Yuanta Financial Holding Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

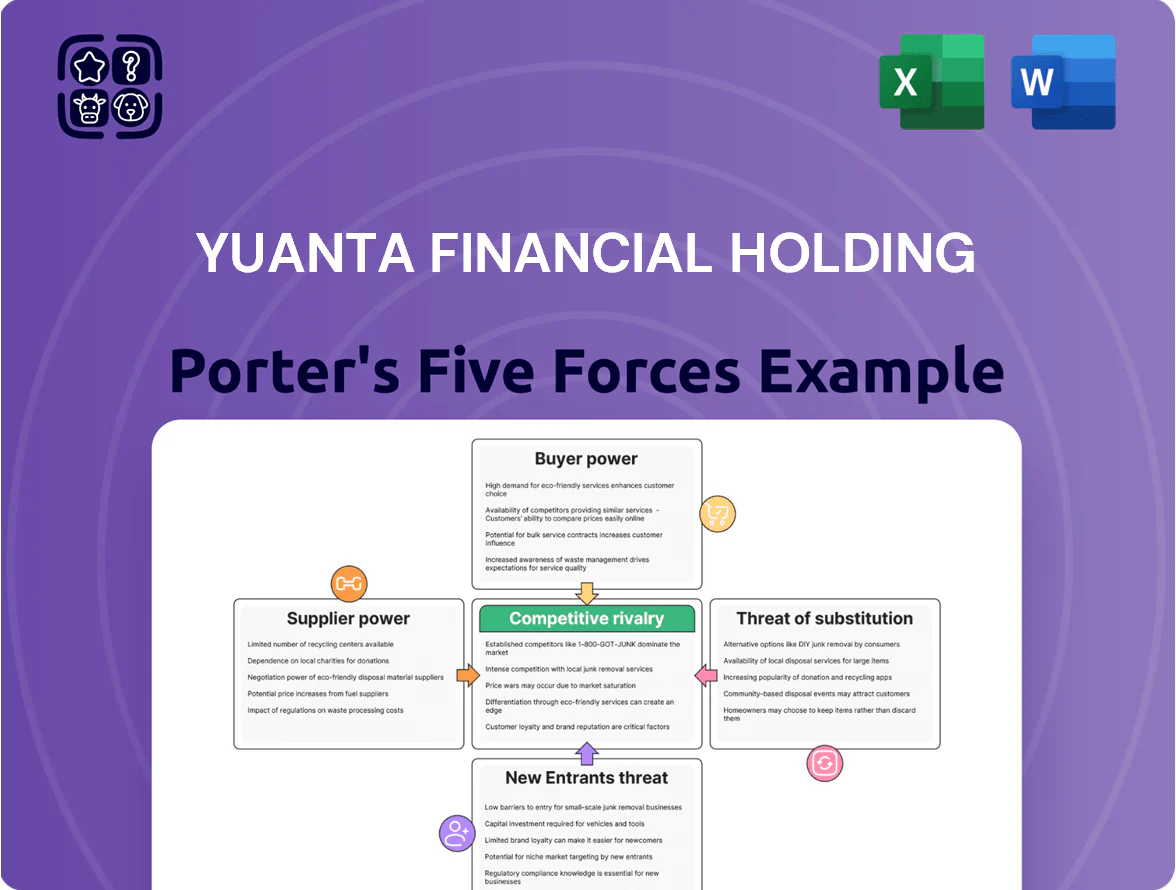

Yuanta Financial Holding operates in a tightly regulated, capital-intensive sector where competitive rivalry and buyer power are significant but mitigated by scale and diversified services; supplier and substitute threats remain moderate while barriers to entry are high due to licensing and trust requirements. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Yuanta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Fintech Talent

Demand for top-tier software engineers and cybersecurity experts in Taiwan’s financial sector stayed high through 2025, with tech job vacancies up 18% year-over-year and median cybersec salaries reaching NT$1.9M (≈US$60k) in 2025; Yuanta must poach talent from TSMC, ASUS, and global banks, so suppliers of this human capital hold strong leverage, pushing compensation and benefits higher and raising Yuanta’s operating costs by an estimated 3–5% of IT payroll.

Dependence on Global Financial Data Providers

Yuanta relies on a handful of global data providers—notably Bloomberg and Refinitiv—for real-time market data, analytics, and terminals; these vendors charge premium fees, with Bloomberg Terminal fees around $27,000 per seat annually (2025 industry estimate), giving suppliers strong pricing power. Because real-time feeds and analytics are mission-critical for brokerage and investment banking, Yuanta has limited bargaining leverage and little room to substitute without service or cost loss. A 10% vendor price hike or a week-long outage could raise securities division operating costs materially; for example, a 10% rise on $50m in data/license spend equals $5m extra annual cost. Supply disruption risk thus directly pressures margins and pricing flexibility.

Cost of Capital from Retail and Institutional Depositors

Yuanta’s banks treat depositors as suppliers of capital; by Q3 2025, Taiwan household deposit flows to higher-yield products rose ~8% YoY, and fintech savings grew 14% YoY, pushing Yuanta to raise average deposit rates from 0.9% in 2023 to ~1.8% in 2025. Higher rates lift cost of funds, compressing net interest margin (NIM)—Yuanta Financial reported consolidated NIM of 1.35% in 2025, down 20 bps vs 2023.

Critical Cloud Infrastructure and Outsourcing

The move to cloud ties Yuanta to a few hyperscalers—Amazon Web Services, Microsoft Azure, Google Cloud—creating strong supplier power because switching costs (re-architecting apps, data migration, retraining) often exceed millions; a typical bank cloud migration can cost US$5–20m and take 12–24 months.

Taiwan data-residency rules shrink vendor options, raising negotiation leverage for local compliant providers and hyprescalers with Taiwan regions, and increasing risk if a provider raises prices or limits capacity.

Regulatory Compliance and Auditing Services

The Financial Supervisory Commission tightened ESG reporting and AML rules in 2024, raising demand for specialized auditing and legal services for complex groups like Yuanta Financial Holding.

Top-tier firms that audit conglomerates command high fees and limited capacity; Deloitte, KPMG, EY, and PwC handled over 60% of Taiwan’s Big Four-listed audits in 2024, keeping supplier leverage strong.

As compliance spend rose—estimated 12% year-over-year in 2024 for Taiwan banks—Yuanta faces sustained supplier bargaining power for certification and advisory work.

- FSC tightened ESG/AML in 2024

- Big Four cover 60%+ of major audits

- Compliance spend up ~12% YoY in 2024

- Limited specialist supply → high supplier leverage

Suppliers Squeeze Margins: Tech, Data & Cloud Costs Push NIM Down to ~1.35% (2025)

Suppliers hold strong leverage: tech talent shortages raised IT payroll costs ~3–5% (2025); Bloomberg/Refinitiv data fees (~$27k/seat) risk $5m extra if raised 10% on $50m spend; cloud hyperscalers control ~65–70% market (2024) with switch costs US$5–20m (12–24 months); deposit shifts lifted average deposit rates to ~1.8% (2025), cutting NIM to 1.35% (2025).

| Category | Key Metric | Year |

|---|---|---|

| Tech salaries | NT$1.9M median cybersec | 2025 |

| Data vendors | $27k/seat est. | 2025 |

| Cloud market | 65–70% hyperscalers | 2024 |

| Switch cost | US$5–20m, 12–24m | typical |

| Deposit rate | ~1.8% avg | 2025 |

| NIM | 1.35% consolidated | 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Yuanta Financial Holding highlighting competitive intensity, buyer and supplier power, threat of substitutes and entrants, and strategic levers to protect margins and market share.

A concise Porter's Five Forces snapshot for Yuanta Financial Holding—quickly highlights competitive pressures and relief strategies for boardrooms and investor decks.

Customers Bargaining Power

High Price Sensitivity in Brokerage Services

Yuanta dominates Taiwan's securities market with ~25% retail share in 2024, but retail clients show high price sensitivity to commissions, with 58% citing fees as top brokerage factor in a 2023 Taiwan investor survey.

The rise of low-cost digital brokers cut average commission rates from ~0.15% in 2018 to ~0.05% by 2024, pushing investors to demand lower fees and faster execution.

If Yuanta keeps higher pricing, it risks losing share to discount rivals; a 1bp commission gap can shift ~0.5–1.2% of active retail volumes annually.

Low Switching Costs for Wealth Management Clients

Wealth clients in 2025 can easily compare Yuanta Financial Holding’s fund returns to global benchmarks via platforms and Bloomberg data, and net flows show Taiwanese HNW clients moved an estimated TWD 120 billion in 2024–25 between institutions; low switching costs cut loyalty and raise pressure on Yuanta to outperfom (sic), so the firm must boost RM spending—estimated +15–25%—to retain top clients.

Bargaining Power of Large Corporate Borrowers

Institutional clients and large Taiwanese corporates hold strong leverage over Yuanta Financial Holding because their deals account for an estimated 30–45% of institutional revenues; in 2024 Yuanta’s corporate lending book was NT$1.2 trillion, so loss of a few key accounts would hit fee and interest income materially. These customers routinely solicit bids from 3–6 banks, forcing Yuanta to trim margins—underwriting fees dropped ~12% across peers in 2023—while competition lets big clients dictate covenants and pricing.

Sophistication of Digital Banking Users

The modern banking customer expects seamless multi-channel digital experiences and personalized products, making UX and AI advisory table stakes; global data shows 78% of consumers use mobile banking in 2024 and 62% prefer personalized offers, raising churn risk for laggards. Yuanta must continuously invest in its digital ecosystem—apps, APIs, AI advisors—to retain clients and match competitors that can poach users with superior interfaces.

- 78% mobile banking use (2024)

- 62% prefer personalized offers

- AI advice increases retention vs legacy UX

- Continuous digital investment needed to avoid churn

Impact of Consumer Protection Regulations

By end-2025 Taiwan laws boosted consumer transparency and data portability, enabling 28% faster account switches and 15% higher product comparison usage per FSC 2024–25 reports, shifting bargaining power to individuals and pressuring Yuanta Financial Holding to prioritize customer-centric pricing and retention.

Fee pressure, digital churn & HNW shifts squeeze margins—retail power reshapes revenues

Customers hold strong bargaining power: retail fee sensitivity (58% cite fees, 2023) and discount brokers cut commissions from ~0.15% (2018) to ~0.05% (2024), moving volumes; a 1bp gap shifts ~0.5–1.2% retail volume. HNW/net flows ~TWD120bn moved 2024–25; institutional clients drive 30–45% of institutional revenue. Digital expectations (78% mobile use, 62% want personalization) raise churn risk.

| Metric | Value |

|---|---|

| Retail market share (Yuanta, 2024) | ~25% |

| Fee sensitivity (investor survey, 2023) | 58% |

| Avg commission rate (2018 → 2024) | ~0.15% → ~0.05% |

| Volume shift per 1bp gap | ~0.5–1.2% |

| HNW flows moved (2024–25) | TWD 120bn |

| Institutional revenue concentration | 30–45% |

| Mobile banking use (2024) | 78% |

| Prefer personalized offers | 62% |

Preview Before You Purchase

Yuanta Financial Holding Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Yuanta Financial Holding you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Yuanta Financial Holding operates in a tightly regulated, capital-intensive sector where competitive rivalry and buyer power are significant but mitigated by scale and diversified services; supplier and substitute threats remain moderate while barriers to entry are high due to licensing and trust requirements. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Yuanta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Fintech Talent

Demand for top-tier software engineers and cybersecurity experts in Taiwan’s financial sector stayed high through 2025, with tech job vacancies up 18% year-over-year and median cybersec salaries reaching NT$1.9M (≈US$60k) in 2025; Yuanta must poach talent from TSMC, ASUS, and global banks, so suppliers of this human capital hold strong leverage, pushing compensation and benefits higher and raising Yuanta’s operating costs by an estimated 3–5% of IT payroll.

Dependence on Global Financial Data Providers

Yuanta relies on a handful of global data providers—notably Bloomberg and Refinitiv—for real-time market data, analytics, and terminals; these vendors charge premium fees, with Bloomberg Terminal fees around $27,000 per seat annually (2025 industry estimate), giving suppliers strong pricing power. Because real-time feeds and analytics are mission-critical for brokerage and investment banking, Yuanta has limited bargaining leverage and little room to substitute without service or cost loss. A 10% vendor price hike or a week-long outage could raise securities division operating costs materially; for example, a 10% rise on $50m in data/license spend equals $5m extra annual cost. Supply disruption risk thus directly pressures margins and pricing flexibility.

Cost of Capital from Retail and Institutional Depositors

Yuanta’s banks treat depositors as suppliers of capital; by Q3 2025, Taiwan household deposit flows to higher-yield products rose ~8% YoY, and fintech savings grew 14% YoY, pushing Yuanta to raise average deposit rates from 0.9% in 2023 to ~1.8% in 2025. Higher rates lift cost of funds, compressing net interest margin (NIM)—Yuanta Financial reported consolidated NIM of 1.35% in 2025, down 20 bps vs 2023.

Critical Cloud Infrastructure and Outsourcing

The move to cloud ties Yuanta to a few hyperscalers—Amazon Web Services, Microsoft Azure, Google Cloud—creating strong supplier power because switching costs (re-architecting apps, data migration, retraining) often exceed millions; a typical bank cloud migration can cost US$5–20m and take 12–24 months.

Taiwan data-residency rules shrink vendor options, raising negotiation leverage for local compliant providers and hyprescalers with Taiwan regions, and increasing risk if a provider raises prices or limits capacity.

Regulatory Compliance and Auditing Services

The Financial Supervisory Commission tightened ESG reporting and AML rules in 2024, raising demand for specialized auditing and legal services for complex groups like Yuanta Financial Holding.

Top-tier firms that audit conglomerates command high fees and limited capacity; Deloitte, KPMG, EY, and PwC handled over 60% of Taiwan’s Big Four-listed audits in 2024, keeping supplier leverage strong.

As compliance spend rose—estimated 12% year-over-year in 2024 for Taiwan banks—Yuanta faces sustained supplier bargaining power for certification and advisory work.

- FSC tightened ESG/AML in 2024

- Big Four cover 60%+ of major audits

- Compliance spend up ~12% YoY in 2024

- Limited specialist supply → high supplier leverage

Suppliers Squeeze Margins: Tech, Data & Cloud Costs Push NIM Down to ~1.35% (2025)

Suppliers hold strong leverage: tech talent shortages raised IT payroll costs ~3–5% (2025); Bloomberg/Refinitiv data fees (~$27k/seat) risk $5m extra if raised 10% on $50m spend; cloud hyperscalers control ~65–70% market (2024) with switch costs US$5–20m (12–24 months); deposit shifts lifted average deposit rates to ~1.8% (2025), cutting NIM to 1.35% (2025).

| Category | Key Metric | Year |

|---|---|---|

| Tech salaries | NT$1.9M median cybersec | 2025 |

| Data vendors | $27k/seat est. | 2025 |

| Cloud market | 65–70% hyperscalers | 2024 |

| Switch cost | US$5–20m, 12–24m | typical |

| Deposit rate | ~1.8% avg | 2025 |

| NIM | 1.35% consolidated | 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Yuanta Financial Holding highlighting competitive intensity, buyer and supplier power, threat of substitutes and entrants, and strategic levers to protect margins and market share.

A concise Porter's Five Forces snapshot for Yuanta Financial Holding—quickly highlights competitive pressures and relief strategies for boardrooms and investor decks.

Customers Bargaining Power

High Price Sensitivity in Brokerage Services

Yuanta dominates Taiwan's securities market with ~25% retail share in 2024, but retail clients show high price sensitivity to commissions, with 58% citing fees as top brokerage factor in a 2023 Taiwan investor survey.

The rise of low-cost digital brokers cut average commission rates from ~0.15% in 2018 to ~0.05% by 2024, pushing investors to demand lower fees and faster execution.

If Yuanta keeps higher pricing, it risks losing share to discount rivals; a 1bp commission gap can shift ~0.5–1.2% of active retail volumes annually.

Low Switching Costs for Wealth Management Clients

Wealth clients in 2025 can easily compare Yuanta Financial Holding’s fund returns to global benchmarks via platforms and Bloomberg data, and net flows show Taiwanese HNW clients moved an estimated TWD 120 billion in 2024–25 between institutions; low switching costs cut loyalty and raise pressure on Yuanta to outperfom (sic), so the firm must boost RM spending—estimated +15–25%—to retain top clients.

Bargaining Power of Large Corporate Borrowers

Institutional clients and large Taiwanese corporates hold strong leverage over Yuanta Financial Holding because their deals account for an estimated 30–45% of institutional revenues; in 2024 Yuanta’s corporate lending book was NT$1.2 trillion, so loss of a few key accounts would hit fee and interest income materially. These customers routinely solicit bids from 3–6 banks, forcing Yuanta to trim margins—underwriting fees dropped ~12% across peers in 2023—while competition lets big clients dictate covenants and pricing.

Sophistication of Digital Banking Users

The modern banking customer expects seamless multi-channel digital experiences and personalized products, making UX and AI advisory table stakes; global data shows 78% of consumers use mobile banking in 2024 and 62% prefer personalized offers, raising churn risk for laggards. Yuanta must continuously invest in its digital ecosystem—apps, APIs, AI advisors—to retain clients and match competitors that can poach users with superior interfaces.

- 78% mobile banking use (2024)

- 62% prefer personalized offers

- AI advice increases retention vs legacy UX

- Continuous digital investment needed to avoid churn

Impact of Consumer Protection Regulations

By end-2025 Taiwan laws boosted consumer transparency and data portability, enabling 28% faster account switches and 15% higher product comparison usage per FSC 2024–25 reports, shifting bargaining power to individuals and pressuring Yuanta Financial Holding to prioritize customer-centric pricing and retention.

Fee pressure, digital churn & HNW shifts squeeze margins—retail power reshapes revenues

Customers hold strong bargaining power: retail fee sensitivity (58% cite fees, 2023) and discount brokers cut commissions from ~0.15% (2018) to ~0.05% (2024), moving volumes; a 1bp gap shifts ~0.5–1.2% retail volume. HNW/net flows ~TWD120bn moved 2024–25; institutional clients drive 30–45% of institutional revenue. Digital expectations (78% mobile use, 62% want personalization) raise churn risk.

| Metric | Value |

|---|---|

| Retail market share (Yuanta, 2024) | ~25% |

| Fee sensitivity (investor survey, 2023) | 58% |

| Avg commission rate (2018 → 2024) | ~0.15% → ~0.05% |

| Volume shift per 1bp gap | ~0.5–1.2% |

| HNW flows moved (2024–25) | TWD 120bn |

| Institutional revenue concentration | 30–45% |

| Mobile banking use (2024) | 78% |

| Prefer personalized offers | 62% |

Preview Before You Purchase

Yuanta Financial Holding Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Yuanta Financial Holding you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.