Zip Marketing Mix

Get Inspired by a Complete Brand Strategy

Discover how Zip’s product features, pricing tiers, distribution channels, and promotional tactics combine to drive market traction—this concise overview highlights key strengths and opportunities; for an editable, presentation-ready deep dive with real data, strategic recommendations, and ready-to-use templates, get the full 4P’s Marketing Mix Analysis to save time and accelerate decision-making.

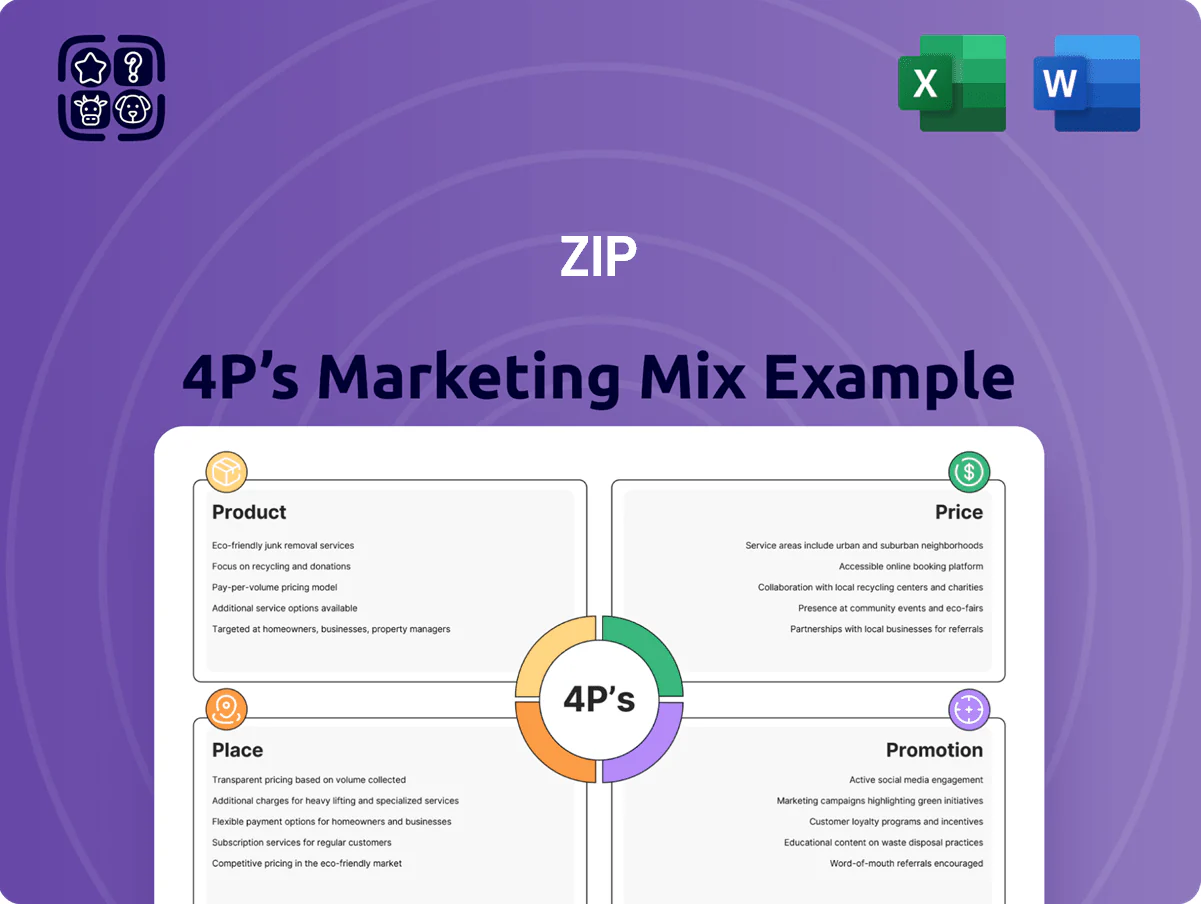

Product

Zip Business Capital

Zip Business Capital offers unsecured SME loans from 5,000 to 500,000 USD, targeting fast access to growth capital and cash‑flow gaps; average approval time reported in 2024 was 48 hours versus 15+ days at banks.

Products emphasize flexible terms tied to borrower cash cycles—typical tenors 3–24 months—and Zip’s 2024 SME portfolio saw a 4.2% default rate, funding ~USD 420M globally.

Zip Business Trade

Zip Business Trade is an account-based credit line functioning as a digital wallet for procurement and inventory, letting SMEs pay suppliers up front and defer cash outlay—often with a 0% interest window (typical 30–60 days); Zip reported 2025 Q1 merchant acceptance growth of 18% YoY, with business account volumes up 22%.

Merchant Integration API

Zip's Merchant Integration API lets merchants embed buy-now-pay-later at checkout and POS, boosting average order value by about 18% and conversion rates by ~12% based on 2024 Zip merchant data; it supports RESTful endpoints, SDKs, and webhooks for cards, mobile, and POS terminals.

Zip Business Trade Plus

Zip Business Trade Plus targets larger enterprises, offering higher credit limits (commonly $50k–$250k) and advanced spend-management tools for corporate spending.

It adds enhanced reporting and admin controls for real-time employee spend and departmental budgets, cutting reconciliation time by ~40% in Zip case studies (2024 pilot).

Designed to scale with business complexity, it supports multi-entity billing and integrates with ERP systems (SAP, Xero) to streamline cash flow across subsidiaries.

- Higher limits: $50k–$250k typical

- Real-time control: ~40% faster reconciliation (2024)

- ERP integrations: SAP, Xero, NetSuite

Virtual Card Technology

Zip Business issues virtual cards that work across Visa and Mastercard networks, letting firms pay merchants that aren’t Zip partners and turning Zip’s credit line into a universal tool; as of 2025 Zip reported ~1.2M business users, boosting ARPU by 9% year-over-year.

Virtual cards offer single-use numbers for one-off vendor invoices or recurring tokens for subscriptions, reducing fraud risk and lowering reconciliation time; industry data shows virtual cards cut card-not-present fraud by ~40%.

- Universal acceptance via Visa/Mastercard

- Single-use or recurring tokens

- Reduces fraud ~40%

- Supports 1.2M business users (2025)

- ARPU +9% YoY

Zip Business: Fast $5k–$500k SME loans, $420M portfolio, 1.2M users, 4.2% defaults

Zip Business offers unsecured SME loans $5k–$500k (avg approval 48h, 2024), Trade credit lines with 0% windows (30–60d) and Trade Plus ($50k–$250k) with ERP integrations; virtual Visa/Mastercard cards serve ~1.2M users (2025), ARPU +9% YoY, portfolio funded ~$420M, default 4.2% (2024).

| Metric | Value |

|---|---|

| Approval time | 48h (2024) |

| Loan range | $5k–$500k |

| Portfolio | $420M (2024) |

| Default rate | 4.2% (2024) |

| Business users | 1.2M (2025) |

| ARPU growth | +9% YoY |

What is included in the product

Delivers a company-specific deep dive into Zip’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to ground recommendations.

Summarizes Zip’s 4P marketing strategy into a concise, presentation-ready snapshot that quickly relieves briefing and alignment pain points for leadership and cross-functional teams.

Place

Direct Online Platform

Zip Business’s primary access is its proprietary web portal and mobile app, letting users open accounts and apply for funding online; as of Q4 2025 the platform saw 1.2 million active business users and processed 78% of loan applications digitally. This digital-first model removes geographic barriers for remote and digital firms, increasing rural SME reach by 34% year-over-year. The portal centralizes admin tasks—repayment schedules, credit-limit increase requests, and statements—cutting service time by 42%.

E-commerce Partner Network

Zip embeds at checkout across thousands of retailers, appearing at the purchase decision point to lift conversion; internal data shows POS placement can boost AOV (average order value) by ~10% and conversion by 6–12% in BNPL pilots (2024 pilots with Shopify merchants).

Physical Retail Point-of-Sale

Physical retail point-of-sale uses QR codes and NFC-enabled digital cards so contractors and retailers can access Zip Business on-site without corporate cards or cash; in 2025 Zip reported 28% of SMB transactions started via QR/NFC at partner stores.

That bridge from digital credit to physical commerce cuts procurement friction—average ticket sizes rose 14% for trade purchases after rollout, per Zip’s 2024 merchant data.

Partner merchants receive branded signage and marketing collateral; stores displaying Zip materials saw a 22% uplift in payment adoption within six months.

Global Market Presence

As of late 2025, Zip focuses on Australia and the United States, aligning offers to local rules and capturing markets with rapid BNPL adoption—Australia accounted for ~48% of FY2025 GMV and US growth hit 42% YoY.

Targeting high-growth, digitally mature regions lets Zip concentrate distribution where alternative lending demand is highest, keeping operating margins near 8% in FY2025 while serving 10+ markets.

- Core markets: Australia, US

- FY2025: Australia ~48% GMV

- US growth: 42% YoY in 2025

- Operating margin: ~8% FY2025

Integration with Accounting Software

Zip Business integrates with Xero and QuickBooks, letting SMEs manage Zip invoices and payments inside their accounting apps; 2024 Xero reported 4.4 million subscribers and Intuit QuickBooks had ~6 million global small-business customers, so placement hits large user bases.

This reduces admin time—clients report 25–30% faster reconciliation in similar integrations—and embeds Zip into daily cashflow workflows, raising stickiness and transaction frequency.

- Integrates with Xero, QuickBooks

- Reaches ~10.4M SMB users (2024)

- 25–30% faster reconciliation

- Increases daily product stickiness

Zip Business: 1.2M users, digital-first SME growth—QR/NFC 28%, US +42% YoY

Zip Business uses a digital-first portal and app plus embedded POS, QR/NFC onsite access, and accounting integrations (Xero, QuickBooks) to broaden SME reach—1.2M active users (Q4 2025), 78% digital app rate, 34% rural SME growth, 28% QR/NFC transactions (2025), Australia ~48% FY2025 GMV, US growth 42% YoY; integrations cut reconciliation time 25–30% and lift stickiness.

| Metric | Value |

|---|---|

| Active users (Q4 2025) | 1.2M |

| Digital application share | 78% |

| Rural SME reach YoY | +34% |

| QR/NFC start share (2025) | 28% |

| Australia GMV (FY2025) | ~48% |

| US growth (2025 YoY) | 42% |

| Operating margin (FY2025) | ~8% |

| Reconciliation time saved | 25–30% |

Preview the Actual Deliverable

Zip 4P's Marketing Mix Analysis

The preview shown here is the actual Zip 4P's Marketing Mix document you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Get Inspired by a Complete Brand Strategy

Discover how Zip’s product features, pricing tiers, distribution channels, and promotional tactics combine to drive market traction—this concise overview highlights key strengths and opportunities; for an editable, presentation-ready deep dive with real data, strategic recommendations, and ready-to-use templates, get the full 4P’s Marketing Mix Analysis to save time and accelerate decision-making.

Product

Zip Business Capital

Zip Business Capital offers unsecured SME loans from 5,000 to 500,000 USD, targeting fast access to growth capital and cash‑flow gaps; average approval time reported in 2024 was 48 hours versus 15+ days at banks.

Products emphasize flexible terms tied to borrower cash cycles—typical tenors 3–24 months—and Zip’s 2024 SME portfolio saw a 4.2% default rate, funding ~USD 420M globally.

Zip Business Trade

Zip Business Trade is an account-based credit line functioning as a digital wallet for procurement and inventory, letting SMEs pay suppliers up front and defer cash outlay—often with a 0% interest window (typical 30–60 days); Zip reported 2025 Q1 merchant acceptance growth of 18% YoY, with business account volumes up 22%.

Merchant Integration API

Zip's Merchant Integration API lets merchants embed buy-now-pay-later at checkout and POS, boosting average order value by about 18% and conversion rates by ~12% based on 2024 Zip merchant data; it supports RESTful endpoints, SDKs, and webhooks for cards, mobile, and POS terminals.

Zip Business Trade Plus

Zip Business Trade Plus targets larger enterprises, offering higher credit limits (commonly $50k–$250k) and advanced spend-management tools for corporate spending.

It adds enhanced reporting and admin controls for real-time employee spend and departmental budgets, cutting reconciliation time by ~40% in Zip case studies (2024 pilot).

Designed to scale with business complexity, it supports multi-entity billing and integrates with ERP systems (SAP, Xero) to streamline cash flow across subsidiaries.

- Higher limits: $50k–$250k typical

- Real-time control: ~40% faster reconciliation (2024)

- ERP integrations: SAP, Xero, NetSuite

Virtual Card Technology

Zip Business issues virtual cards that work across Visa and Mastercard networks, letting firms pay merchants that aren’t Zip partners and turning Zip’s credit line into a universal tool; as of 2025 Zip reported ~1.2M business users, boosting ARPU by 9% year-over-year.

Virtual cards offer single-use numbers for one-off vendor invoices or recurring tokens for subscriptions, reducing fraud risk and lowering reconciliation time; industry data shows virtual cards cut card-not-present fraud by ~40%.

- Universal acceptance via Visa/Mastercard

- Single-use or recurring tokens

- Reduces fraud ~40%

- Supports 1.2M business users (2025)

- ARPU +9% YoY

Zip Business: Fast $5k–$500k SME loans, $420M portfolio, 1.2M users, 4.2% defaults

Zip Business offers unsecured SME loans $5k–$500k (avg approval 48h, 2024), Trade credit lines with 0% windows (30–60d) and Trade Plus ($50k–$250k) with ERP integrations; virtual Visa/Mastercard cards serve ~1.2M users (2025), ARPU +9% YoY, portfolio funded ~$420M, default 4.2% (2024).

| Metric | Value |

|---|---|

| Approval time | 48h (2024) |

| Loan range | $5k–$500k |

| Portfolio | $420M (2024) |

| Default rate | 4.2% (2024) |

| Business users | 1.2M (2025) |

| ARPU growth | +9% YoY |

What is included in the product

Delivers a company-specific deep dive into Zip’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to ground recommendations.

Summarizes Zip’s 4P marketing strategy into a concise, presentation-ready snapshot that quickly relieves briefing and alignment pain points for leadership and cross-functional teams.

Place

Direct Online Platform

Zip Business’s primary access is its proprietary web portal and mobile app, letting users open accounts and apply for funding online; as of Q4 2025 the platform saw 1.2 million active business users and processed 78% of loan applications digitally. This digital-first model removes geographic barriers for remote and digital firms, increasing rural SME reach by 34% year-over-year. The portal centralizes admin tasks—repayment schedules, credit-limit increase requests, and statements—cutting service time by 42%.

E-commerce Partner Network

Zip embeds at checkout across thousands of retailers, appearing at the purchase decision point to lift conversion; internal data shows POS placement can boost AOV (average order value) by ~10% and conversion by 6–12% in BNPL pilots (2024 pilots with Shopify merchants).

Physical Retail Point-of-Sale

Physical retail point-of-sale uses QR codes and NFC-enabled digital cards so contractors and retailers can access Zip Business on-site without corporate cards or cash; in 2025 Zip reported 28% of SMB transactions started via QR/NFC at partner stores.

That bridge from digital credit to physical commerce cuts procurement friction—average ticket sizes rose 14% for trade purchases after rollout, per Zip’s 2024 merchant data.

Partner merchants receive branded signage and marketing collateral; stores displaying Zip materials saw a 22% uplift in payment adoption within six months.

Global Market Presence

As of late 2025, Zip focuses on Australia and the United States, aligning offers to local rules and capturing markets with rapid BNPL adoption—Australia accounted for ~48% of FY2025 GMV and US growth hit 42% YoY.

Targeting high-growth, digitally mature regions lets Zip concentrate distribution where alternative lending demand is highest, keeping operating margins near 8% in FY2025 while serving 10+ markets.

- Core markets: Australia, US

- FY2025: Australia ~48% GMV

- US growth: 42% YoY in 2025

- Operating margin: ~8% FY2025

Integration with Accounting Software

Zip Business integrates with Xero and QuickBooks, letting SMEs manage Zip invoices and payments inside their accounting apps; 2024 Xero reported 4.4 million subscribers and Intuit QuickBooks had ~6 million global small-business customers, so placement hits large user bases.

This reduces admin time—clients report 25–30% faster reconciliation in similar integrations—and embeds Zip into daily cashflow workflows, raising stickiness and transaction frequency.

- Integrates with Xero, QuickBooks

- Reaches ~10.4M SMB users (2024)

- 25–30% faster reconciliation

- Increases daily product stickiness

Zip Business: 1.2M users, digital-first SME growth—QR/NFC 28%, US +42% YoY

Zip Business uses a digital-first portal and app plus embedded POS, QR/NFC onsite access, and accounting integrations (Xero, QuickBooks) to broaden SME reach—1.2M active users (Q4 2025), 78% digital app rate, 34% rural SME growth, 28% QR/NFC transactions (2025), Australia ~48% FY2025 GMV, US growth 42% YoY; integrations cut reconciliation time 25–30% and lift stickiness.

| Metric | Value |

|---|---|

| Active users (Q4 2025) | 1.2M |

| Digital application share | 78% |

| Rural SME reach YoY | +34% |

| QR/NFC start share (2025) | 28% |

| Australia GMV (FY2025) | ~48% |

| US growth (2025 YoY) | 42% |

| Operating margin (FY2025) | ~8% |

| Reconciliation time saved | 25–30% |

Preview the Actual Deliverable

Zip 4P's Marketing Mix Analysis

The preview shown here is the actual Zip 4P's Marketing Mix document you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.