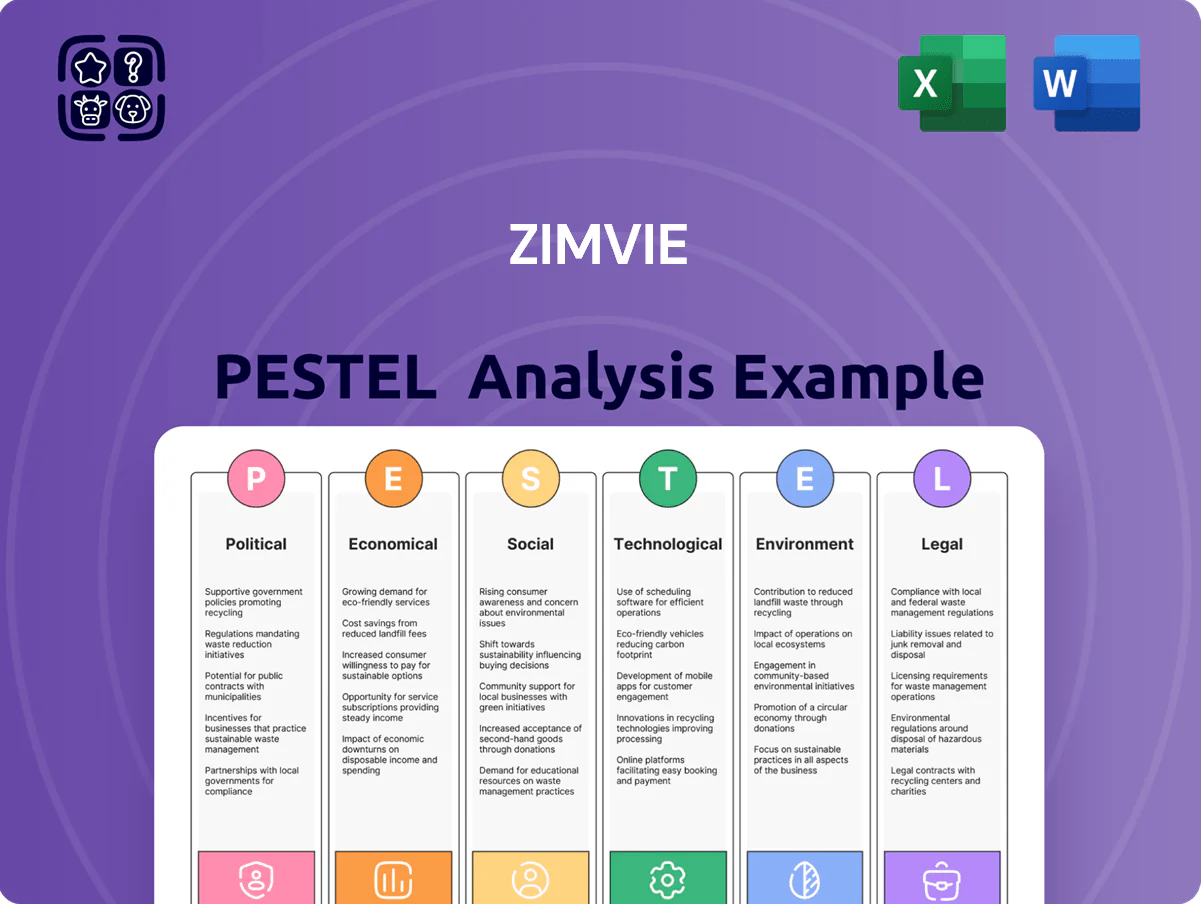

ZimVie PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, healthcare spending trends, and rapid medtech innovation are shaping ZimVie's trajectory—our concise PESTLE snapshot highlights key risks and opportunities you need to know; purchase the full, editable PESTLE Analysis to get detailed insights, actionable recommendations, and data-ready charts for immediate strategic use.

Political factors

Global Trade Policy and Tariffs

Changes in international trade agreements and tariffs drive input and finished-goods costs for ZimVie; e.g., US tariffs on Chinese medical devices rose effective 2024, lifting some component import costs by 5–12%, while EU trade barriers pushed average landed costs up ~6% in 2023–24.

With a global supply chain, deterioration in US-China ties or new European non-tariff barriers can disrupt manufacturing lead times, contributing to reported FY2024 COGS growth of ~7% year-over-year for comparable device makers.

Strategic planning must model tariff scenarios and diversify sourcing—shifting even 15–20% of procurement to alternate regions can stabilize margins and help retain competitive pricing across key markets.

Healthcare Reimbursement Reform

Regulatory Harmonization Initiatives

The shift to EU MDR (fully applicable since May 2021) and global regulatory harmonization raises compliance costs for ZimVie, with industry estimates showing MDR-related conformity costs up to 5-10% of product revenues; aligning submissions across FDA and notified bodies remains a priority to avoid delays in the 20+ markets where ZimVie seeks authorization.

Geopolitical Stability in Manufacturing Hubs

Political unrest in manufacturing hubs where ZimVie or key suppliers operate can cause supply chain delays; for example, global supply disruptions in 2024 raised lead times by up to 28% in some medical device supply chains.

Monitoring emerging-market political climates is essential to mitigate expropriation, civil unrest, or abrupt labor-law changes that could affect ~15–20% of components sourced from Asia and Latin America.

Establishing redundant supply chains in stable regions—shifting 10–25% of sourcing to North America or EU facilities—reduces disruption risk and supports continuity.

- Up to 28% longer lead times reported in 2024 supply disruptions

- 15–20% of components sourced from higher-risk emerging markets

- 10–25% of sourcing can be shifted to stable regions to reduce risk

Public Health Funding and Advocacy

Governmental funding for oral health campaigns—e.g., WHO noting 3.5 billion people affected by oral diseases in 2022—increases demand for advanced restorative solutions, benefiting ZimVie’s implant and restorative product lines.

Dental association lobbying raises oral health on national agendas; countries increasing oral health budgets (US dental spending ~135 billion USD in 2023) boost procedure volumes and device uptake.

Political recognition of oral-systemic links drives higher utilization rates of ZimVie products through public programs and reimbursement policies.

- Increased public funding → higher procedure demand

- Advocacy elevates policy priority and reimbursement

- Oral-systemic recognition raises device utilization

Political risks, tariffs and MDR squeeze ZimVie margins—reshore 10–25% to cut disruption

Political shifts—tariffs (US-China 2024 +5–12%), EU pricing caps, Medicare/Medicaid dental proposals (CMS 2024) and MDR compliance (costs ~5–10% revenue)—drive ZimVie margin and access risks; supply-chain political unrest raised lead times up to 28% in 2024; reallocating 10–25% sourcing to stable regions can cut disruption exposure.

| Factor | 2023–24 Data |

|---|---|

| Tariff impact | +5–12% |

| MDR compliance | 5–10% rev. |

| Lead-time rise | Up to 28% |

| Sourcing shift | 10–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect ZimVie across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Condenses ZimVie’s full PESTLE into a shareable, slide-ready summary that highlights key external risks and market drivers for quick alignment across teams.

Economic factors

Consumer Discretionary Spending Levels

High-end dental procedures like implants and complex restorations are largely paid out-of-pocket and therefore closely tied to disposable income; U.S. consumer spending fell 0.2% in Q4 2025 vs Q3 2025 amid 3.4% inflation, pressuring elective demand. Economic downturns prompt patients to defer elective surgeries in favor of essential care—global elective procedure volumes dropped ~6% in 2024 vs 2019. ZimVie's revenue growth remains correlated with global GDP and middle-class financial confidence, with middle-income households accounting for roughly 60% of elective dental spend.

Interest Rate Environment and Financing

Prevailing interest rates affect ZimVie’s customers—dental practices and DSOs—by raising borrowing costs for expensive equipment and inventory; US prime rate rose to 8.50% in 2024, tightening financing for capex-heavy purchases.

Higher rates can slow clinic expansion, reducing demand for ZimVie’s digital dentistry tools and implants; US dental capex growth decelerated to ~2% in 2024 vs 6% in 2022.

Investors track central bank policy—Fed pauses or cuts could revive provider capex cycles, while further hikes would suppress investment in new tech and consolidation.

Foreign Exchange Rate Volatility

As a multinational MedTech firm, ZimVie faces currency translation risk that trimmed adjusted EBITDA by an estimated 2–3% in FY2024 as the US dollar strengthened ~8% vs the euro, pressuring reported earnings and margins.

A stronger dollar makes ZimVie products pricier abroad, risking share losses to local competitors in Europe and emerging markets where price elasticity is high.

ZimVie uses forward contracts and option hedges—hedged exposures covered roughly 60% of near-term FX risk in 2024—and is expanding localized manufacturing to lower currency pass-through and protect margins.

Inflationary Pressures on Raw Materials

Rising costs for medical-grade titanium (+18% YoY in 2024) and specialty polymers, plus a 22% surge in industrial energy prices in key markets, are increasing ZimVie’s COGS for dental implants and restorative products.

ZimVie must weigh passing costs via price hikes against volume loss to lower-cost competitors; sensitivity models show a 3–5% price rise could cut volumes 4–7%.

Active monitoring of global commodity indices (titanium, polymer resin, energy) is required to protect gross margins near the 60% target reported in FY2024.

- Ti prices +18% (2024)

- Energy +22% (2024)

- Price hike elasticity: −4 to −7% volume per 3–5% increase

- Target gross margin ~60% (FY2024)

Consolidation of Dental Service Organizations

Consolidation of dental practices into DSOs shifts purchasing power toward large buyers; as of 2024 DSOs account for roughly 30–40% of US dental care revenue, enabling them to secure double-digit discounts on implants and biomaterials and pressuring ZimVie's margin and pricing strategy.

Transitioning to a B2B model focused on institutional contracts is vital—ZimVie must offer volume pricing, supply-chain integration, and service-level agreements to retain share as DSOs expand.

- 2024 DSOs ~30–40% of US dental revenue

- DSO-negotiated discounts often 10–20% on implants

- ZimVie needs B2B pricing, logistics, contract support

Elective dental hit by weaker consumer spend, rising rates and input-cost squeeze

Economic sensitivity: elective dental demand tied to disposable income—US consumer spending fell 0.2% Q4 2025; global elective volumes −6% (2024 vs 2019). Higher rates (US prime 8.50% in 2024) and rising input costs (titanium +18%, energy +22% in 2024) pressure capex, margins (gross ~60% FY2024) and pricing vs DSOs (30–40% US revenue).

| Metric | Value |

|---|---|

| Elective volumes | −6% (2024 vs 2019) |

| US prime | 8.50% (2024) |

| Titanium | +18% (2024) |

| Energy | +22% (2024) |

| Gross margin | ~60% (FY2024) |

| DSO share | 30–40% (2024) |

Full Version Awaits

ZimVie PESTLE Analysis

The preview shown here is the exact ZimVie PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, healthcare spending trends, and rapid medtech innovation are shaping ZimVie's trajectory—our concise PESTLE snapshot highlights key risks and opportunities you need to know; purchase the full, editable PESTLE Analysis to get detailed insights, actionable recommendations, and data-ready charts for immediate strategic use.

Political factors

Global Trade Policy and Tariffs

Changes in international trade agreements and tariffs drive input and finished-goods costs for ZimVie; e.g., US tariffs on Chinese medical devices rose effective 2024, lifting some component import costs by 5–12%, while EU trade barriers pushed average landed costs up ~6% in 2023–24.

With a global supply chain, deterioration in US-China ties or new European non-tariff barriers can disrupt manufacturing lead times, contributing to reported FY2024 COGS growth of ~7% year-over-year for comparable device makers.

Strategic planning must model tariff scenarios and diversify sourcing—shifting even 15–20% of procurement to alternate regions can stabilize margins and help retain competitive pricing across key markets.

Healthcare Reimbursement Reform

Regulatory Harmonization Initiatives

The shift to EU MDR (fully applicable since May 2021) and global regulatory harmonization raises compliance costs for ZimVie, with industry estimates showing MDR-related conformity costs up to 5-10% of product revenues; aligning submissions across FDA and notified bodies remains a priority to avoid delays in the 20+ markets where ZimVie seeks authorization.

Geopolitical Stability in Manufacturing Hubs

Political unrest in manufacturing hubs where ZimVie or key suppliers operate can cause supply chain delays; for example, global supply disruptions in 2024 raised lead times by up to 28% in some medical device supply chains.

Monitoring emerging-market political climates is essential to mitigate expropriation, civil unrest, or abrupt labor-law changes that could affect ~15–20% of components sourced from Asia and Latin America.

Establishing redundant supply chains in stable regions—shifting 10–25% of sourcing to North America or EU facilities—reduces disruption risk and supports continuity.

- Up to 28% longer lead times reported in 2024 supply disruptions

- 15–20% of components sourced from higher-risk emerging markets

- 10–25% of sourcing can be shifted to stable regions to reduce risk

Public Health Funding and Advocacy

Governmental funding for oral health campaigns—e.g., WHO noting 3.5 billion people affected by oral diseases in 2022—increases demand for advanced restorative solutions, benefiting ZimVie’s implant and restorative product lines.

Dental association lobbying raises oral health on national agendas; countries increasing oral health budgets (US dental spending ~135 billion USD in 2023) boost procedure volumes and device uptake.

Political recognition of oral-systemic links drives higher utilization rates of ZimVie products through public programs and reimbursement policies.

- Increased public funding → higher procedure demand

- Advocacy elevates policy priority and reimbursement

- Oral-systemic recognition raises device utilization

Political risks, tariffs and MDR squeeze ZimVie margins—reshore 10–25% to cut disruption

Political shifts—tariffs (US-China 2024 +5–12%), EU pricing caps, Medicare/Medicaid dental proposals (CMS 2024) and MDR compliance (costs ~5–10% revenue)—drive ZimVie margin and access risks; supply-chain political unrest raised lead times up to 28% in 2024; reallocating 10–25% sourcing to stable regions can cut disruption exposure.

| Factor | 2023–24 Data |

|---|---|

| Tariff impact | +5–12% |

| MDR compliance | 5–10% rev. |

| Lead-time rise | Up to 28% |

| Sourcing shift | 10–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect ZimVie across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Condenses ZimVie’s full PESTLE into a shareable, slide-ready summary that highlights key external risks and market drivers for quick alignment across teams.

Economic factors

Consumer Discretionary Spending Levels

High-end dental procedures like implants and complex restorations are largely paid out-of-pocket and therefore closely tied to disposable income; U.S. consumer spending fell 0.2% in Q4 2025 vs Q3 2025 amid 3.4% inflation, pressuring elective demand. Economic downturns prompt patients to defer elective surgeries in favor of essential care—global elective procedure volumes dropped ~6% in 2024 vs 2019. ZimVie's revenue growth remains correlated with global GDP and middle-class financial confidence, with middle-income households accounting for roughly 60% of elective dental spend.

Interest Rate Environment and Financing

Prevailing interest rates affect ZimVie’s customers—dental practices and DSOs—by raising borrowing costs for expensive equipment and inventory; US prime rate rose to 8.50% in 2024, tightening financing for capex-heavy purchases.

Higher rates can slow clinic expansion, reducing demand for ZimVie’s digital dentistry tools and implants; US dental capex growth decelerated to ~2% in 2024 vs 6% in 2022.

Investors track central bank policy—Fed pauses or cuts could revive provider capex cycles, while further hikes would suppress investment in new tech and consolidation.

Foreign Exchange Rate Volatility

As a multinational MedTech firm, ZimVie faces currency translation risk that trimmed adjusted EBITDA by an estimated 2–3% in FY2024 as the US dollar strengthened ~8% vs the euro, pressuring reported earnings and margins.

A stronger dollar makes ZimVie products pricier abroad, risking share losses to local competitors in Europe and emerging markets where price elasticity is high.

ZimVie uses forward contracts and option hedges—hedged exposures covered roughly 60% of near-term FX risk in 2024—and is expanding localized manufacturing to lower currency pass-through and protect margins.

Inflationary Pressures on Raw Materials

Rising costs for medical-grade titanium (+18% YoY in 2024) and specialty polymers, plus a 22% surge in industrial energy prices in key markets, are increasing ZimVie’s COGS for dental implants and restorative products.

ZimVie must weigh passing costs via price hikes against volume loss to lower-cost competitors; sensitivity models show a 3–5% price rise could cut volumes 4–7%.

Active monitoring of global commodity indices (titanium, polymer resin, energy) is required to protect gross margins near the 60% target reported in FY2024.

- Ti prices +18% (2024)

- Energy +22% (2024)

- Price hike elasticity: −4 to −7% volume per 3–5% increase

- Target gross margin ~60% (FY2024)

Consolidation of Dental Service Organizations

Consolidation of dental practices into DSOs shifts purchasing power toward large buyers; as of 2024 DSOs account for roughly 30–40% of US dental care revenue, enabling them to secure double-digit discounts on implants and biomaterials and pressuring ZimVie's margin and pricing strategy.

Transitioning to a B2B model focused on institutional contracts is vital—ZimVie must offer volume pricing, supply-chain integration, and service-level agreements to retain share as DSOs expand.

- 2024 DSOs ~30–40% of US dental revenue

- DSO-negotiated discounts often 10–20% on implants

- ZimVie needs B2B pricing, logistics, contract support

Elective dental hit by weaker consumer spend, rising rates and input-cost squeeze

Economic sensitivity: elective dental demand tied to disposable income—US consumer spending fell 0.2% Q4 2025; global elective volumes −6% (2024 vs 2019). Higher rates (US prime 8.50% in 2024) and rising input costs (titanium +18%, energy +22% in 2024) pressure capex, margins (gross ~60% FY2024) and pricing vs DSOs (30–40% US revenue).

| Metric | Value |

|---|---|

| Elective volumes | −6% (2024 vs 2019) |

| US prime | 8.50% (2024) |

| Titanium | +18% (2024) |

| Energy | +22% (2024) |

| Gross margin | ~60% (FY2024) |

| DSO share | 30–40% (2024) |

Full Version Awaits

ZimVie PESTLE Analysis

The preview shown here is the exact ZimVie PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.