Yes Bank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our concise PESTLE Analysis of Yes Bank—unpack how political shifts, economic trends, regulatory pressures, and technological disruption shape its outlook, and use these insights to inform smarter investment and strategy decisions; purchase the full report for the complete, ready-to-use breakdown and actionable recommendations.

Political factors

Government Stability and Policy Continuity

The Indian political landscape at end-2025 remains stable, with the government maintaining 2025-26 Union Budget capex of INR 11.1 trillion supporting infrastructure—this lets Yes Bank align long-term strategy to national fiscal goals. Continued policy continuity on digital public infrastructure (Aadhaar/UPI reach 750 million+ users in 2024) improves forecasting of retail and MSME credit demand. Reduced risk of abrupt regulatory shifts lowers potential operational disruption for banks.

Regulatory Oversight and RBI Intervention

As a reconstructed entity, Yes Bank remains under tight RBI scrutiny after the 2020 reconstruction; the central bank monitors capital ratios and governance—RBI required Yes Bank to maintain CET1 above 9% and CRAR above 12% in 2024–25. Political pressure to safeguard depositor confidence means stricter oversight of dividend payouts and branch expansion. Regulatory clearance has constrained Yes Bank’s aggressive growth plans, with loan book growth capped by supervisory limits and periodic reviews.

Financial Inclusion Initiatives

The government’s push via Pradhan Mantri Jan Dhan Yojana (over 460 million accounts since 2014) and related inclusion schemes compels Yes Bank to deepen presence in underserved markets, increasing CASA and low-ticket deposit volumes. Political directives to enroll private banks in low-cost insurance and pension programs (e.g., PM Suraksha Bima/PM Jeevan Jyoti reach >200 million policies) compress near-term margins due to higher operating costs and lower yields. This dual mandate forces Yes Bank to balance mandated social obligations with shareholder return targets, driving investments in low-cost distribution and digital onboarding to scale while protecting profitability.

Geopolitical Influence on Capital Inflows

India's growing role—GDP ~US$3.7tn (2024) and 6.8% IMF 2024 growth—boosts FPI flows, critical for Yes Bank's CET1 and capital adequacy as foreign ownership supports equity raises.

Political ties with US, EU, UAE influence ease of raising equity from FIIs; 2024 FPI net inflows to India were ~US$16bn, aiding liquidity access for banks like Yes Bank.

Geopolitical tensions risk capital flight, raising share-price volatility and pressuring liquidity ratios; heightened volatility in 2022–24 saw Indian banking beta spike versus benchmark.

- India GDP 2024 ~US$3.7tn; IMF growth 6.8%

- 2024 FPI net inflows ~US$16bn

- Tensions → higher volatility, stress on CET1 and liquidity

Public-Private Partnership Support

The Indian government’s push for public-private partnerships (PPPs) sustains a steady pipeline of corporate lending for Yes Bank, with infrastructure investment targets of $1.4 trillion to 2030 creating deal flow.

Production Linked Incentive schemes for green energy and manufacturing (allocations ~INR 1.97 lakh crore in 2023–25) bolster Yes Bank’s corporate book via project and working-capital loans.

Navigating these politically backed sectors requires expertise in subsidy timelines, viability gap funding and regulatory risk to manage credit exposure.

- PPPs and $1.4T infrastructure pipeline to 2030 = lending opportunities

- PLIs ~INR 1.97 lakh crore (2023–25) drive green/manufacturing loans

- Need for mastery of subsidy structures, timelines, regulatory risk

Capex, inclusion & PLIs fuel lending demand; RBI capital rules cap Yes Bank growth

Stable 2025 politics, INR 11.1tn capex (2025–26) and digital infrastructure (UPI/Aadhaar scale) support retail/MSME credit; RBI mandates CET1 >9% and CRAR >12% constrain Yes Bank growth; govt inclusion (Jan Dhan 460M+) and social schemes raise low-yield liabilities; $1.4tn PPP pipeline and PLIs ~INR 1.97 lakh crore (2023–25) create lending opportunities amid FPI inflows (~US$16bn 2024) and volatility risks.

| Metric | Value |

|---|---|

| Union capex 2025–26 | INR 11.1tn |

| CET1 / CRAR (RBI req) | >9% / >12% |

| Jan Dhan accounts | ~460M |

| PPP pipeline to 2030 | $1.4tn |

| PLIs (2023–25) | INR 1.97 lakh crore |

| FPI net inflows 2024 | ~US$16bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Yes Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, consultants, and investors in identifying threats, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary for Yes Bank that eases meeting prep and supports rapid decision-making by highlighting external risks and opportunities at a glance.

Economic factors

Interest Rate Environment and Monetary Policy

By end-2025 the RBI policy path will directly shape Yes Bank’s NIM and profitability: a 25–50bp repo cut cycle could compress funding costs but also squeeze yields, while a higher-rate scenario lifts deposit rates; Yes Bank reported a Q3 2025 NIM of ~3.6% (annualized), making sensitivity to repo moves material.

Repo rate volatility alters deposit costs and advance yields, forcing active ALM—Yes Bank’s CASA ratio of ~42% (FY2024) provides some buffer, but repricing mismatches can widen liquidity costs rapidly.

Navigating shifts from high-inflation regimes to growth-led rate cuts is critical to retain lending market share; stress-testing shows a 50bp easing could reduce NII by ~4–6% unless loan yields are restructured promptly.

India GDP Growth and Credit Demand

India’s GDP grew 7.3% in FY2023–24 and IMF projects 6.8% for 2024, underpinning robust retail and MSME credit demand that boosts Yes Bank’s working capital and personal loan portfolios.

Rising consumer spending and SME capex lifted bank credit growth to 15.6% YoY in 2024, directly benefiting Yes Bank’s loan book expansion.

However, regional slowdowns or sectoral stress can raise slippages; Yes Bank reported a GNPA ratio of 2.5% and a PCR of ~55% in 2024, exposing profitability to provisioning shocks.

Asset Quality and NPA Management

The legacy of bad loans still weighs on Yes Bank’s balance sheet, with gross NPA falling to 2.8% in FY2024 from double digits in 2020 but provisioning and restructuring costs keeping stressed exposure elevated.

The bank has sold over INR 35,000 crore of stressed assets to ARCs since the crisis, improving CET1 to approximately 12.5% by Sept 2025 while borrower-sector health—real estate and power—remains a vulnerability.

Ongoing monitoring of Credit Cost, which averaged about 0.9% in FY2024–25, is essential to prevent recurrence of high-NPA cycles and to sustain lending capacity.

Inflationary Pressures on Operating Costs

Rising inflation in India, with CPI around 6.7% in 2024-25, lifts Yes Bank’s operating expenses—notably employee wages and tech maintenance—pressuring margins and cost-to-income ratio.

Higher inflation erodes retail customers’ disposable income, which can slow growth of low-cost CASA; India’s urban real wage growth weakened in 2024, reducing deposit elasticity.

Yes Bank must pursue efficiency measures—automation, branch rationalization—to contain a reported FY2024 cost-to-income near industry mid-teens while navigating a high-cost environment.

- Inflation ~6.7% (2024-25) raises wage/tech costs

- Weaker real wages curb CASA growth

- Need for automation, branch rationalization

- Target: improve cost-to-income from mid-teens

MSME Sector Resilience

Yes Bank's sizable MSME loan book—around 18% of advances as of FY2025—makes it highly exposed to cyclical risks; MSME profitability at end-2025 will directly shape the bank's risk appetite and pricing. Economic shocks could lift MSME NPA formation quickly, as seen in 2020–21 when MSME slippages rose twofold, so the bank needs tighter credit scoring and stress-testing. Robust early warning systems and sectoral monitoring are essential to limit rapid asset-quality deterioration.

- MSME share ~18% of advances (FY2025)

- MSME slippage sensitivity: historical twofold rise under shock

- End-2025 MSME viability drives loan pricing and provisioning

- Requires enhanced stress tests, credit scoring, and EWS

Yes Bank outlook: NIM 3.6%, CASA 42%, GNPA 2.5%—GDP, CPI, RBI policy key

Macro: RBI policy, CPI ~6.7% (2024-25) and GDP ~6.8% (2024 proj.) drive Yes Bank NIM (Q3‑2025 ~3.6%), CASA ~42% (FY2024), GNPA ~2.5%/PCR ~55% (2024), CET1 ~12.5% (Sept‑2025), MSME ~18% of advances; credit cost ~0.9% (FY2024‑25) and loan growth ~15.6% YoY (2024) determine profitability and provisioning.

| Metric | Value |

|---|---|

| NIM Q3‑2025 | ~3.6% |

| CASA FY2024 | ~42% |

| GNPA 2024 | 2.5% |

| CET1 Sep‑2025 | ~12.5% |

Preview the Actual Deliverable

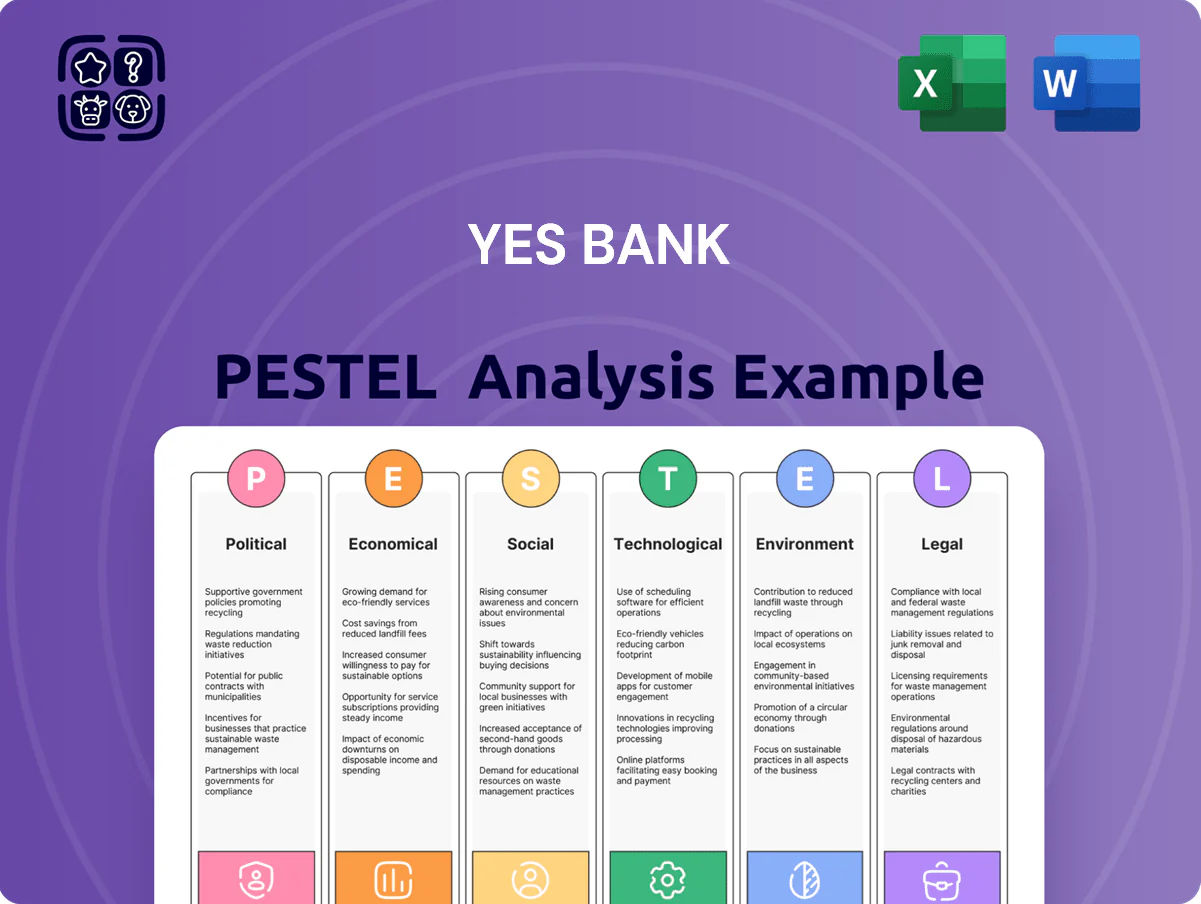

Yes Bank PESTLE Analysis

The preview shown here is the exact Yes Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and structure visible here match the downloadable file you’ll get immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our concise PESTLE Analysis of Yes Bank—unpack how political shifts, economic trends, regulatory pressures, and technological disruption shape its outlook, and use these insights to inform smarter investment and strategy decisions; purchase the full report for the complete, ready-to-use breakdown and actionable recommendations.

Political factors

Government Stability and Policy Continuity

The Indian political landscape at end-2025 remains stable, with the government maintaining 2025-26 Union Budget capex of INR 11.1 trillion supporting infrastructure—this lets Yes Bank align long-term strategy to national fiscal goals. Continued policy continuity on digital public infrastructure (Aadhaar/UPI reach 750 million+ users in 2024) improves forecasting of retail and MSME credit demand. Reduced risk of abrupt regulatory shifts lowers potential operational disruption for banks.

Regulatory Oversight and RBI Intervention

As a reconstructed entity, Yes Bank remains under tight RBI scrutiny after the 2020 reconstruction; the central bank monitors capital ratios and governance—RBI required Yes Bank to maintain CET1 above 9% and CRAR above 12% in 2024–25. Political pressure to safeguard depositor confidence means stricter oversight of dividend payouts and branch expansion. Regulatory clearance has constrained Yes Bank’s aggressive growth plans, with loan book growth capped by supervisory limits and periodic reviews.

Financial Inclusion Initiatives

The government’s push via Pradhan Mantri Jan Dhan Yojana (over 460 million accounts since 2014) and related inclusion schemes compels Yes Bank to deepen presence in underserved markets, increasing CASA and low-ticket deposit volumes. Political directives to enroll private banks in low-cost insurance and pension programs (e.g., PM Suraksha Bima/PM Jeevan Jyoti reach >200 million policies) compress near-term margins due to higher operating costs and lower yields. This dual mandate forces Yes Bank to balance mandated social obligations with shareholder return targets, driving investments in low-cost distribution and digital onboarding to scale while protecting profitability.

Geopolitical Influence on Capital Inflows

India's growing role—GDP ~US$3.7tn (2024) and 6.8% IMF 2024 growth—boosts FPI flows, critical for Yes Bank's CET1 and capital adequacy as foreign ownership supports equity raises.

Political ties with US, EU, UAE influence ease of raising equity from FIIs; 2024 FPI net inflows to India were ~US$16bn, aiding liquidity access for banks like Yes Bank.

Geopolitical tensions risk capital flight, raising share-price volatility and pressuring liquidity ratios; heightened volatility in 2022–24 saw Indian banking beta spike versus benchmark.

- India GDP 2024 ~US$3.7tn; IMF growth 6.8%

- 2024 FPI net inflows ~US$16bn

- Tensions → higher volatility, stress on CET1 and liquidity

Public-Private Partnership Support

The Indian government’s push for public-private partnerships (PPPs) sustains a steady pipeline of corporate lending for Yes Bank, with infrastructure investment targets of $1.4 trillion to 2030 creating deal flow.

Production Linked Incentive schemes for green energy and manufacturing (allocations ~INR 1.97 lakh crore in 2023–25) bolster Yes Bank’s corporate book via project and working-capital loans.

Navigating these politically backed sectors requires expertise in subsidy timelines, viability gap funding and regulatory risk to manage credit exposure.

- PPPs and $1.4T infrastructure pipeline to 2030 = lending opportunities

- PLIs ~INR 1.97 lakh crore (2023–25) drive green/manufacturing loans

- Need for mastery of subsidy structures, timelines, regulatory risk

Capex, inclusion & PLIs fuel lending demand; RBI capital rules cap Yes Bank growth

Stable 2025 politics, INR 11.1tn capex (2025–26) and digital infrastructure (UPI/Aadhaar scale) support retail/MSME credit; RBI mandates CET1 >9% and CRAR >12% constrain Yes Bank growth; govt inclusion (Jan Dhan 460M+) and social schemes raise low-yield liabilities; $1.4tn PPP pipeline and PLIs ~INR 1.97 lakh crore (2023–25) create lending opportunities amid FPI inflows (~US$16bn 2024) and volatility risks.

| Metric | Value |

|---|---|

| Union capex 2025–26 | INR 11.1tn |

| CET1 / CRAR (RBI req) | >9% / >12% |

| Jan Dhan accounts | ~460M |

| PPP pipeline to 2030 | $1.4tn |

| PLIs (2023–25) | INR 1.97 lakh crore |

| FPI net inflows 2024 | ~US$16bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Yes Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, consultants, and investors in identifying threats, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary for Yes Bank that eases meeting prep and supports rapid decision-making by highlighting external risks and opportunities at a glance.

Economic factors

Interest Rate Environment and Monetary Policy

By end-2025 the RBI policy path will directly shape Yes Bank’s NIM and profitability: a 25–50bp repo cut cycle could compress funding costs but also squeeze yields, while a higher-rate scenario lifts deposit rates; Yes Bank reported a Q3 2025 NIM of ~3.6% (annualized), making sensitivity to repo moves material.

Repo rate volatility alters deposit costs and advance yields, forcing active ALM—Yes Bank’s CASA ratio of ~42% (FY2024) provides some buffer, but repricing mismatches can widen liquidity costs rapidly.

Navigating shifts from high-inflation regimes to growth-led rate cuts is critical to retain lending market share; stress-testing shows a 50bp easing could reduce NII by ~4–6% unless loan yields are restructured promptly.

India GDP Growth and Credit Demand

India’s GDP grew 7.3% in FY2023–24 and IMF projects 6.8% for 2024, underpinning robust retail and MSME credit demand that boosts Yes Bank’s working capital and personal loan portfolios.

Rising consumer spending and SME capex lifted bank credit growth to 15.6% YoY in 2024, directly benefiting Yes Bank’s loan book expansion.

However, regional slowdowns or sectoral stress can raise slippages; Yes Bank reported a GNPA ratio of 2.5% and a PCR of ~55% in 2024, exposing profitability to provisioning shocks.

Asset Quality and NPA Management

The legacy of bad loans still weighs on Yes Bank’s balance sheet, with gross NPA falling to 2.8% in FY2024 from double digits in 2020 but provisioning and restructuring costs keeping stressed exposure elevated.

The bank has sold over INR 35,000 crore of stressed assets to ARCs since the crisis, improving CET1 to approximately 12.5% by Sept 2025 while borrower-sector health—real estate and power—remains a vulnerability.

Ongoing monitoring of Credit Cost, which averaged about 0.9% in FY2024–25, is essential to prevent recurrence of high-NPA cycles and to sustain lending capacity.

Inflationary Pressures on Operating Costs

Rising inflation in India, with CPI around 6.7% in 2024-25, lifts Yes Bank’s operating expenses—notably employee wages and tech maintenance—pressuring margins and cost-to-income ratio.

Higher inflation erodes retail customers’ disposable income, which can slow growth of low-cost CASA; India’s urban real wage growth weakened in 2024, reducing deposit elasticity.

Yes Bank must pursue efficiency measures—automation, branch rationalization—to contain a reported FY2024 cost-to-income near industry mid-teens while navigating a high-cost environment.

- Inflation ~6.7% (2024-25) raises wage/tech costs

- Weaker real wages curb CASA growth

- Need for automation, branch rationalization

- Target: improve cost-to-income from mid-teens

MSME Sector Resilience

Yes Bank's sizable MSME loan book—around 18% of advances as of FY2025—makes it highly exposed to cyclical risks; MSME profitability at end-2025 will directly shape the bank's risk appetite and pricing. Economic shocks could lift MSME NPA formation quickly, as seen in 2020–21 when MSME slippages rose twofold, so the bank needs tighter credit scoring and stress-testing. Robust early warning systems and sectoral monitoring are essential to limit rapid asset-quality deterioration.

- MSME share ~18% of advances (FY2025)

- MSME slippage sensitivity: historical twofold rise under shock

- End-2025 MSME viability drives loan pricing and provisioning

- Requires enhanced stress tests, credit scoring, and EWS

Yes Bank outlook: NIM 3.6%, CASA 42%, GNPA 2.5%—GDP, CPI, RBI policy key

Macro: RBI policy, CPI ~6.7% (2024-25) and GDP ~6.8% (2024 proj.) drive Yes Bank NIM (Q3‑2025 ~3.6%), CASA ~42% (FY2024), GNPA ~2.5%/PCR ~55% (2024), CET1 ~12.5% (Sept‑2025), MSME ~18% of advances; credit cost ~0.9% (FY2024‑25) and loan growth ~15.6% YoY (2024) determine profitability and provisioning.

| Metric | Value |

|---|---|

| NIM Q3‑2025 | ~3.6% |

| CASA FY2024 | ~42% |

| GNPA 2024 | 2.5% |

| CET1 Sep‑2025 | ~12.5% |

Preview the Actual Deliverable

Yes Bank PESTLE Analysis

The preview shown here is the exact Yes Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and structure visible here match the downloadable file you’ll get immediately after checkout.