Zachry Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

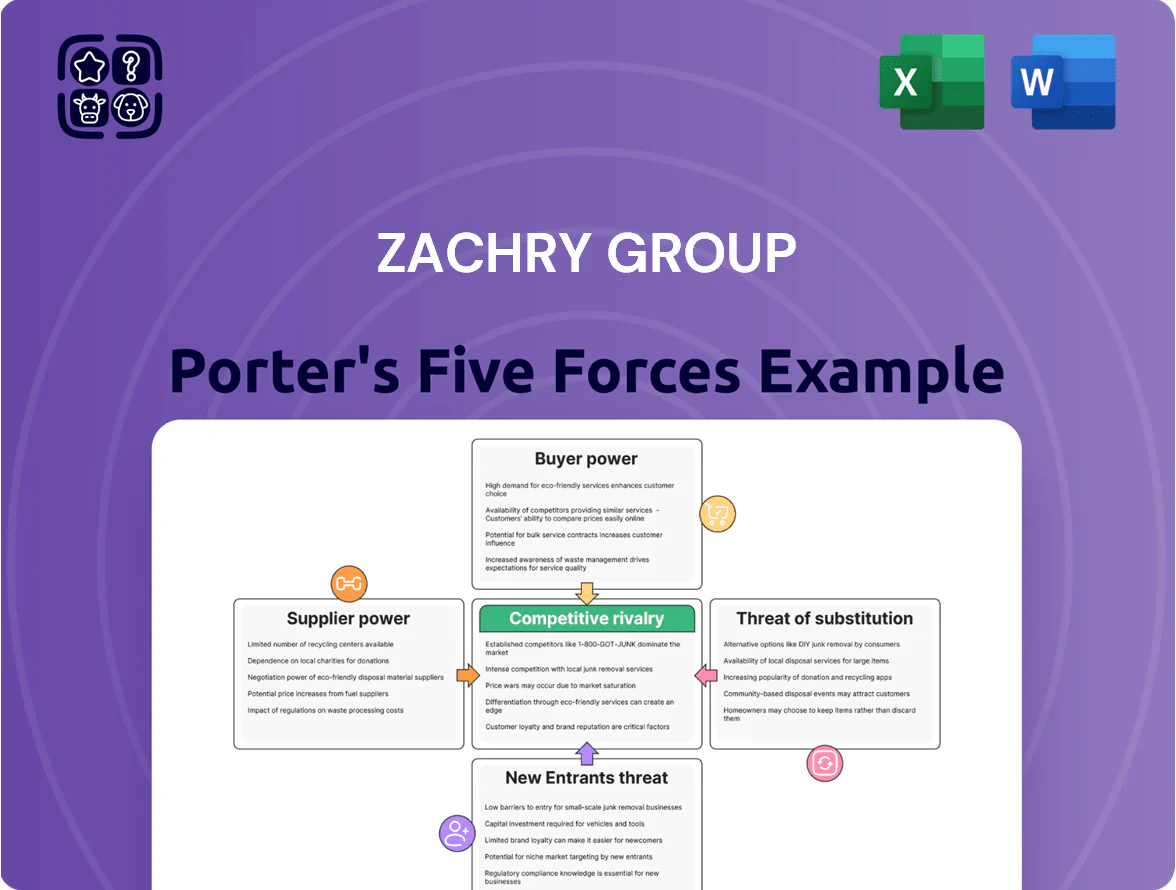

Zachry Group operates in a capital-intensive, relationship-driven construction and engineering sector where supplier reliability, client bargaining power, and high entry barriers shape strategic positioning; competitive rivalry hinges on project pipelines and specialized capabilities while substitute threats are limited but technological disruption and regulatory shifts pose real risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Zachry Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Skilled Labor Scarcity

The 2025 industrial construction shortage of certified welders and specialist engineers (estimated 18% national shortfall per Bureau of Labor Statistics 2024–25 projections) gives unions and staffing firms strong bargaining power over Zachry Group, which depends on that workforce for complex energy and chemical projects.

Zachry must pay wage premiums—reported 12–20% higher for certified pipeline welders in 2025—and richer benefits to retain staff, squeezing gross margins on major contracts and raising bid premiums for new work.

Volatility of Raw Material Costs

Suppliers of structural steel, copper, and specialty alloys exert real leverage: global trade policy shifts and supply-chain bottlenecks pushed steel futures up ~28% and copper ~22% YTD by Nov 2025, making long-term hedges imperfect.

Zachry must secure priority allocations and layer short-term purchases with 12–24 month contracts to reduce delay risk; a single-month shortage can add 3–5% to project costs and shift timelines.

Dominance of Heavy Equipment Manufacturers

The supplier base for turbines, reactors and other long-lead heavy equipment is very narrow—roughly 5–10 global OEMs dominate segments—letting suppliers set prices and delivery terms; industry reports show lead times of 18–36 months for major pieces.

Zachry Group relies on multi-year procurement plans and advance contracts to lock capacity and mitigate price volatility; a 2024 EPC survey found 68% of firms use 2–5 year supplier commitments for major equipment.

Subcontractor Dependency in Niche Markets

Zachry relies on a tiny pool of subcontractors for niche work like advanced environmental remediation and high-tech instrumentation, many holding unique certifications and five-star safety records required by power and manufacturing regulators.

Those subcontractors can pick among major EPC firms, letting them demand 30–90 day early-payment premiums, higher margins (often 10–20% above standard rates), and stricter contract clauses.

What this hides: a single supplier failure can delay projects by 4–12 weeks and add 1–3% to total project cost.

- Small supplier pool: < 10 qualified firms per niche

- Typical margin premium: 10–20%

- Delay risk: 4–12 weeks per supplier disruption

Energy and Logistics Provider Influence

- Diesel +14% in 2024 — higher operating costs

- US railcar loadings −3% Y/Y in 2024 — capacity tight

- Heavy-lift charters $200k–$1M+ — supplier leverage

- Remote sites amplify delays and price power

Supply Squeeze: Labor, metals & OEM bottlenecks Driving Costs and Delays

Suppliers hold high power: labor shortfall ~18% (BLS 2024–25), welder wages +12–20% (2025), steel futures +28% & copper +22% YTD Nov 2025, long-lead OEMs 5–10 players with 18–36 month lead times, single supplier failure adds 4–12 weeks and 1–3% cost, diesel +14% (2024), heavy-lift charters $200k–$1M.

| Metric | Value |

|---|---|

| Labor shortfall | 18% |

| Welder wage prem | 12–20% |

| Steel / Copper YTD | +28% / +22% |

| OEMs | 5–10 |

What is included in the product

Tailored exclusively for Zachry Group, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its profitability and strategic positioning.

A concise Porter's Five Forces overview tailored for Zachry Group—streamlines competitive pressure insights for faster strategic decisions.

Customers Bargaining Power

Concentration of Large Scale Industrial Clients

The customer base for Zachry Group is concentrated among a small set of mega corporates in energy, chemicals, and power, where the top 10 clients can account for over 60% of revenue in comparable EPC firms; that concentration raises customer bargaining power.

Global oil majors and utility giants control capital expenditure pools often exceeding $10–50 billion annually, letting them demand lower prices, stricter liability terms, and accelerated payment schedules during competitive bids.

In 2024 tender data, large owners negotiated average EPC margin compression of 200–400 basis points versus mid-market projects, forcing contractors like Zachry to pursue scope carve-outs, performance guarantees, or JV structures to protect margins.

Shift Toward Fixed Price Contract Models

High Transparency in Competitive Bidding

Sophisticated procurement teams at major industrial clients use digital platforms and historical bid data to compare proposals to the penny, driving transparency; a 2024 McKinsey survey found 68% of EPC buyers use e-procurement and benchmarking tools. This precision forces Zachry into price competition on commoditized scopes, with margins for non-specialized work falling as much as 200–400 basis points versus bespoke projects. Easy switching between reputable contractors each 3–5 years keeps continuous efficiency pressure on Zachry.

Stringent Financial and Safety Requirements

Customers in heavy industry now demand spotless safety records and rock-solid finances to qualify for bids; after Zachry Group's high-profile disputes (notably 2021–2023 contract claims), procurement teams in 2025 require enhanced balance-sheet scrutiny, credit ratings, and liquidity ratios before shortlisting partners.

Because major projects exceed billions (US pipeline and infrastructure tenders often >$1bn), even a single negative flag can eliminate a bidder entirely, shifting negotiating leverage to buyers.

- 2025 trend: lenders/owners expect current ratio ≥1.2 and EBITDA coverage visible

- Zero-tolerance on 3+ OSHA recordable incidents in 3 years

- Failure to meet financial covenants often disqualifies bidders on $1bn+ projects

Internal Engineering Capabilities of Owners

Many of Zachry Group’s biggest clients, like large refiners and chemical firms, run internal engineering and project teams that handle routine maintenance and small upgrades; in 2024, integrated oil majors reduced external maintenance spend by roughly 12% as onshore teams grew.

This in-house alternative lets customers threaten to in-source work if Zachry’s bids or delivery slip, cutting Zachry’s leverage especially in recurring maintenance and turnaround (TAR) work where contracts are smaller and margins thin.

That dynamic likely pressures pricing and adds churn risk: if 20–30% of routine TAR volume can be insourced, Zachry faces concentrated revenue exposure in those segments.

- Clients’ internal teams grew maintenance spend share ~12% (2024)

- In-sourcing threat strongest for routine TAR and small upgrades

- Estimated 20–30% of routine TAR volume at risk

Buyer Power Surge: Top-Clients >60%, Lump-Sum & E-Procurement Drive 200–400bp Margin Hit

Customers hold high bargaining power: top 10 clients can be >60% revenue, large owners force 200–400bp margin compression, 40–55% of big deals moved to lump-sum by 2025, and 68% use e-procurement; balance-sheet, safety, and insourcing (12% shift in 2024; 20–30% TAR at risk) amplify buyer leverage.

| Metric | Value (2024–25) |

|---|---|

| Top-10 client share | >60% |

| Margin compression (large bids) | 200–400 bp |

| Lump-sum deal share | 40–55% |

| E-procurement usage | 68% |

| In-house maintenance shift | 12% |

| TAR volume at risk | 20–30% |

Preview the Actual Deliverable

Zachry Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Zachry Group you’ll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Zachry Group operates in a capital-intensive, relationship-driven construction and engineering sector where supplier reliability, client bargaining power, and high entry barriers shape strategic positioning; competitive rivalry hinges on project pipelines and specialized capabilities while substitute threats are limited but technological disruption and regulatory shifts pose real risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Zachry Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Skilled Labor Scarcity

The 2025 industrial construction shortage of certified welders and specialist engineers (estimated 18% national shortfall per Bureau of Labor Statistics 2024–25 projections) gives unions and staffing firms strong bargaining power over Zachry Group, which depends on that workforce for complex energy and chemical projects.

Zachry must pay wage premiums—reported 12–20% higher for certified pipeline welders in 2025—and richer benefits to retain staff, squeezing gross margins on major contracts and raising bid premiums for new work.

Volatility of Raw Material Costs

Suppliers of structural steel, copper, and specialty alloys exert real leverage: global trade policy shifts and supply-chain bottlenecks pushed steel futures up ~28% and copper ~22% YTD by Nov 2025, making long-term hedges imperfect.

Zachry must secure priority allocations and layer short-term purchases with 12–24 month contracts to reduce delay risk; a single-month shortage can add 3–5% to project costs and shift timelines.

Dominance of Heavy Equipment Manufacturers

The supplier base for turbines, reactors and other long-lead heavy equipment is very narrow—roughly 5–10 global OEMs dominate segments—letting suppliers set prices and delivery terms; industry reports show lead times of 18–36 months for major pieces.

Zachry Group relies on multi-year procurement plans and advance contracts to lock capacity and mitigate price volatility; a 2024 EPC survey found 68% of firms use 2–5 year supplier commitments for major equipment.

Subcontractor Dependency in Niche Markets

Zachry relies on a tiny pool of subcontractors for niche work like advanced environmental remediation and high-tech instrumentation, many holding unique certifications and five-star safety records required by power and manufacturing regulators.

Those subcontractors can pick among major EPC firms, letting them demand 30–90 day early-payment premiums, higher margins (often 10–20% above standard rates), and stricter contract clauses.

What this hides: a single supplier failure can delay projects by 4–12 weeks and add 1–3% to total project cost.

- Small supplier pool: < 10 qualified firms per niche

- Typical margin premium: 10–20%

- Delay risk: 4–12 weeks per supplier disruption

Energy and Logistics Provider Influence

- Diesel +14% in 2024 — higher operating costs

- US railcar loadings −3% Y/Y in 2024 — capacity tight

- Heavy-lift charters $200k–$1M+ — supplier leverage

- Remote sites amplify delays and price power

Supply Squeeze: Labor, metals & OEM bottlenecks Driving Costs and Delays

Suppliers hold high power: labor shortfall ~18% (BLS 2024–25), welder wages +12–20% (2025), steel futures +28% & copper +22% YTD Nov 2025, long-lead OEMs 5–10 players with 18–36 month lead times, single supplier failure adds 4–12 weeks and 1–3% cost, diesel +14% (2024), heavy-lift charters $200k–$1M.

| Metric | Value |

|---|---|

| Labor shortfall | 18% |

| Welder wage prem | 12–20% |

| Steel / Copper YTD | +28% / +22% |

| OEMs | 5–10 |

What is included in the product

Tailored exclusively for Zachry Group, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its profitability and strategic positioning.

A concise Porter's Five Forces overview tailored for Zachry Group—streamlines competitive pressure insights for faster strategic decisions.

Customers Bargaining Power

Concentration of Large Scale Industrial Clients

The customer base for Zachry Group is concentrated among a small set of mega corporates in energy, chemicals, and power, where the top 10 clients can account for over 60% of revenue in comparable EPC firms; that concentration raises customer bargaining power.

Global oil majors and utility giants control capital expenditure pools often exceeding $10–50 billion annually, letting them demand lower prices, stricter liability terms, and accelerated payment schedules during competitive bids.

In 2024 tender data, large owners negotiated average EPC margin compression of 200–400 basis points versus mid-market projects, forcing contractors like Zachry to pursue scope carve-outs, performance guarantees, or JV structures to protect margins.

Shift Toward Fixed Price Contract Models

High Transparency in Competitive Bidding

Sophisticated procurement teams at major industrial clients use digital platforms and historical bid data to compare proposals to the penny, driving transparency; a 2024 McKinsey survey found 68% of EPC buyers use e-procurement and benchmarking tools. This precision forces Zachry into price competition on commoditized scopes, with margins for non-specialized work falling as much as 200–400 basis points versus bespoke projects. Easy switching between reputable contractors each 3–5 years keeps continuous efficiency pressure on Zachry.

Stringent Financial and Safety Requirements

Customers in heavy industry now demand spotless safety records and rock-solid finances to qualify for bids; after Zachry Group's high-profile disputes (notably 2021–2023 contract claims), procurement teams in 2025 require enhanced balance-sheet scrutiny, credit ratings, and liquidity ratios before shortlisting partners.

Because major projects exceed billions (US pipeline and infrastructure tenders often >$1bn), even a single negative flag can eliminate a bidder entirely, shifting negotiating leverage to buyers.

- 2025 trend: lenders/owners expect current ratio ≥1.2 and EBITDA coverage visible

- Zero-tolerance on 3+ OSHA recordable incidents in 3 years

- Failure to meet financial covenants often disqualifies bidders on $1bn+ projects

Internal Engineering Capabilities of Owners

Many of Zachry Group’s biggest clients, like large refiners and chemical firms, run internal engineering and project teams that handle routine maintenance and small upgrades; in 2024, integrated oil majors reduced external maintenance spend by roughly 12% as onshore teams grew.

This in-house alternative lets customers threaten to in-source work if Zachry’s bids or delivery slip, cutting Zachry’s leverage especially in recurring maintenance and turnaround (TAR) work where contracts are smaller and margins thin.

That dynamic likely pressures pricing and adds churn risk: if 20–30% of routine TAR volume can be insourced, Zachry faces concentrated revenue exposure in those segments.

- Clients’ internal teams grew maintenance spend share ~12% (2024)

- In-sourcing threat strongest for routine TAR and small upgrades

- Estimated 20–30% of routine TAR volume at risk

Buyer Power Surge: Top-Clients >60%, Lump-Sum & E-Procurement Drive 200–400bp Margin Hit

Customers hold high bargaining power: top 10 clients can be >60% revenue, large owners force 200–400bp margin compression, 40–55% of big deals moved to lump-sum by 2025, and 68% use e-procurement; balance-sheet, safety, and insourcing (12% shift in 2024; 20–30% TAR at risk) amplify buyer leverage.

| Metric | Value (2024–25) |

|---|---|

| Top-10 client share | >60% |

| Margin compression (large bids) | 200–400 bp |

| Lump-sum deal share | 40–55% |

| E-procurement usage | 68% |

| In-house maintenance shift | 12% |

| TAR volume at risk | 20–30% |

Preview the Actual Deliverable

Zachry Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Zachry Group you’ll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders or mockups.