Zeon PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological advances are reshaping Zeon’s opportunities and risks in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to unlock detailed regulatory, environmental, and social insights, ready-to-use in presentations and decision models.

Political factors

Geopolitical Trade Tensions

Government Subsidies for EV Infrastructure

Global initiatives to phase out ICEs have driven over $500bn in EV-related subsidies worldwide through 2025, boosting EV production and battery R&D; this expansion raises demand for Zeon’s binder resins used in lithium-ion cells.

Zeon’s volumes and pricing exposure hinge on the scale and stability of such incentives—e.g., the EU’s Fit for 55 and US CHIPS/IRA allocations that expanded battery manufacturing capacity by an estimated 35% from 2021–2024.

Political turnover risks policy reversals: a 10–20% swing in subsidy intensity could materially alter Zeon’s multi-year demand forecasts and capital planning for capacity expansions.

Chemical Safety Regulations and Policy

Political pressure is driving stricter chemical safety oversight, with REACH-like regimes expanding in Asia; REACH alone regulates 22,000 substances and recent EU amendments (2023–2025) tightened registrant data requirements, raising compliance costs by an estimated 10–20% for specialty-chemical makers.

Such frameworks extend approval timelines—industry surveys show average time-to-market for novel specialty polymers rises from 18 to 30 months under enhanced scrutiny—impacting Zeon’s product rollout and revenue recognition.

Active engagement with regulators is essential: firms investing in regulatory affairs see 5–8% faster approvals; Zeon must allocate resources to policy dialogue and compliance to protect margins and sustain competitive advantage.

Energy Security and Industrial Policy

National energy-independence policies raise domestic feedstock sourcing costs; naphtha and LPG prices rose 18% YoY in 2024, squeezing margins for petrochemical feedstocks used in synthetic rubber production.

Political instability in Middle East and Russia caused Brent volatility (2024 range $64–$96/bbl), transmitting feedstock price swings that compressed Zeon’s synthetic rubber margins by an estimated 150–250 bps in 2024.

Governments boosted domestic chemical capacity—Japan allocated ¥300bn (2024–25) for industrial resilience—creating procurement opportunities for Zeon but increasing competition from subsidized local players.

- Feedstock price impact: +18% naphtha/LPG (2024)

- Oil volatility: Brent $64–$96/bbl (2024)

- Margin hit: ~150–250 bps (2024)

- Policy support: Japan ¥300bn industrial fund (2024–25)

International Relations and Market Access

Diplomatic relations between Japan and key partners determine Zeon’s market access; in 2024 Japan’s FTAs covered 30% of its trade, easing specialty chemical exports and supporting Zeon’s ¥220 billion overseas revenue in FY2023.

FTA benefits contrast with risks from diplomatic friction—non-tariff barriers or boycotts can disrupt supply and sales, as seen in regional trade disruptions that reduced chemical exports by up to 8% in 2022–23.

Maintaining diversified global operations—Asia, North America, and Europe—helps Zeon offset localized instability and foreign-policy shifts that could affect up to 40% of regional revenue.

- FTAs expand market access; Japan FTAs = ~30% of trade (2024)

- Zeon overseas revenue ≈ ¥220bn (FY2023)

- Regional trade disruptions cut chemical exports by ~8% (2022–23)

- ~40% of revenue potentially exposed to regional policy shifts

Trade tariffs squeeze Zeon margins as EV boom and Japan support offset headwinds

US-China trade measures and tariffs (up to 25%) raised feedstock costs ~12% in 2024, squeezing Zeon’s margins (150–250 bps); EV subsidies (>$500bn through 2025) lifted battery demand ~35% (2021–24), aiding binder resin sales; REACH-style rules increased compliance costs 10–20% and extended time-to-market to ~30 months; Japan’s ¥300bn industrial fund and FTAs (30% trade) support ¥220bn FY2023 overseas revenue.

| Metric | 2024/2023 Value |

|---|---|

| Feedstock cost rise | +12% |

| Tariffs on intermediates | up to 25% |

| Margin impact | 150–250 bps |

| EV subsidies through 2025 | >$500bn |

| Battery capacity growth | +35% (2021–24) |

| Compliance cost rise | 10–20% |

| Japan industrial fund | ¥300bn (2024–25) |

| Zeon overseas revenue | ¥220bn (FY2023) |

What is included in the product

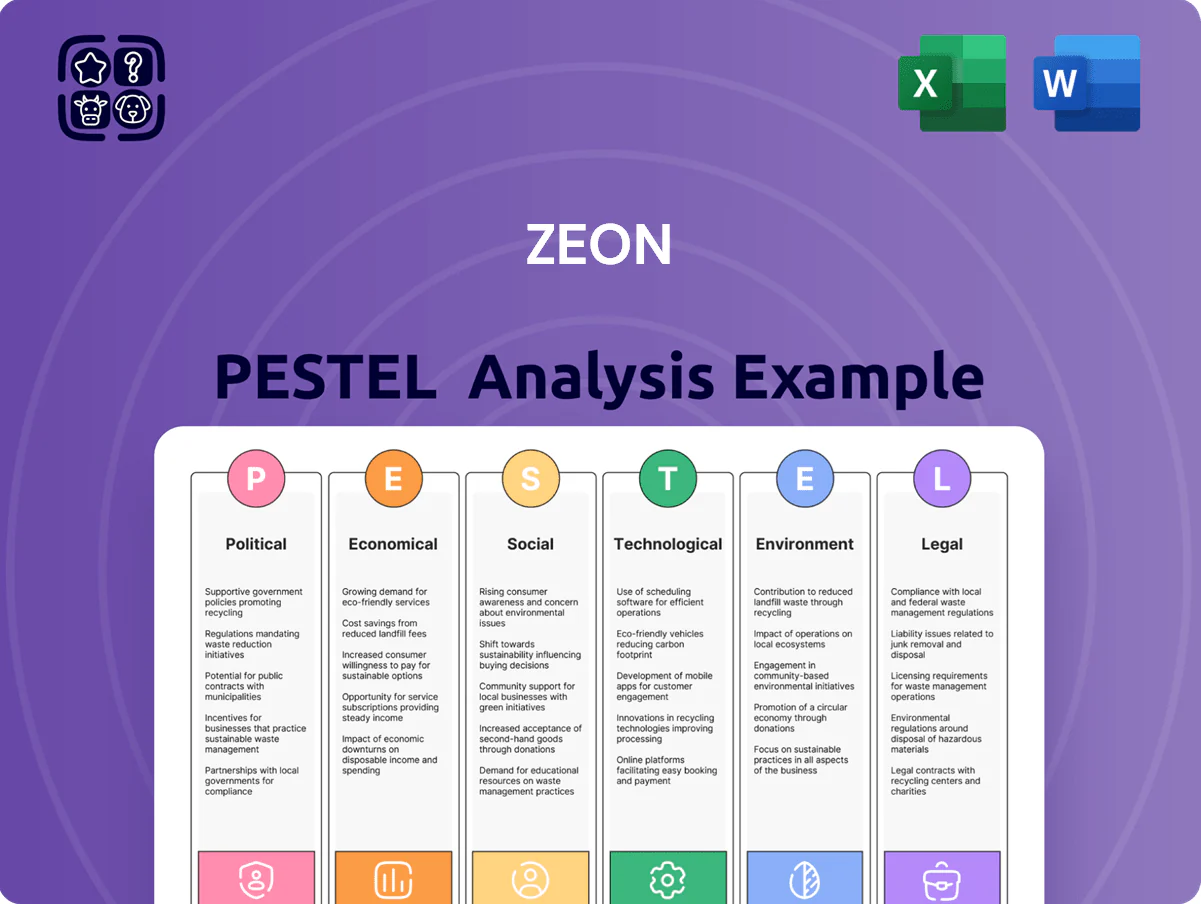

Explores how external macro-environmental factors uniquely affect Zeon across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

Provides a concise, shareable PESTLE summary of Zeon that’s visually segmented for quick interpretation and easily dropped into presentations or strategy packs to streamline risk discussions and team alignment.

Economic factors

Fluctuations in Raw Material Costs

The price of naphtha and petroleum feedstocks drives Zeon’s production costs—naphtha rose ~45% from 2020–2022 and averaged about $700/ton in 2024, pressuring margins; Zeon uses hedging (forwards, swaps) and flexible pricing to protect EBITDA, which fell to 6.8% in FY2023 from 9.2% in FY2021; prolonged high oil and energy prices, with global Brent averaging ~$85–95/bbl in 2024, can cut consumer disposable income and dampen demand for premium electronics and autos.

Global Exchange Rate Volatility

As a Japan-headquartered chemicals firm with ~60% revenue outside Japan, Zeon is exposed to JPY/USD and JPY/EUR swings; the Yen fell ~8% vs USD in 2023 then strengthened ~6% in 2024, amplifying reporting volatility. A weaker Yen boosts export price competitiveness but raised imported feedstock costs—Japan monthly CPI-linked commodity import costs rose ~12% YoY in 2023. Hedging and local production remain key: Zeon reported FX derivatives covering ~40% of anticipated 12-month net exposures in FY2024.

Interest Rate Trends and Capital Expenditure

Global central banks lifted policy rates in 2022–24; the BOJ moved to normalize policy and the US Fed funds rate peaked near 5.25–5.50% in 2023–24, raising corporate borrowing costs and pushing average investment-grade yields up ~150–250 bps versus 2021, which increases financing costs for Zeon’s large-scale R&D and plant expansions.

Higher borrowing costs have prompted many specialty chemical peers to defer or scale back CAPEX; industry CAPEX-to-sales ratios fell ~10–15% in 2023, indicating a more cautious stance likely to affect Zeon’s timing for long-term projects.

To fund its technological roadmap without eroding investor appeal, Zeon must manage debt-to-equity—keeping leverage near industry medians (roughly 0.6–0.8 net debt/EBITDA for specialty chemicals in 2024) to maintain credit metrics and financing access.

Growth of the Electric Vehicle Market

The shift to electrification offers Zeon’s battery materials division significant upside: global EV sales reached 14 million in 2023 and are projected at ~21–25 million by 2025, boosting demand for binders and separators as battery costs fell ~15%/year (2020–2024) to below $120/kWh in 2024.

However, economic downturns can compress vehicle purchases—global auto sales dropped ~8% in 2020 and similar shocks could delay EV uptake, stalling short-term volumes for automotive materials.

- EV sales: 14M (2023); est. 21–25M (2025)

- Battery cost: ~<$120/kWh (2024); −15%/yr (2020–24)

- Volume upside: higher binder/separator demand

- Risk: recessions can cause temporary −% declines in auto purchases

Inflationary Pressures on Operational Costs

Rising labor costs—average wage growth of 4.5%–6% in key markets in 2024—and logistics inflation (+12% year-on-year for container freight in 2024) squeeze Zeon’s margins, requiring investment in automation and lean processes to preserve operational efficiency and competitive pricing.

Persistent inflation in Japan (core CPI ~3% in 2024) and other core markets can shift demand toward lower-cost polymer alternatives, forcing Zeon to prioritize cost-down product lines and process optimization to retain customers.

- Wage growth 4.5%–6% (2024)

- Container freight +12% YoY (2024)

- Japan core CPI ~3% (2024)

- Actions: automation, lean/process optimization

High feedstock, energy and rates squeeze margins — EV boom fuels battery-materials upside

High feedstock costs (naphtha ~$700/t in 2024) and energy (Brent ~$85–95/bbl) compress margins; FX volatility (JPY −8% vs USD in 2023, +6% in 2024) affects costs and reporting; higher rates raise borrowing costs (IG yields +150–250bps vs 2021) constraining CAPEX; EV demand (14M EVs in 2023 → est. 21–25M in 2025) supports battery materials upside.

| Metric | 2024/2025 |

|---|---|

| Naphtha | $700/t (2024) |

| Brent | $85–95/bbl (2024) |

| EV sales | 14M (2023) → 21–25M (2025 est.) |

Full Version Awaits

Zeon PESTLE Analysis

The preview shown here is the exact Zeon PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological advances are reshaping Zeon’s opportunities and risks in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to unlock detailed regulatory, environmental, and social insights, ready-to-use in presentations and decision models.

Political factors

Geopolitical Trade Tensions

Government Subsidies for EV Infrastructure

Global initiatives to phase out ICEs have driven over $500bn in EV-related subsidies worldwide through 2025, boosting EV production and battery R&D; this expansion raises demand for Zeon’s binder resins used in lithium-ion cells.

Zeon’s volumes and pricing exposure hinge on the scale and stability of such incentives—e.g., the EU’s Fit for 55 and US CHIPS/IRA allocations that expanded battery manufacturing capacity by an estimated 35% from 2021–2024.

Political turnover risks policy reversals: a 10–20% swing in subsidy intensity could materially alter Zeon’s multi-year demand forecasts and capital planning for capacity expansions.

Chemical Safety Regulations and Policy

Political pressure is driving stricter chemical safety oversight, with REACH-like regimes expanding in Asia; REACH alone regulates 22,000 substances and recent EU amendments (2023–2025) tightened registrant data requirements, raising compliance costs by an estimated 10–20% for specialty-chemical makers.

Such frameworks extend approval timelines—industry surveys show average time-to-market for novel specialty polymers rises from 18 to 30 months under enhanced scrutiny—impacting Zeon’s product rollout and revenue recognition.

Active engagement with regulators is essential: firms investing in regulatory affairs see 5–8% faster approvals; Zeon must allocate resources to policy dialogue and compliance to protect margins and sustain competitive advantage.

Energy Security and Industrial Policy

National energy-independence policies raise domestic feedstock sourcing costs; naphtha and LPG prices rose 18% YoY in 2024, squeezing margins for petrochemical feedstocks used in synthetic rubber production.

Political instability in Middle East and Russia caused Brent volatility (2024 range $64–$96/bbl), transmitting feedstock price swings that compressed Zeon’s synthetic rubber margins by an estimated 150–250 bps in 2024.

Governments boosted domestic chemical capacity—Japan allocated ¥300bn (2024–25) for industrial resilience—creating procurement opportunities for Zeon but increasing competition from subsidized local players.

- Feedstock price impact: +18% naphtha/LPG (2024)

- Oil volatility: Brent $64–$96/bbl (2024)

- Margin hit: ~150–250 bps (2024)

- Policy support: Japan ¥300bn industrial fund (2024–25)

International Relations and Market Access

Diplomatic relations between Japan and key partners determine Zeon’s market access; in 2024 Japan’s FTAs covered 30% of its trade, easing specialty chemical exports and supporting Zeon’s ¥220 billion overseas revenue in FY2023.

FTA benefits contrast with risks from diplomatic friction—non-tariff barriers or boycotts can disrupt supply and sales, as seen in regional trade disruptions that reduced chemical exports by up to 8% in 2022–23.

Maintaining diversified global operations—Asia, North America, and Europe—helps Zeon offset localized instability and foreign-policy shifts that could affect up to 40% of regional revenue.

- FTAs expand market access; Japan FTAs = ~30% of trade (2024)

- Zeon overseas revenue ≈ ¥220bn (FY2023)

- Regional trade disruptions cut chemical exports by ~8% (2022–23)

- ~40% of revenue potentially exposed to regional policy shifts

Trade tariffs squeeze Zeon margins as EV boom and Japan support offset headwinds

US-China trade measures and tariffs (up to 25%) raised feedstock costs ~12% in 2024, squeezing Zeon’s margins (150–250 bps); EV subsidies (>$500bn through 2025) lifted battery demand ~35% (2021–24), aiding binder resin sales; REACH-style rules increased compliance costs 10–20% and extended time-to-market to ~30 months; Japan’s ¥300bn industrial fund and FTAs (30% trade) support ¥220bn FY2023 overseas revenue.

| Metric | 2024/2023 Value |

|---|---|

| Feedstock cost rise | +12% |

| Tariffs on intermediates | up to 25% |

| Margin impact | 150–250 bps |

| EV subsidies through 2025 | >$500bn |

| Battery capacity growth | +35% (2021–24) |

| Compliance cost rise | 10–20% |

| Japan industrial fund | ¥300bn (2024–25) |

| Zeon overseas revenue | ¥220bn (FY2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Zeon across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

Provides a concise, shareable PESTLE summary of Zeon that’s visually segmented for quick interpretation and easily dropped into presentations or strategy packs to streamline risk discussions and team alignment.

Economic factors

Fluctuations in Raw Material Costs

The price of naphtha and petroleum feedstocks drives Zeon’s production costs—naphtha rose ~45% from 2020–2022 and averaged about $700/ton in 2024, pressuring margins; Zeon uses hedging (forwards, swaps) and flexible pricing to protect EBITDA, which fell to 6.8% in FY2023 from 9.2% in FY2021; prolonged high oil and energy prices, with global Brent averaging ~$85–95/bbl in 2024, can cut consumer disposable income and dampen demand for premium electronics and autos.

Global Exchange Rate Volatility

As a Japan-headquartered chemicals firm with ~60% revenue outside Japan, Zeon is exposed to JPY/USD and JPY/EUR swings; the Yen fell ~8% vs USD in 2023 then strengthened ~6% in 2024, amplifying reporting volatility. A weaker Yen boosts export price competitiveness but raised imported feedstock costs—Japan monthly CPI-linked commodity import costs rose ~12% YoY in 2023. Hedging and local production remain key: Zeon reported FX derivatives covering ~40% of anticipated 12-month net exposures in FY2024.

Interest Rate Trends and Capital Expenditure

Global central banks lifted policy rates in 2022–24; the BOJ moved to normalize policy and the US Fed funds rate peaked near 5.25–5.50% in 2023–24, raising corporate borrowing costs and pushing average investment-grade yields up ~150–250 bps versus 2021, which increases financing costs for Zeon’s large-scale R&D and plant expansions.

Higher borrowing costs have prompted many specialty chemical peers to defer or scale back CAPEX; industry CAPEX-to-sales ratios fell ~10–15% in 2023, indicating a more cautious stance likely to affect Zeon’s timing for long-term projects.

To fund its technological roadmap without eroding investor appeal, Zeon must manage debt-to-equity—keeping leverage near industry medians (roughly 0.6–0.8 net debt/EBITDA for specialty chemicals in 2024) to maintain credit metrics and financing access.

Growth of the Electric Vehicle Market

The shift to electrification offers Zeon’s battery materials division significant upside: global EV sales reached 14 million in 2023 and are projected at ~21–25 million by 2025, boosting demand for binders and separators as battery costs fell ~15%/year (2020–2024) to below $120/kWh in 2024.

However, economic downturns can compress vehicle purchases—global auto sales dropped ~8% in 2020 and similar shocks could delay EV uptake, stalling short-term volumes for automotive materials.

- EV sales: 14M (2023); est. 21–25M (2025)

- Battery cost: ~<$120/kWh (2024); −15%/yr (2020–24)

- Volume upside: higher binder/separator demand

- Risk: recessions can cause temporary −% declines in auto purchases

Inflationary Pressures on Operational Costs

Rising labor costs—average wage growth of 4.5%–6% in key markets in 2024—and logistics inflation (+12% year-on-year for container freight in 2024) squeeze Zeon’s margins, requiring investment in automation and lean processes to preserve operational efficiency and competitive pricing.

Persistent inflation in Japan (core CPI ~3% in 2024) and other core markets can shift demand toward lower-cost polymer alternatives, forcing Zeon to prioritize cost-down product lines and process optimization to retain customers.

- Wage growth 4.5%–6% (2024)

- Container freight +12% YoY (2024)

- Japan core CPI ~3% (2024)

- Actions: automation, lean/process optimization

High feedstock, energy and rates squeeze margins — EV boom fuels battery-materials upside

High feedstock costs (naphtha ~$700/t in 2024) and energy (Brent ~$85–95/bbl) compress margins; FX volatility (JPY −8% vs USD in 2023, +6% in 2024) affects costs and reporting; higher rates raise borrowing costs (IG yields +150–250bps vs 2021) constraining CAPEX; EV demand (14M EVs in 2023 → est. 21–25M in 2025) supports battery materials upside.

| Metric | 2024/2025 |

|---|---|

| Naphtha | $700/t (2024) |

| Brent | $85–95/bbl (2024) |

| EV sales | 14M (2023) → 21–25M (2025 est.) |

Full Version Awaits

Zeon PESTLE Analysis

The preview shown here is the exact Zeon PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.