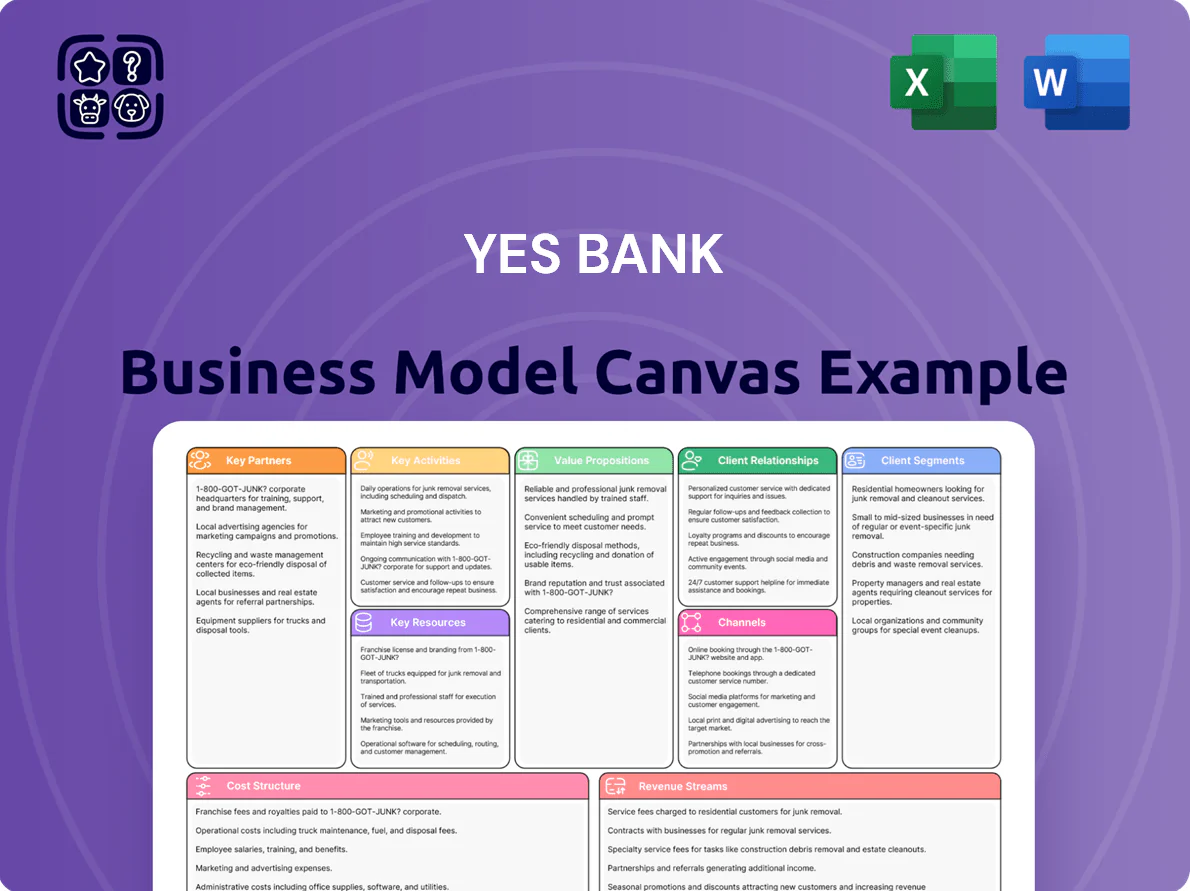

A comprehensive, pre-written Business Model Canvas tailored to Yes Bank’s strategy, covering customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams with real-world operational insights and competitive analysis to support presentations, funding discussions, and strategic decision-making.

High-level snapshot of Yes Bank’s business model with editable cells to quickly identify core banking components, ideal for boardrooms, team collaboration, and fast executive summaries.

Activities

Lending and Credit Management

The bank disburses and manages loans across retail, MSME and corporate segments, using layered credit appraisal and monthly portfolio reviews; gross advances were Rs 1.12 lakh crore as of Sep 30, 2025, with retail at ~42% and MSME at ~18%.

Proactive monitoring targets GNPA below 2.5% and PCR (provision coverage ratio) above 75% by late 2025 to protect net interest margin, with targeted loan mix shifts to sustain NIM near 3.4%.

Digital Banking Operations

Yes Bank continuously develops and maintains digital platforms—mobile app and UPI—handling 28% of retail transactions digitally in FY2024 and 42m UPI transactions monthly (2024), focusing on faster onboarding, smoother payments, and reduced processing times.

Operations prioritize UX improvements and strong cybersecurity: 24/7 monitoring, ISO 27001 controls, and a 35% drop in fraud losses year-on-year to FY2024, supporting a digital-first strategy to win and keep tech-savvy customers.

Risk Management and Compliance

Yes Bank allocates significant staff and capital to meet Reserve Bank of India rules, running quarterly internal audits and annual stress tests; regulatory spend rose to an estimated ₹1.2–1.5 billion in FY2024 for compliance programs. The bank enforces AML (anti-money laundering) frameworks and credit/market risk controls to protect depositors and preserve its banking licence, keeping CET1 capital at or above regulatory buffers—12.5% reported in Sep 2024.

Customer Acquisition and Marketing

Yes Bank runs targeted marketing campaigns using data analytics to acquire deposits and loan customers, aiming to raise CASA (current and savings accounts) which was 23.8% in FY2024 to cut funding costs; campaigns focus on salaried millennials and SME segments with personalized digital offers and 20–30% higher conversion in pilot cohorts.

- CASA 23.8% (FY2024)

- Target segments: salaried millennials, SMEs

- Data-driven personalization lifts conversions 20–30%

- Goal: raise CASA to lower cost of funds

Wealth Management and Advisory

Wealth management and advisory is a core Yes Bank activity, serving HNWIs and corporates with portfolio management, market research, and asset-allocation strategies while distributing third-party products; fee income from wealth grew bank-wide, contributing to non-interest revenue that rose ~18% YoY to ₹3,450 crore in FY2024.

- HNW/Corp portfolio management

- Market research-led asset allocation

- Third-party product distribution

- Drives fee-based revenue; non-interest income ₹3,450 crore FY2024 (+18% YoY)

Yes Bank: ₹1.12Lcr advances, 42% retail, targeting GNPA <2.5% & PCR >75% by late‑2025

Yes Bank originates and services loans across retail, MSME and corporate; gross advances Rs 1.12 lakh crore (Sep 30, 2025), retail ~42%, MSME ~18%, targeting GNPA <2.5% and PCR >75% by late 2025 to protect NIM ~3.4%.

It runs digital channels (28% retail digital FY2024, 42m UPI/month 2024), strong cybersecurity (ISO 27001, 24/7), compliance spend ₹1.2–1.5bn FY2024, and fee income drove non-interest revenue ₹3,450cr (+18% YoY FY2024).

| Metric | Value |

|---|---|

| Gross advances | ₹1.12L cr (Sep 30, 2025) |

| Retail share | ~42% |

| MSME share | ~18% |

| GNPA target | <2.5% (late 2025) |

| PCR target | >75% (late 2025) |

| NIM | ~3.4% |

| Digital retail txn | 28% (FY2024) |

| UPI/month | 42m (2024) |

| Compliance spend | ₹1.2–1.5bn (FY2024) |

| Non-int income | ₹3,450cr (+18% YoY FY2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you see is the actual Yes Bank Business Model Canvas—not a mockup—and it matches the exact document you’ll receive after purchase; upon ordering, you’ll get the full, editable file in Word and Excel formats, structured and formatted exactly as shown.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Yes Bank Business Model Canvas: Strategic Blueprint for Investors & Executives

Unlock the full strategic blueprint behind Yes Bank’s business model—this concise Business Model Canvas exposes how the bank delivers customer value, scales revenue streams, and navigates regulatory and competitive challenges; ideal for investors, consultants, and executives seeking actionable, company-specific insights to guide strategy and investment decisions.

Partnerships

Strategic Fintech Collaborations

Yes Bank partners with 40+ fintechs, integrating payment rails and niche lending stacks that drove a 28% YoY rise in digital-originated loans to INR 6,200 crore in FY2024; these alliances enable BNPL, API payments, and SME underwriting plug-ins that cut customer onboarding time to under 24 hours. By end-2025, fintech tie-ups are central to retaining market share amid India's digital credit growth forecast of 20% CAGR (2023–2026).

Institutional Investors and Promoters

Yes Bank depends on major backers—State Bank of India (SBI) and global PE firms Carlyle and Advent International—whose capital injections helped restore CET1 capital to about 12.5% and total capital adequacy to ~16.0% by FY2024, giving regulatory comfort and funding headroom. Their governance oversight and committed support are essential for market confidence and to finance strategic expansion, including targeted credit growth of 12–15% annually.

Technology and Infrastructure Providers

Partnerships with cloud providers and cybersecurity firms give Yes Bank scalable hosting and 99.95%+ uptime for mobile/net banking; in 2024 the bank reported 40% digital transaction growth and cut outage incidents by 65% after cloud migration. These vendors lower operational-risk metrics and support compliance with RBI and ISO 27001 controls, reducing expected loss from cyber incidents by an estimated 30%.

Bancassurance and Third-party Distributors

Yes Bank partners with top insurers and mutual fund houses to distribute life, health, and investment products, generating fee income—reported bancassurance fees of INR 320 crore in FY2024—while expanding customer lifetime value through holistic financial planning tools.

These third-party channels drive cross-sell: 48% of retail CASA customers hold at least one third-party product, boosting share-of-wallet and engagement.

- INR 320 crore bancassurance fees (FY2024)

- 48% retail CASA customers hold a third-party product

- Fee income diversifies net interest margin pressure

Corporate and MSME Ecosystems

Yes Bank partners with industry bodies and trade associations to serve MSMEs, enabling sector-specific credit programs and supply-chain finance; by 2025 the bank reported ~INR 18,500 crore in MSME loans and a 24% YoY growth in supply-chain financing (FY2024-25).

- Alliances with trade bodies for tailored credit

- Supply-chain finance grew 24% YoY (FY24-25)

- MSME book ~INR 18,500 crore (2025)

- Integration with corporate value chains boosts deal flow

Yes Bank's fintech push fuels INR6,200cr digital loans, CET1 ~12.5% and 24% SCF growth

Yes Bank's 40+ fintech tie-ups and insurer/MF distributors drove digital-originated loans to INR 6,200 crore (FY2024), bancassurance fees INR 320 crore (FY2024), MSME book ~INR 18,500 crore (2025) and 24% YoY supply-chain finance growth (FY24-25); SBI, Carlyle, Advent support restored CET1 ~12.5% and total CAR ~16.0% (FY2024).

| Metric | Value |

|---|---|

| Digital loans | INR 6,200 cr (FY2024) |

| Bancassurance fees | INR 320 cr (FY2024) |

| MSME loans | ~INR 18,500 cr (2025) |

| Supply-chain finance growth | 24% YoY (FY24-25) |

| CET1 | ~12.5% (FY2024) |

| Total CAR | ~16.0% (FY2024) |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Yes Bank’s strategy, covering customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams with real-world operational insights and competitive analysis to support presentations, funding discussions, and strategic decision-making.

High-level snapshot of Yes Bank’s business model with editable cells to quickly identify core banking components, ideal for boardrooms, team collaboration, and fast executive summaries.

Activities

Lending and Credit Management

The bank disburses and manages loans across retail, MSME and corporate segments, using layered credit appraisal and monthly portfolio reviews; gross advances were Rs 1.12 lakh crore as of Sep 30, 2025, with retail at ~42% and MSME at ~18%.

Proactive monitoring targets GNPA below 2.5% and PCR (provision coverage ratio) above 75% by late 2025 to protect net interest margin, with targeted loan mix shifts to sustain NIM near 3.4%.

Digital Banking Operations

Yes Bank continuously develops and maintains digital platforms—mobile app and UPI—handling 28% of retail transactions digitally in FY2024 and 42m UPI transactions monthly (2024), focusing on faster onboarding, smoother payments, and reduced processing times.

Operations prioritize UX improvements and strong cybersecurity: 24/7 monitoring, ISO 27001 controls, and a 35% drop in fraud losses year-on-year to FY2024, supporting a digital-first strategy to win and keep tech-savvy customers.

Risk Management and Compliance

Yes Bank allocates significant staff and capital to meet Reserve Bank of India rules, running quarterly internal audits and annual stress tests; regulatory spend rose to an estimated ₹1.2–1.5 billion in FY2024 for compliance programs. The bank enforces AML (anti-money laundering) frameworks and credit/market risk controls to protect depositors and preserve its banking licence, keeping CET1 capital at or above regulatory buffers—12.5% reported in Sep 2024.

Customer Acquisition and Marketing

Yes Bank runs targeted marketing campaigns using data analytics to acquire deposits and loan customers, aiming to raise CASA (current and savings accounts) which was 23.8% in FY2024 to cut funding costs; campaigns focus on salaried millennials and SME segments with personalized digital offers and 20–30% higher conversion in pilot cohorts.

- CASA 23.8% (FY2024)

- Target segments: salaried millennials, SMEs

- Data-driven personalization lifts conversions 20–30%

- Goal: raise CASA to lower cost of funds

Wealth Management and Advisory

Wealth management and advisory is a core Yes Bank activity, serving HNWIs and corporates with portfolio management, market research, and asset-allocation strategies while distributing third-party products; fee income from wealth grew bank-wide, contributing to non-interest revenue that rose ~18% YoY to ₹3,450 crore in FY2024.

- HNW/Corp portfolio management

- Market research-led asset allocation

- Third-party product distribution

- Drives fee-based revenue; non-interest income ₹3,450 crore FY2024 (+18% YoY)

Yes Bank: ₹1.12Lcr advances, 42% retail, targeting GNPA <2.5% & PCR >75% by late‑2025

Yes Bank originates and services loans across retail, MSME and corporate; gross advances Rs 1.12 lakh crore (Sep 30, 2025), retail ~42%, MSME ~18%, targeting GNPA <2.5% and PCR >75% by late 2025 to protect NIM ~3.4%.

It runs digital channels (28% retail digital FY2024, 42m UPI/month 2024), strong cybersecurity (ISO 27001, 24/7), compliance spend ₹1.2–1.5bn FY2024, and fee income drove non-interest revenue ₹3,450cr (+18% YoY FY2024).

| Metric | Value |

|---|---|

| Gross advances | ₹1.12L cr (Sep 30, 2025) |

| Retail share | ~42% |

| MSME share | ~18% |

| GNPA target | <2.5% (late 2025) |

| PCR target | >75% (late 2025) |

| NIM | ~3.4% |

| Digital retail txn | 28% (FY2024) |

| UPI/month | 42m (2024) |

| Compliance spend | ₹1.2–1.5bn (FY2024) |

| Non-int income | ₹3,450cr (+18% YoY FY2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you see is the actual Yes Bank Business Model Canvas—not a mockup—and it matches the exact document you’ll receive after purchase; upon ordering, you’ll get the full, editable file in Word and Excel formats, structured and formatted exactly as shown.