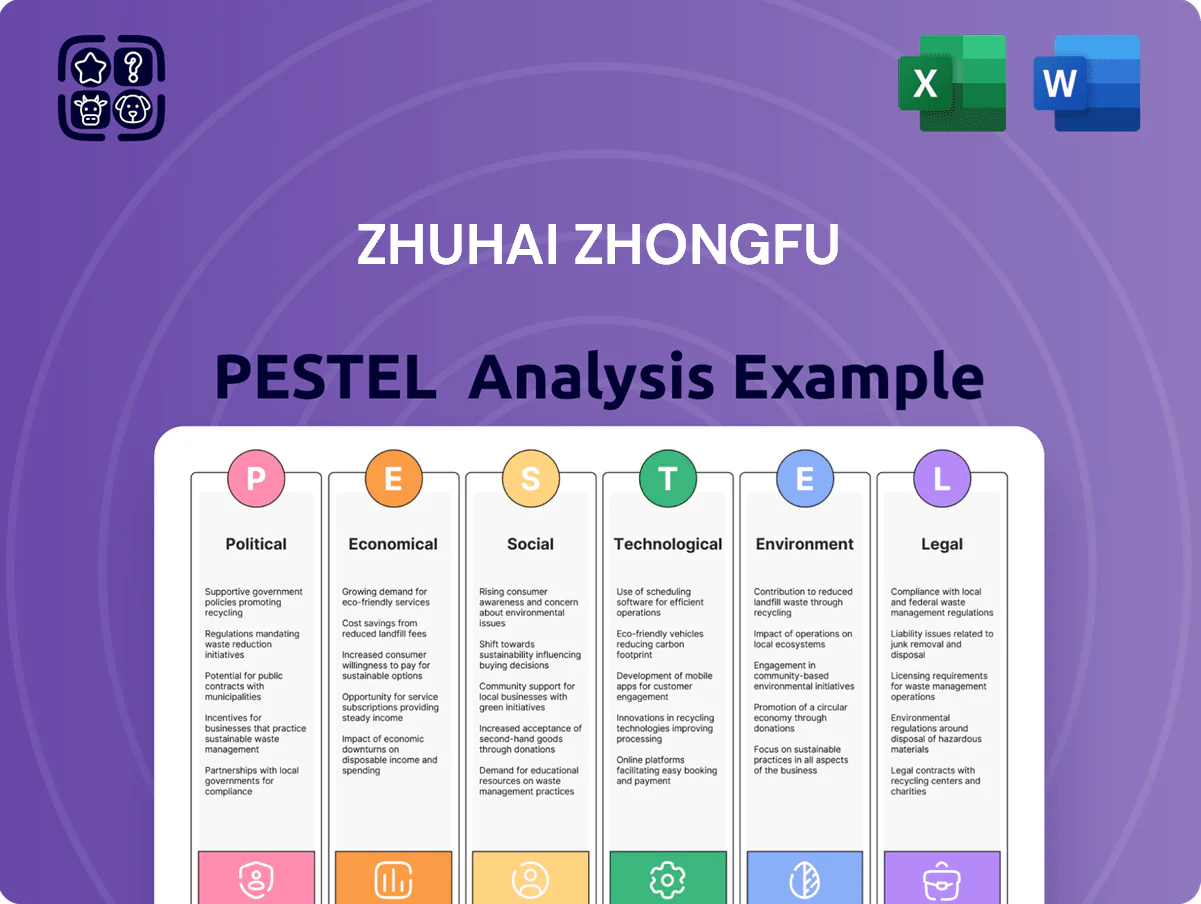

Zhuhai Zhongfu PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Explore how political shifts, economic cycles, and technological change are reshaping Zhuhai Zhongfu’s strategic landscape—our concise PESTLE highlights key risks and opportunities to inform smarter decisions. Purchase the full analysis for a complete, editable report with actionable insights and market-ready recommendations.

Political factors

Government industrial modernization initiatives

The Made in China 2025 drive, now in its final evaluation phase, channels provincial and central funding toward upgrading manufacturing; Guangdong received RMB 48.6 billion in 2024 industrial transformation grants, benefiting Zhuhai Zhongfu's packaging equipment and advanced materials lines. State programs prioritize high-end equipment and materials, with Zhongfu obtaining subsidies covering up to 20% of qualifying capex and R&D tax credits reducing effective rates by ~10 percentage points. Policies also fund smart manufacturing: Guangdong rolled out RMB 7.2 billion for digital transformation in 2024, enabling Zhongfu to integrate IoT and automation that cut unit labor costs by ~12% year-on-year.

Trade relations and export stability

Ongoing trade tensions between China and Western economies push Zhuhai Zhongfu to pivot toward domestic demand and RCEP markets, which accounted for 42% of China’s PET exports in 2024; this reduces exposure to US/EU tariffs that rose intermittently in 2023–2025. As of late 2025 the firm faces fluctuating raw material and finished-PET tariffs and input-cost volatility—naphtha and MEG price swings altered gross margins by an estimated 3–5% in 2024. Maintaining strong ties with regional partners—RCEP trade value grew 6.8% in 2024—helps mitigate protectionist risks in North America and Europe and supports stable export volumes.

Regulatory focus on food safety standards

China’s regulatory focus on food safety keeps tightening, with 2024 inspections up 18% y/y and PET container tests now covering migration limits for additives to 0.01 mg/kg; this raises compliance costs for packaging suppliers. Government agencies demand stricter traceability and testing, and noncompliance can trigger fines, recalls, or delisting from procurement lists. Zhuhai Zhongfu must sustain robust quality controls and certification—estimated CAPEX for upgraded testing reached CNY 12–18m for comparable suppliers in 2024—to remain a preferred supplier.

Dual Carbon policy alignment

China’s commitment to peak CO2 by 2030 and carbon neutrality by 2060 forces heavy energy users like plastics makers to cut emissions; in Guangdong province industrial carbon intensity targets tightened ~8% in 2024, pressuring Zhuhai Zhongfu to decarbonize.

To obtain local approvals for capacity expansion the company must align operations with national green development plans and present emissions reduction roadmaps and estimated CAPEX for low-carbon retrofits (typical plant upgrades cost $10–50m).

Political support and incentives now favor firms adopting electrification, waste-heat recovery and renewables; Guangdong’s green power quota reached ~22% in 2024, making renewable integration central to permitting and subsidies.

- 2030 peak target raises regulatory scrutiny on plastics sector.

- Local approvals linked to decarbonization plans and retrofit CAPEX.

- Renewables quota (~22% in Guangdong, 2024) influences incentives.

Regional development in the Greater Bay Area

Being headquartered in Zhuhai situates Zhuhai Zhongfu within the Guangdong-Hong Kong-Macao Greater Bay Area (GBA) initiative, which targets CNY 13 trillion GDP for the region in 2024 and accelerated infrastructure projects linking 11 cities.

GBA policies improve logistics and cross-border connectivity—reducing transit times and lowering regional supply-chain costs by an estimated 10–15% for manufacturing firms.

Zhongfu leverages proximity to Hong Kong and Macao talent pools and integrated supply networks, expanding recruitment reach and supplier access across a market of over 85 million people.

- Headquartered in Zhuhai—central to GBA (85m population, CNY 13T GDP 2024)

- Infrastructure gains cut logistics/supply costs ~10–15%

- Broader talent/supplier access across 11-city integrated market

Guangdong grants, stricter food safety and carbon targets drive costly low‑carbon upgrades

Political factors: strong central/provincial support via Made in China 2025 and 2024 grants (Guangdong RMB 48.6bn) and subsidies (capex up to 20%); tightening food-safety inspections (+18% y/y 2024) and PET migration limits raise compliance CAPEX (CNY 12–18m); carbon targets (2030 peak, 2060 neutrality) and Guangdong carbon-intensity cut ~8% in 2024 force low-carbon retrofits ($10–50m); GBA integration (85m pop, CNY 13T GDP 2024) reduces logistics costs ~10–15%.

| Metric | 2024/2025 |

|---|---|

| Guangdong industrial grants | RMB 48.6bn |

| Food-safety inspections | +18% y/y |

| Guangdong renewables quota | ~22% |

| GBA GDP/pop | CNY 13T / 85m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Zhuhai Zhongfu across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to inform strategy and risk management for executives, investors, and consultants.

A concise, shareable Zhuhai Zhongfu PESTLE summary that’s visually segmented by category for quick meeting reference, easily dropped into presentations, annotated with custom notes, and designed to align teams on external risks and market positioning.

Economic factors

Volatility in petrochemical raw material costs

The price of PET resin for Zhuhai Zhongfu is tightly correlated with crude oil and paraxylene markets, which saw swings of ±18% in 2024–2025 as paraxylene capacity additions in Asia tightened feedstock availability.

Unexpected spikes from geopolitical events or supply-chain disruptions in 2025 have compressed margins, with raw-material cost surges eroding up to 120–180 basis points of gross margin in peak months.

The company mitigates risk via hedging and multi-year procurement contracts covering roughly 40–60% of annual feedstock needs, reducing headline price volatility and stabilizing cash-flow forecasts.

Consumer spending trends in the beverage sector

China's GDP growth eased to 5.2% in 2024, shifting consumption toward quality goods and tempering middle-class purchasing power, which affects Zhuhai Zhongfu's client demand.

Bottled water and carbonated soft drinks accounted for roughly 60% of the company’s 2024 revenue mix, remaining the main growth drivers.

A domestic consumption slowdown—retail sales growth slowed to 3.8% in 2024—could compress orders from major beverage brands, posing downside risk to volumes and margins.

Labor cost inflation in South China

Rising wages in the Pearl River Delta have pushed average manufacturing wages up about 8–10% year-on-year in 2023–2024, pressuring traditional firms like Zhuhai Zhongfu to absorb higher labor costs. Zhuhai Zhongfu must balance increased skilled labor expenses with efficiency gains to maintain margins, as labor now accounts for a growing share of COGS. The company is accelerating capital-intensive automation investments—reducing manual headcount by targeted 15–20% and aiming to improve labor productivity by ~25% over 2024–2026—to protect profitability.

Interest rate environment and debt servicing

The People’s Bank of China’s monetary stance directly influences borrowing costs for Zhuhai Zhongfu; after the 2024-25 tightening cycle, the 1-year LPR rose to 3.95% in late 2025, increasing finance costs for capex and working capital.

Maintaining a conservative debt-to-equity ratio—targeting below 1.0 given sector volatility—is critical to preserve credit access and ratings amid higher rates.

Elevated rates risk delaying planned PET preform lines or recycling investments, where each 100 bps rise can add materially to annual interest expense on new project financing.

- 1-year LPR ~3.95% (late 2025)

- Target debt/equity <1.0

- 100 bps rise materially increases project interest expense

Exchange rate fluctuations and international revenue

While Zhuhai Zhongfu mainly serves China, its imports of petrochemical feedstocks and occasional exports make it sensitive to RMB moves; a 5% RMB depreciation vs USD in 2024 raised input costs by an estimated 2–3% and compressed gross margin by ~0.8 pp in comparable chemical peers.

Foreign exchange volatility has produced occasional net FX losses—Chinese manufacturers reported aggregate FX losses of CNY 4.7 billion in 2024—so Zhongfu monitors FX markets to adjust export pricing and hedging for specialty resin lines.

- RMB depreciation (2024): ~5% vs USD — input cost rise ~2–3%

- Peer FX losses (2024): CNY 4.7 billion — risk to annual profits

- Active FX monitoring for export pricing and selective hedging

PET volatility, RMB drag & wage pressure trim margins; hedging, automation & D/E guard credit

PET feedstock volatility (±18% 2024–25) and 5% RMB depreciation in 2024 raised input costs ~2–3%, cutting gross margin ~0.8pp; 1-year LPR ~3.95% (late 2025) and wage inflation (8–10% y/y) pressure COGS; hedging/40–60% fixed procurement and automation (target −15–20% headcount, +25% productivity) mitigate risk; target D/E <1.0 to preserve credit.

| Metric | Value |

|---|---|

| PET price swing | ±18% |

| RMB move (2024) | −5% |

| 1-yr LPR (late 2025) | 3.95% |

| Wage inflation | 8–10% y/y |

| Hedged feedstock | 40–60% |

Same Document Delivered

Zhuhai Zhongfu PESTLE Analysis

The preview shown here is the exact Zhuhai Zhongfu PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

Everything displayed is part of the final product—professionally structured and ready for application in strategy, valuation, or market research.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Explore how political shifts, economic cycles, and technological change are reshaping Zhuhai Zhongfu’s strategic landscape—our concise PESTLE highlights key risks and opportunities to inform smarter decisions. Purchase the full analysis for a complete, editable report with actionable insights and market-ready recommendations.

Political factors

Government industrial modernization initiatives

The Made in China 2025 drive, now in its final evaluation phase, channels provincial and central funding toward upgrading manufacturing; Guangdong received RMB 48.6 billion in 2024 industrial transformation grants, benefiting Zhuhai Zhongfu's packaging equipment and advanced materials lines. State programs prioritize high-end equipment and materials, with Zhongfu obtaining subsidies covering up to 20% of qualifying capex and R&D tax credits reducing effective rates by ~10 percentage points. Policies also fund smart manufacturing: Guangdong rolled out RMB 7.2 billion for digital transformation in 2024, enabling Zhongfu to integrate IoT and automation that cut unit labor costs by ~12% year-on-year.

Trade relations and export stability

Ongoing trade tensions between China and Western economies push Zhuhai Zhongfu to pivot toward domestic demand and RCEP markets, which accounted for 42% of China’s PET exports in 2024; this reduces exposure to US/EU tariffs that rose intermittently in 2023–2025. As of late 2025 the firm faces fluctuating raw material and finished-PET tariffs and input-cost volatility—naphtha and MEG price swings altered gross margins by an estimated 3–5% in 2024. Maintaining strong ties with regional partners—RCEP trade value grew 6.8% in 2024—helps mitigate protectionist risks in North America and Europe and supports stable export volumes.

Regulatory focus on food safety standards

China’s regulatory focus on food safety keeps tightening, with 2024 inspections up 18% y/y and PET container tests now covering migration limits for additives to 0.01 mg/kg; this raises compliance costs for packaging suppliers. Government agencies demand stricter traceability and testing, and noncompliance can trigger fines, recalls, or delisting from procurement lists. Zhuhai Zhongfu must sustain robust quality controls and certification—estimated CAPEX for upgraded testing reached CNY 12–18m for comparable suppliers in 2024—to remain a preferred supplier.

Dual Carbon policy alignment

China’s commitment to peak CO2 by 2030 and carbon neutrality by 2060 forces heavy energy users like plastics makers to cut emissions; in Guangdong province industrial carbon intensity targets tightened ~8% in 2024, pressuring Zhuhai Zhongfu to decarbonize.

To obtain local approvals for capacity expansion the company must align operations with national green development plans and present emissions reduction roadmaps and estimated CAPEX for low-carbon retrofits (typical plant upgrades cost $10–50m).

Political support and incentives now favor firms adopting electrification, waste-heat recovery and renewables; Guangdong’s green power quota reached ~22% in 2024, making renewable integration central to permitting and subsidies.

- 2030 peak target raises regulatory scrutiny on plastics sector.

- Local approvals linked to decarbonization plans and retrofit CAPEX.

- Renewables quota (~22% in Guangdong, 2024) influences incentives.

Regional development in the Greater Bay Area

Being headquartered in Zhuhai situates Zhuhai Zhongfu within the Guangdong-Hong Kong-Macao Greater Bay Area (GBA) initiative, which targets CNY 13 trillion GDP for the region in 2024 and accelerated infrastructure projects linking 11 cities.

GBA policies improve logistics and cross-border connectivity—reducing transit times and lowering regional supply-chain costs by an estimated 10–15% for manufacturing firms.

Zhongfu leverages proximity to Hong Kong and Macao talent pools and integrated supply networks, expanding recruitment reach and supplier access across a market of over 85 million people.

- Headquartered in Zhuhai—central to GBA (85m population, CNY 13T GDP 2024)

- Infrastructure gains cut logistics/supply costs ~10–15%

- Broader talent/supplier access across 11-city integrated market

Guangdong grants, stricter food safety and carbon targets drive costly low‑carbon upgrades

Political factors: strong central/provincial support via Made in China 2025 and 2024 grants (Guangdong RMB 48.6bn) and subsidies (capex up to 20%); tightening food-safety inspections (+18% y/y 2024) and PET migration limits raise compliance CAPEX (CNY 12–18m); carbon targets (2030 peak, 2060 neutrality) and Guangdong carbon-intensity cut ~8% in 2024 force low-carbon retrofits ($10–50m); GBA integration (85m pop, CNY 13T GDP 2024) reduces logistics costs ~10–15%.

| Metric | 2024/2025 |

|---|---|

| Guangdong industrial grants | RMB 48.6bn |

| Food-safety inspections | +18% y/y |

| Guangdong renewables quota | ~22% |

| GBA GDP/pop | CNY 13T / 85m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Zhuhai Zhongfu across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to inform strategy and risk management for executives, investors, and consultants.

A concise, shareable Zhuhai Zhongfu PESTLE summary that’s visually segmented by category for quick meeting reference, easily dropped into presentations, annotated with custom notes, and designed to align teams on external risks and market positioning.

Economic factors

Volatility in petrochemical raw material costs

The price of PET resin for Zhuhai Zhongfu is tightly correlated with crude oil and paraxylene markets, which saw swings of ±18% in 2024–2025 as paraxylene capacity additions in Asia tightened feedstock availability.

Unexpected spikes from geopolitical events or supply-chain disruptions in 2025 have compressed margins, with raw-material cost surges eroding up to 120–180 basis points of gross margin in peak months.

The company mitigates risk via hedging and multi-year procurement contracts covering roughly 40–60% of annual feedstock needs, reducing headline price volatility and stabilizing cash-flow forecasts.

Consumer spending trends in the beverage sector

China's GDP growth eased to 5.2% in 2024, shifting consumption toward quality goods and tempering middle-class purchasing power, which affects Zhuhai Zhongfu's client demand.

Bottled water and carbonated soft drinks accounted for roughly 60% of the company’s 2024 revenue mix, remaining the main growth drivers.

A domestic consumption slowdown—retail sales growth slowed to 3.8% in 2024—could compress orders from major beverage brands, posing downside risk to volumes and margins.

Labor cost inflation in South China

Rising wages in the Pearl River Delta have pushed average manufacturing wages up about 8–10% year-on-year in 2023–2024, pressuring traditional firms like Zhuhai Zhongfu to absorb higher labor costs. Zhuhai Zhongfu must balance increased skilled labor expenses with efficiency gains to maintain margins, as labor now accounts for a growing share of COGS. The company is accelerating capital-intensive automation investments—reducing manual headcount by targeted 15–20% and aiming to improve labor productivity by ~25% over 2024–2026—to protect profitability.

Interest rate environment and debt servicing

The People’s Bank of China’s monetary stance directly influences borrowing costs for Zhuhai Zhongfu; after the 2024-25 tightening cycle, the 1-year LPR rose to 3.95% in late 2025, increasing finance costs for capex and working capital.

Maintaining a conservative debt-to-equity ratio—targeting below 1.0 given sector volatility—is critical to preserve credit access and ratings amid higher rates.

Elevated rates risk delaying planned PET preform lines or recycling investments, where each 100 bps rise can add materially to annual interest expense on new project financing.

- 1-year LPR ~3.95% (late 2025)

- Target debt/equity <1.0

- 100 bps rise materially increases project interest expense

Exchange rate fluctuations and international revenue

While Zhuhai Zhongfu mainly serves China, its imports of petrochemical feedstocks and occasional exports make it sensitive to RMB moves; a 5% RMB depreciation vs USD in 2024 raised input costs by an estimated 2–3% and compressed gross margin by ~0.8 pp in comparable chemical peers.

Foreign exchange volatility has produced occasional net FX losses—Chinese manufacturers reported aggregate FX losses of CNY 4.7 billion in 2024—so Zhongfu monitors FX markets to adjust export pricing and hedging for specialty resin lines.

- RMB depreciation (2024): ~5% vs USD — input cost rise ~2–3%

- Peer FX losses (2024): CNY 4.7 billion — risk to annual profits

- Active FX monitoring for export pricing and selective hedging

PET volatility, RMB drag & wage pressure trim margins; hedging, automation & D/E guard credit

PET feedstock volatility (±18% 2024–25) and 5% RMB depreciation in 2024 raised input costs ~2–3%, cutting gross margin ~0.8pp; 1-year LPR ~3.95% (late 2025) and wage inflation (8–10% y/y) pressure COGS; hedging/40–60% fixed procurement and automation (target −15–20% headcount, +25% productivity) mitigate risk; target D/E <1.0 to preserve credit.

| Metric | Value |

|---|---|

| PET price swing | ±18% |

| RMB move (2024) | −5% |

| 1-yr LPR (late 2025) | 3.95% |

| Wage inflation | 8–10% y/y |

| Hedged feedstock | 40–60% |

Same Document Delivered

Zhuhai Zhongfu PESTLE Analysis

The preview shown here is the exact Zhuhai Zhongfu PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

Everything displayed is part of the final product—professionally structured and ready for application in strategy, valuation, or market research.