Zhejiang Zheneng Electric Power Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

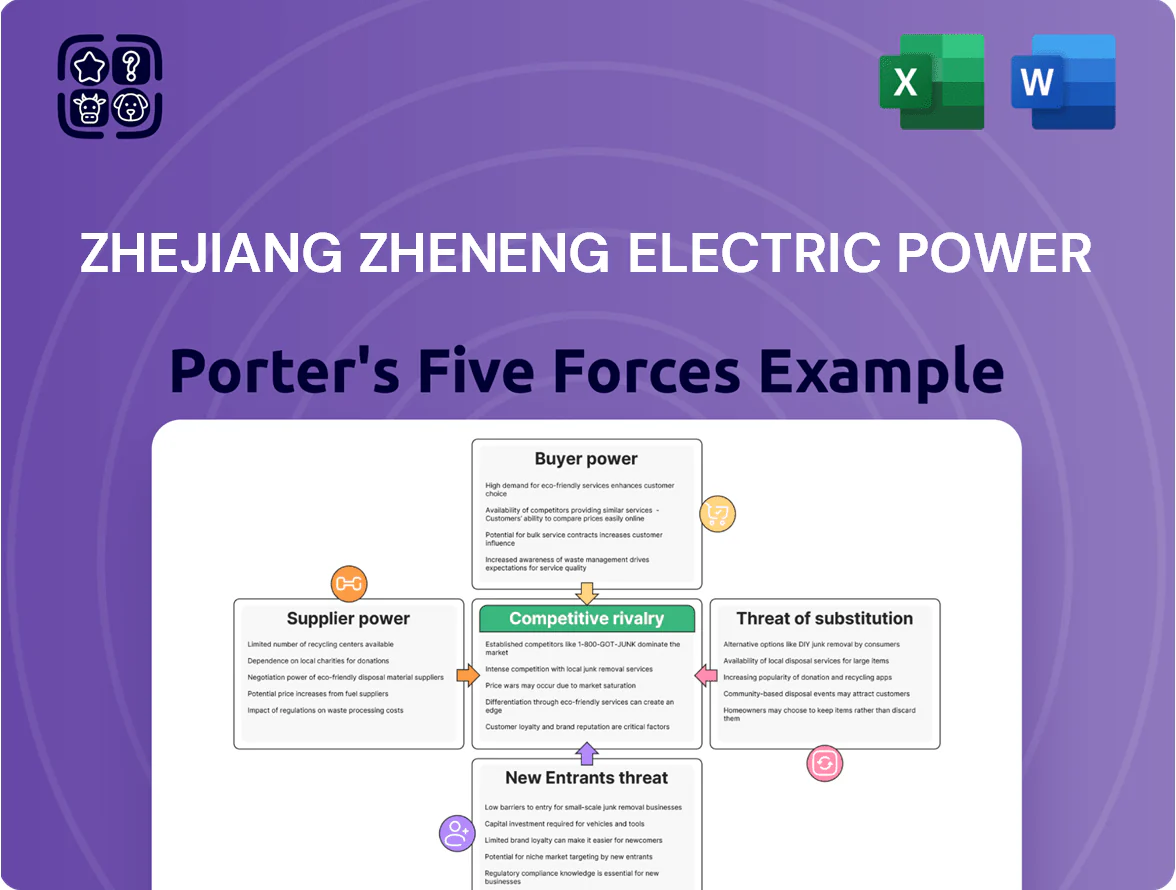

Zhejiang Zheneng Electric Power faces moderate buyer power, regulated pricing and high capital intensity that limit new entrants, while supplier power is elevated for fuel and equipment; competitive rivalry hinges on scale, efficiency, and renewable transition strategies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Zhejiang Zheneng Electric Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Coal Commodity Price Volatility

As a primary thermal power producer, Zhejiang Zheneng Electric Power is highly sensitive to raw coal prices, which rose ~12% YoY in 2024 and averaged RMB 900/ton in H1 2025, driven by global cycles and variable domestic mining output.

Long-term contracts with state-owned miners cover ~60% of demand, cushioning short-term swings, but supply shocks or port-logistics bottlenecks can cut EBITDA margins by 3–5 percentage points.

By late 2025, a shift toward market-based coal pricing increased bargaining power for large miners, raising spot-price exposure and short-term procurement costs for generators.

Dependence on Specialized Equipment Manufacturers

Procurement of high-efficiency turbines, boilers, and SCR emission systems ties Zhejiang Zheneng to a few global and Chinese OEMs (e.g., GE, Siemens, Harbin Electric), giving suppliers moderate bargaining power because equipment is specialized and switching raises maintenance and proprietary-software costs; replacing a 600 MW turbine can cost ~RMB 400–700m and retrofit SCRs ~RMB 50–120m, so Zheneng must balance partner terms to keep tech parity and control capex.

Impact of Carbon Credit Markets

The national carbon trading scheme (launched 2021) makes regulators primary suppliers of emission rights; with China tightening quotas toward 2026, permit prices rose ~45% in 2024 to ~CNY 80/ton, raising Zheneng’s offset costs materially. Suppliers of green certificates can demand higher premiums as available allowances shrink, so Zheneng must negotiate under stricter supply and rising-cost conditions that compress margins and raise compliance spending.

Logistics and Transportation Infrastructure

Reliance on rail and maritime coal delivery gives transport monopolies and port operators strong leverage; Zhejiang handled 1.2 billion tonnes of coastal cargo in 2024, so freight swings hit landed fuel cost directly.

Zhejiang Zheneng reduced exposure by building private logistics capacity—own terminals handling ~18% of inbound coal in 2025—but third-party rail and shipping providers still set key prices and schedules.

- Coastal cargo 2024: 1.2B t

- Own terminals handle ~18% (2025)

- Freight hikes directly raise landed coal cost

- Rail/port operators retain pricing power

Technological Integration for Renewables

As Zhejiang Zheneng Electric Power expands into wind and solar, suppliers of semiconductors and rare-earth metals (highly concentrated; top 3 firms control ~70% of rare-earth processing in China) hold strong pricing power, raising input cost risk for 2025–2026 integration.

Securing PV cells and turbine components is critical: missed deliveries or 10–20% price hikes could delay meeting renewables capacity targets set for 2025 and 2026.

- High supplier concentration: top 3 ≈70% rare-earth processing

- Price shock risk: potential 10–20% input cost spikes

- Key need: long-term contracts, diversified sourcing, inventory buffers

Rising coal and carbon costs + supplier concentration squeeze margins

Suppliers exert moderate-to-high power: coal price volatility (avg RMB900/t H1 2025; +12% YoY 2024) and rail/port leverage raise landed costs; long-term contracts cover ~60% coal need; own terminals handle ~18% inbound coal (2025). OEMs and rare-earth/top-3 processors (~70% share) add tech and input concentration risk; carbon permit price ~CNY80/t (2024, +45% YoY) increases compliance costs.

| Metric | Value |

|---|---|

| Coal price H1 2025 | RMB900/t |

| Coal contracts covered | ~60% |

| Own terminals | ~18% |

| Carbon price 2024 | CNY80/t (+45%) |

| Rare-earth top-3 | ~70% |

What is included in the product

Tailored exclusively for Zhejiang Zheneng Electric Power, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats affecting its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot tailored to Zhejiang Zheneng Electric Power—quickly spot bargaining power, competitive threats, and regulatory pressure to streamline strategic decisions.

Customers Bargaining Power

Monopsony Power of the State Grid

The State Grid Corporation of China is the dominant buyer for Zhejiang Zheneng Electric Power, creating a monopsony-like market that caps the company’s pricing power and negotiation leverage.

Despite reforms since 2015 and pilot spot-market expansions, over 70% of provincial dispatch and tariff decisions in Zhejiang remained regulated in 2024, limiting Zheneng’s ability to capture short-term price spikes.

This yields revenue stability—Zheneng sold roughly 38 TWh to State Grid in 2024—but foregoes upside during peak demand when market prices can exceed regulated tariffs by 10–30%.

Direct Power Purchase Agreements

Large Zhejiang industrial users can now sign direct power purchase agreements (PPAs) with generators, shifting bargaining power toward buyers; in 2024 about 18% of provincial industrial demand (≈28 TWh) was covered by direct contracts, raising buyer leverage.

High-volume customers can switch on price and carbon: a 2025 survey showed 62% of manufacturers prioritize low-carbon tariffs, so switching costs are low and price sensitivity is high.

To retain them Zheneng must match market rates (wholesale margins under 6% in 2024) and add energy-management services—real-time load control and green-certificates—to differentiate from regional rivals.

Heating Market Sensitivity

Zhejiang Zheneng Electric Power’s heating arm serves nearby industrial parks and residential districts where price sensitivity is high; in Zhejiang province household heating tariffs are often capped by local governments, limiting pass-through of fuel cost rises. In 2024 Zhejiang reported a 12% jump in coal-to-heat feedstock prices, yet municipal caps kept end-user rates largely unchanged, forcing Zheneng to absorb margin pressure to meet social-stability and public-service obligations.

Demand for Green Energy Certificates

Corporate buyers now demand electricity paired with Green Electricity Certificates to meet ESG targets and EU/US export rules, boosting their bargaining power over Zhejiang Zheneng Electric Power.

This trend forces faster decarbonization: by 2024 corporate offtake for certified green power rose ~18% YoY in China, so failure to supply verifiable green energy risks losing high-margin contracts to cleaner rivals.

- 2024: corporate green power demand +18% YoY

- Loss risk: high-margin contracts shift to low-carbon suppliers

- Action: accelerate verified RE and certificate issuance

Regional Economic Fluctuations

- Export exposure: high; Zhejiang exports ~18% of provincial GDP (2023).

- Industrial output signal: PMI below 50 → lower demand.

- Tariff risk: 6–12% demand swings affect margins.

- Action: monthly macro + load monitoring to manage buyers.

Zheneng squeezed: State Grid buys 38TWh, PPAs 28TWh, margins under 6%

State Grid dominates buying—Zheneng sold ~38 TWh to State Grid in 2024—limiting price upside despite spot-market pilots; direct industrial PPAs covered ≈28 TWh (18% provincial demand) in 2024, raising buyer leverage. Corporate green demand grew ~18% YoY (2024), pushing Zheneng to supply certified RE or lose high-margin contracts; wholesale margins averaged <6% in 2024.

| Metric | 2024 value |

|---|---|

| Sales to State Grid | 38 TWh |

| Industrial PPAs | 28 TWh (18%) |

| Corporate green demand YoY | +18% |

| Wholesale margin | <6% |

What You See Is What You Get

Zhejiang Zheneng Electric Power Porter's Five Forces Analysis

This preview shows the exact Zhejiang Zheneng Electric Power Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it includes supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry assessed with industry data.

The document displayed here is the part of the full version you’ll get—fully formatted, ready for download and use the moment you buy, with concise strategic implications and suggested actions for stakeholders.

You're looking at the actual, professionally written analysis file. Once you complete your purchase, you’ll get instant access to this exact document—ready for presentation, decision-making, or integration into reports.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Zhejiang Zheneng Electric Power faces moderate buyer power, regulated pricing and high capital intensity that limit new entrants, while supplier power is elevated for fuel and equipment; competitive rivalry hinges on scale, efficiency, and renewable transition strategies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Zhejiang Zheneng Electric Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Coal Commodity Price Volatility

As a primary thermal power producer, Zhejiang Zheneng Electric Power is highly sensitive to raw coal prices, which rose ~12% YoY in 2024 and averaged RMB 900/ton in H1 2025, driven by global cycles and variable domestic mining output.

Long-term contracts with state-owned miners cover ~60% of demand, cushioning short-term swings, but supply shocks or port-logistics bottlenecks can cut EBITDA margins by 3–5 percentage points.

By late 2025, a shift toward market-based coal pricing increased bargaining power for large miners, raising spot-price exposure and short-term procurement costs for generators.

Dependence on Specialized Equipment Manufacturers

Procurement of high-efficiency turbines, boilers, and SCR emission systems ties Zhejiang Zheneng to a few global and Chinese OEMs (e.g., GE, Siemens, Harbin Electric), giving suppliers moderate bargaining power because equipment is specialized and switching raises maintenance and proprietary-software costs; replacing a 600 MW turbine can cost ~RMB 400–700m and retrofit SCRs ~RMB 50–120m, so Zheneng must balance partner terms to keep tech parity and control capex.

Impact of Carbon Credit Markets

The national carbon trading scheme (launched 2021) makes regulators primary suppliers of emission rights; with China tightening quotas toward 2026, permit prices rose ~45% in 2024 to ~CNY 80/ton, raising Zheneng’s offset costs materially. Suppliers of green certificates can demand higher premiums as available allowances shrink, so Zheneng must negotiate under stricter supply and rising-cost conditions that compress margins and raise compliance spending.

Logistics and Transportation Infrastructure

Reliance on rail and maritime coal delivery gives transport monopolies and port operators strong leverage; Zhejiang handled 1.2 billion tonnes of coastal cargo in 2024, so freight swings hit landed fuel cost directly.

Zhejiang Zheneng reduced exposure by building private logistics capacity—own terminals handling ~18% of inbound coal in 2025—but third-party rail and shipping providers still set key prices and schedules.

- Coastal cargo 2024: 1.2B t

- Own terminals handle ~18% (2025)

- Freight hikes directly raise landed coal cost

- Rail/port operators retain pricing power

Technological Integration for Renewables

As Zhejiang Zheneng Electric Power expands into wind and solar, suppliers of semiconductors and rare-earth metals (highly concentrated; top 3 firms control ~70% of rare-earth processing in China) hold strong pricing power, raising input cost risk for 2025–2026 integration.

Securing PV cells and turbine components is critical: missed deliveries or 10–20% price hikes could delay meeting renewables capacity targets set for 2025 and 2026.

- High supplier concentration: top 3 ≈70% rare-earth processing

- Price shock risk: potential 10–20% input cost spikes

- Key need: long-term contracts, diversified sourcing, inventory buffers

Rising coal and carbon costs + supplier concentration squeeze margins

Suppliers exert moderate-to-high power: coal price volatility (avg RMB900/t H1 2025; +12% YoY 2024) and rail/port leverage raise landed costs; long-term contracts cover ~60% coal need; own terminals handle ~18% inbound coal (2025). OEMs and rare-earth/top-3 processors (~70% share) add tech and input concentration risk; carbon permit price ~CNY80/t (2024, +45% YoY) increases compliance costs.

| Metric | Value |

|---|---|

| Coal price H1 2025 | RMB900/t |

| Coal contracts covered | ~60% |

| Own terminals | ~18% |

| Carbon price 2024 | CNY80/t (+45%) |

| Rare-earth top-3 | ~70% |

What is included in the product

Tailored exclusively for Zhejiang Zheneng Electric Power, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats affecting its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot tailored to Zhejiang Zheneng Electric Power—quickly spot bargaining power, competitive threats, and regulatory pressure to streamline strategic decisions.

Customers Bargaining Power

Monopsony Power of the State Grid

The State Grid Corporation of China is the dominant buyer for Zhejiang Zheneng Electric Power, creating a monopsony-like market that caps the company’s pricing power and negotiation leverage.

Despite reforms since 2015 and pilot spot-market expansions, over 70% of provincial dispatch and tariff decisions in Zhejiang remained regulated in 2024, limiting Zheneng’s ability to capture short-term price spikes.

This yields revenue stability—Zheneng sold roughly 38 TWh to State Grid in 2024—but foregoes upside during peak demand when market prices can exceed regulated tariffs by 10–30%.

Direct Power Purchase Agreements

Large Zhejiang industrial users can now sign direct power purchase agreements (PPAs) with generators, shifting bargaining power toward buyers; in 2024 about 18% of provincial industrial demand (≈28 TWh) was covered by direct contracts, raising buyer leverage.

High-volume customers can switch on price and carbon: a 2025 survey showed 62% of manufacturers prioritize low-carbon tariffs, so switching costs are low and price sensitivity is high.

To retain them Zheneng must match market rates (wholesale margins under 6% in 2024) and add energy-management services—real-time load control and green-certificates—to differentiate from regional rivals.

Heating Market Sensitivity

Zhejiang Zheneng Electric Power’s heating arm serves nearby industrial parks and residential districts where price sensitivity is high; in Zhejiang province household heating tariffs are often capped by local governments, limiting pass-through of fuel cost rises. In 2024 Zhejiang reported a 12% jump in coal-to-heat feedstock prices, yet municipal caps kept end-user rates largely unchanged, forcing Zheneng to absorb margin pressure to meet social-stability and public-service obligations.

Demand for Green Energy Certificates

Corporate buyers now demand electricity paired with Green Electricity Certificates to meet ESG targets and EU/US export rules, boosting their bargaining power over Zhejiang Zheneng Electric Power.

This trend forces faster decarbonization: by 2024 corporate offtake for certified green power rose ~18% YoY in China, so failure to supply verifiable green energy risks losing high-margin contracts to cleaner rivals.

- 2024: corporate green power demand +18% YoY

- Loss risk: high-margin contracts shift to low-carbon suppliers

- Action: accelerate verified RE and certificate issuance

Regional Economic Fluctuations

- Export exposure: high; Zhejiang exports ~18% of provincial GDP (2023).

- Industrial output signal: PMI below 50 → lower demand.

- Tariff risk: 6–12% demand swings affect margins.

- Action: monthly macro + load monitoring to manage buyers.

Zheneng squeezed: State Grid buys 38TWh, PPAs 28TWh, margins under 6%

State Grid dominates buying—Zheneng sold ~38 TWh to State Grid in 2024—limiting price upside despite spot-market pilots; direct industrial PPAs covered ≈28 TWh (18% provincial demand) in 2024, raising buyer leverage. Corporate green demand grew ~18% YoY (2024), pushing Zheneng to supply certified RE or lose high-margin contracts; wholesale margins averaged <6% in 2024.

| Metric | 2024 value |

|---|---|

| Sales to State Grid | 38 TWh |

| Industrial PPAs | 28 TWh (18%) |

| Corporate green demand YoY | +18% |

| Wholesale margin | <6% |

What You See Is What You Get

Zhejiang Zheneng Electric Power Porter's Five Forces Analysis

This preview shows the exact Zhejiang Zheneng Electric Power Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it includes supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry assessed with industry data.

The document displayed here is the part of the full version you’ll get—fully formatted, ready for download and use the moment you buy, with concise strategic implications and suggested actions for stakeholders.

You're looking at the actual, professionally written analysis file. Once you complete your purchase, you’ll get instant access to this exact document—ready for presentation, decision-making, or integration into reports.