Zachry Group SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Zachry Group’s deep engineering expertise and diversified project portfolio position it well in infrastructure and energy markets, yet exposure to cyclical construction demand and regulatory shifts are clear risks. Want the complete picture—with financial context, actionable strategies, and editable deliverables—purchase the full SWOT analysis to inform investment, bidding, or strategic planning.

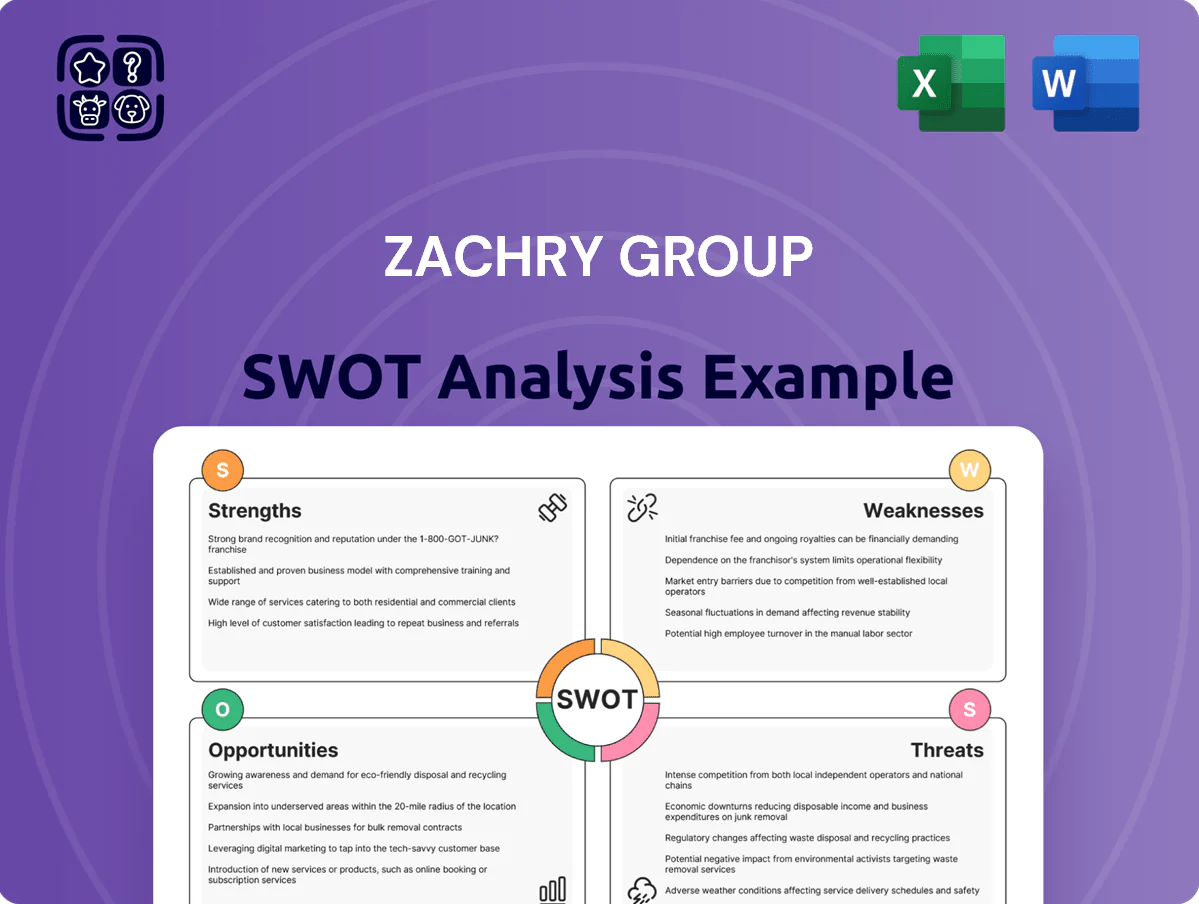

Strengths

Integrated Project Delivery Model

Zachry Group uses a turnkey model that bundles engineering, procurement, and construction, cutting third-party handoffs and saving time; in 2024 Zachry reported $3.1 billion in revenue, showing scale to run fully integrated projects.

Vertical integration improves schedule control and quality across complex industrial sites—Zachry cites repeat EPC contracts with petrochemical clients where on-time delivery rose by ~12% versus segmented teams.

Dominant Presence in US Energy Infrastructure

Zachry Group commands a strong US energy-infrastructure position, notably in the Gulf Coast where ~40% of US petrochemical capacity sits; that regional density lets Zachry leverage local crews and vendors to cut mobilization time by weeks versus national averages.

Specialized Industrial Expertise

Zachry Group’s teams hold deep technical expertise in power generation, petrochemicals, and refining, delivering over 3,500 capital projects since 2018 and $1.6B revenue in 2024 from heavy industrial services.

Engineers are noted for repairing aging infrastructure and upgrading facilities; in 2023 they completed 120 complex turnaround projects with zero major safety incidents.

This specialization makes Zachry a preferred partner for clients needing precise execution in hazardous, high-pressure environments, reflected in a repeat-business rate above 70% in 2024.

Robust Maintenance and Turnaround Services

- 25–30% of 2024 revenue from maintenance/turnarounds

- Typical contracts >5 years, improving retention

- Operational feedback reduced outage time ~15% YoY

Large Scale Skilled Labor Force

- 14,000+ direct staff (2024)

- Training reduces hiring gaps vs industry 20–30% shortfall

- 15–25% fewer accident-related downtime

- Lower insurance costs via improved safety rates

Zachry’s $3.1B EPC: 14k+ staff, 70%+ repeats, 12% faster, 15% less outage, zero major incidents

Zachry’s turnkey EPC model drove $3.1B revenue in 2024, with 14,000+ staff and 25–30% revenue from maintenance; repeat-business >70%, on-time delivery +12%, outage time down ~15% YoY, and zero major safety incidents across 120 turnarounds in 2023—anchoring Gulf Coast regional strength and lower mobilization/insurance costs.

| Metric | 2023–2024 |

|---|---|

| Revenue | $3.1B (2024) |

| Employees | 14,000+ |

| Maintenance rev | 25–30% |

| Repeat rate | >70% |

| On-time uplift | +12% |

| Outage reduction | ~15% YoY |

What is included in the product

Provides a concise SWOT overview of Zachry Group, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a concise SWOT matrix tailored to Zachry Group for quick strategic alignment and stakeholder-ready visuals.

Weaknesses

Financial Instability from Recent Restructuring

The 2024 Chapter 11 filing over the Golden Pass LNG project left Zachry Group with constrained liquidity and downgraded credit metrics into 2025; post-restructure debt fell by roughly 40% but net debt/EBITDA still ranged near 6.5x in Q3 2025, limiting capacity for new, capital-intensive bids. Rebuilding a balance sheet to fund multimillion- to billion-dollar project caps will likely take several years and slows growth.

Concentration in the United States Market

Zachry Group’s revenue is heavily US-centric—about 90% of projects in 2024 were domestic—so a US industrial slowdown or a swing in federal energy policy could cut near-term billings sharply.

Unlike multinational peers, Zachry lacks regional revenue offsets; firms with 30–50% international exposure can mute US downturns, while Zachry remains tied to US capex cycles.

Limited geographic diversification also lowers access to high-growth markets: Southeast Asia and the Middle East grew construction spending ~6–8% annually through 2024, opportunities Zachry is positioned to miss.

Exposure to Fixed Price Contract Risks

Zachry’s reliance on large fixed-price contracts shifts cost overrun risk to the firm; in 2024-25 steel and concrete input swings of 12–18% and wage inflation near 6% squeezed margins on several projects.

High-profile disputes in 2023–24 resulted in contract claims exceeding $120m industry-wide, showing how a single supply-shock could turn profitable jobs into losses.

If 2026 sees renewed inflation or supply-chain disruption, this contract mix could materially depress EBITDA and increase working capital needs.

Reputational Damage from Project Litigation

Prolonged legal battles with major partners like ExxonMobil (settlements/claims in the hundreds of millions) and QatarEnergy have dented perceptions of Zachry Group’s project management and reliability, raising concerns among owners of large upstream and LNG projects.

High-stakes disputes can deter clients who value stability; industry surveys show 42% of owners cite litigation history as a top disqualifier for EPC contractors.

Restoring trust for multi-billion-dollar ventures is a top executive priority and may require demonstrable governance changes and third-party audits within 12–18 months.

- Major partner disputes: high-profile, multi-hundred-million claims

- 42% of owners consider litigation history a disqualifier

- Fix needed: governance, audits, 12–18 month credibility rebuild

Dependency on Carbon Intensive Industries

- ~40% 2024 revenue exposure to carbon-intensive sectors

- ESG funds divested $1.1T from fossil assets in 2023–24

- Global renewables capex up 14% in 2024—shift opportunity

High leverage, US & fossil concentration, $120M+ disputes threaten post-restructure bids

Balance-sheet strain: post-restructure net debt/EBITDA ~6.5x (Q3 2025), 40% post-restructure debt cut limits new billion-dollar bids; US concentration: ~90% 2024 revenue domestic, ~40% tied to fossil fuels; contract risk: input swings 12–18% and 2023–24 claims >$120m; reputation: disputes with ExxonMobil/QatarEnergy raised owner concerns (42% cite litigation as disqualifier).

| Metric | Value |

|---|---|

| Net debt/EBITDA | ~6.5x (Q3 2025) |

| Domestic revenue | ~90% (2024) |

| Fossil exposure | ~40% (2024) |

| Claims & disputes | >$120m (2023–24) |

Same Document Delivered

Zachry Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Zachry Group’s deep engineering expertise and diversified project portfolio position it well in infrastructure and energy markets, yet exposure to cyclical construction demand and regulatory shifts are clear risks. Want the complete picture—with financial context, actionable strategies, and editable deliverables—purchase the full SWOT analysis to inform investment, bidding, or strategic planning.

Strengths

Integrated Project Delivery Model

Zachry Group uses a turnkey model that bundles engineering, procurement, and construction, cutting third-party handoffs and saving time; in 2024 Zachry reported $3.1 billion in revenue, showing scale to run fully integrated projects.

Vertical integration improves schedule control and quality across complex industrial sites—Zachry cites repeat EPC contracts with petrochemical clients where on-time delivery rose by ~12% versus segmented teams.

Dominant Presence in US Energy Infrastructure

Zachry Group commands a strong US energy-infrastructure position, notably in the Gulf Coast where ~40% of US petrochemical capacity sits; that regional density lets Zachry leverage local crews and vendors to cut mobilization time by weeks versus national averages.

Specialized Industrial Expertise

Zachry Group’s teams hold deep technical expertise in power generation, petrochemicals, and refining, delivering over 3,500 capital projects since 2018 and $1.6B revenue in 2024 from heavy industrial services.

Engineers are noted for repairing aging infrastructure and upgrading facilities; in 2023 they completed 120 complex turnaround projects with zero major safety incidents.

This specialization makes Zachry a preferred partner for clients needing precise execution in hazardous, high-pressure environments, reflected in a repeat-business rate above 70% in 2024.

Robust Maintenance and Turnaround Services

- 25–30% of 2024 revenue from maintenance/turnarounds

- Typical contracts >5 years, improving retention

- Operational feedback reduced outage time ~15% YoY

Large Scale Skilled Labor Force

- 14,000+ direct staff (2024)

- Training reduces hiring gaps vs industry 20–30% shortfall

- 15–25% fewer accident-related downtime

- Lower insurance costs via improved safety rates

Zachry’s $3.1B EPC: 14k+ staff, 70%+ repeats, 12% faster, 15% less outage, zero major incidents

Zachry’s turnkey EPC model drove $3.1B revenue in 2024, with 14,000+ staff and 25–30% revenue from maintenance; repeat-business >70%, on-time delivery +12%, outage time down ~15% YoY, and zero major safety incidents across 120 turnarounds in 2023—anchoring Gulf Coast regional strength and lower mobilization/insurance costs.

| Metric | 2023–2024 |

|---|---|

| Revenue | $3.1B (2024) |

| Employees | 14,000+ |

| Maintenance rev | 25–30% |

| Repeat rate | >70% |

| On-time uplift | +12% |

| Outage reduction | ~15% YoY |

What is included in the product

Provides a concise SWOT overview of Zachry Group, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a concise SWOT matrix tailored to Zachry Group for quick strategic alignment and stakeholder-ready visuals.

Weaknesses

Financial Instability from Recent Restructuring

The 2024 Chapter 11 filing over the Golden Pass LNG project left Zachry Group with constrained liquidity and downgraded credit metrics into 2025; post-restructure debt fell by roughly 40% but net debt/EBITDA still ranged near 6.5x in Q3 2025, limiting capacity for new, capital-intensive bids. Rebuilding a balance sheet to fund multimillion- to billion-dollar project caps will likely take several years and slows growth.

Concentration in the United States Market

Zachry Group’s revenue is heavily US-centric—about 90% of projects in 2024 were domestic—so a US industrial slowdown or a swing in federal energy policy could cut near-term billings sharply.

Unlike multinational peers, Zachry lacks regional revenue offsets; firms with 30–50% international exposure can mute US downturns, while Zachry remains tied to US capex cycles.

Limited geographic diversification also lowers access to high-growth markets: Southeast Asia and the Middle East grew construction spending ~6–8% annually through 2024, opportunities Zachry is positioned to miss.

Exposure to Fixed Price Contract Risks

Zachry’s reliance on large fixed-price contracts shifts cost overrun risk to the firm; in 2024-25 steel and concrete input swings of 12–18% and wage inflation near 6% squeezed margins on several projects.

High-profile disputes in 2023–24 resulted in contract claims exceeding $120m industry-wide, showing how a single supply-shock could turn profitable jobs into losses.

If 2026 sees renewed inflation or supply-chain disruption, this contract mix could materially depress EBITDA and increase working capital needs.

Reputational Damage from Project Litigation

Prolonged legal battles with major partners like ExxonMobil (settlements/claims in the hundreds of millions) and QatarEnergy have dented perceptions of Zachry Group’s project management and reliability, raising concerns among owners of large upstream and LNG projects.

High-stakes disputes can deter clients who value stability; industry surveys show 42% of owners cite litigation history as a top disqualifier for EPC contractors.

Restoring trust for multi-billion-dollar ventures is a top executive priority and may require demonstrable governance changes and third-party audits within 12–18 months.

- Major partner disputes: high-profile, multi-hundred-million claims

- 42% of owners consider litigation history a disqualifier

- Fix needed: governance, audits, 12–18 month credibility rebuild

Dependency on Carbon Intensive Industries

- ~40% 2024 revenue exposure to carbon-intensive sectors

- ESG funds divested $1.1T from fossil assets in 2023–24

- Global renewables capex up 14% in 2024—shift opportunity

High leverage, US & fossil concentration, $120M+ disputes threaten post-restructure bids

Balance-sheet strain: post-restructure net debt/EBITDA ~6.5x (Q3 2025), 40% post-restructure debt cut limits new billion-dollar bids; US concentration: ~90% 2024 revenue domestic, ~40% tied to fossil fuels; contract risk: input swings 12–18% and 2023–24 claims >$120m; reputation: disputes with ExxonMobil/QatarEnergy raised owner concerns (42% cite litigation as disqualifier).

| Metric | Value |

|---|---|

| Net debt/EBITDA | ~6.5x (Q3 2025) |

| Domestic revenue | ~90% (2024) |

| Fossil exposure | ~40% (2024) |

| Claims & disputes | >$120m (2023–24) |

Same Document Delivered

Zachry Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.