ZipRecruiter Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

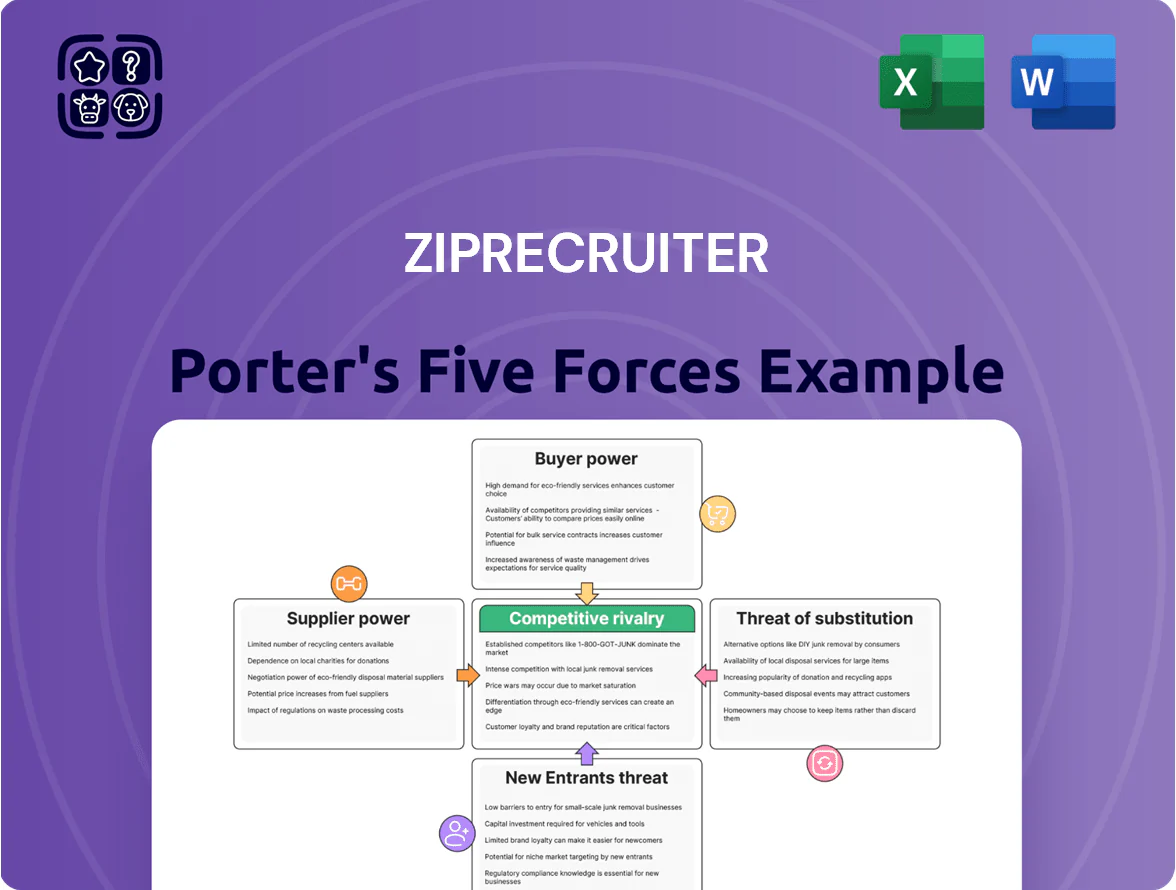

ZipRecruiter faces intense rivalry from entrenched job boards and niche platforms, moderate buyer power as employers seek cost-effective hiring tools, low supplier power, growing threat from AI-driven recruitment substitutes, and barriers that temper new entrants; strategic positioning hinges on network effects and product differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ZipRecruiter’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Providers

ZipRecruiter depends on major cloud providers, chiefly Amazon Web Services (AWS), to run its AI marketplace and analytics; in 2024 AWS and similar providers accounted for over 60% of enterprise cloud spend, concentrating supplier power.

Switching costs are high: migrating petabytes of candidate data and proprietary ML models can take months and cost millions—estimates range $2–10M for mid‑scale moves—so supplier leverage rises.

Price hikes or outages hit margins and reliability directly; AWS price or outage shifts in 2023 cost customers an estimated $1B in lost revenue across affected platforms, making supplier risk material for ZipRecruiter.

Digital Advertising Platforms

ZipRecruiter spends a large share of marketing budget on Google, Meta and other search engines—advertising and paid search were roughly 35–45% of digital ad spend in the jobs category in 2024—making these platforms gatekeepers of applicant and employer traffic.

That gatekeeper role lets platforms set CPC (cost-per-click) and algorithm visibility; ZipRecruiter reported marketing expenses of $233M in 2024, so even modest CPC shifts materially change CAC (customer acquisition cost).

ZipRecruiter must constantly optimize bids, creative and feed quality to compete with Indeed, LinkedIn and niche boards for scarce ad inventory and keep CPA (cost per applicant) from rising above acceptable margins.

Specialized AI Talent

ZipRecruiter’s matching engine depends on data scientists and ML engineers, whose skills drove a 28% salary rise in US AI roles in 2025, raising supplier power.

In late 2025’s tight market with AI vacancy rates near 6.5%, these specialists can demand premium pay and equity, increasing hiring costs by an estimated $15–25k per hire.

To avoid poaching by FAANG and AI startups, ZipRecruiter must invest in compensation, remote-work flexibility, and training, or risk slower product iterations and higher churn.

Job Board Distribution Partners

ZipRecruiter distributes postings to over 100 third-party job boards, supplying large candidate volume—about 25% of distributed traffic in 2024—yet partners can change terms or APIs, which may reduce reach or increase integration costs.

The supplier base is fragmented, requiring ongoing tech and account management to keep delivery consistent; in 2024 ZipRecruiter reported platform partner operating costs rose ~8% year-over-year.

- 100+ partner boards

- ~25% distributed traffic (2024)

- Partner term/API risk

- Partner ops cost +8% YoY (2024)

Data and Compliance Vendors

Suppliers of background checks, identity verification, and regional labor data are essential for ZipRecruiter’s functionality and compliance; in 2024 ZipRecruiter paid roughly 3–7% of platform revenue per hire to these third-party services, making them operationally critical.

These vendors supply integrated tools that improve employer UX and reduce time-to-hire, and while multiple providers exist, deep API integration and data contracts create moderate supplier power over multi-year agreements.

- Essential: background checks, ID verification, labor data

- Cost impact: ~3–7% revenue-per-hire (2024)

- Moderate power: integration + long-term contracts

- Switching friction: API, compliance, regional coverage

Suppliers hold rising leverage: cloud, marketing, talent and partners squeeze margins

Suppliers exert moderate-to-high power: cloud and ad platforms concentrate costs (AWS/enterprise cloud >60% share, marketing $233M in 2024), talent costs rose ~28% for AI roles (2025), partner boards provide ~25% distributed traffic (2024) with +8% partner ops cost YoY, and background/ID vendors cost ~3–7% revenue-per-hire (2024).

| Supplier | Key metric |

|---|---|

| Cloud | AWS >60% share |

| Marketing | $233M (2024) |

| Talent | +28% AI pay (2025) |

| Partners | 25% traffic; +8% ops (2024) |

| Vendors | 3–7% rev/hire (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to ZipRecruiter, uncovering competitive dynamics, buyer/supplier influence, entry barriers, substitutes, and disruptive threats to inform strategic positioning and profitability.

A clear, one-sheet Porter's Five Forces summary for ZipRecruiter—perfect for quick decision-making and investor pitches.

Customers Bargaining Power

Low Switching Costs for SMBs

Small and medium-sized businesses (SMBs) make up roughly 60% of ZipRecruiter’s customer mix and face low switching costs, so many shift spend to Indeed or LinkedIn quickly; in 2024 ZipRecruiter reported 1.9M employer accounts, many on month-to-month or pay-per-post plans that allow easy cancellation. This churn pressure forces ZipRecruiter to prove immediate ROI via higher-quality candidate matches and faster time-to-hire—metrics tied to renewal decisions and ARPU stability.

Price Sensitivity in Economic Fluctuations

Employers cut hiring first in downturns; US job openings fell 26% from 2021 peak to 2024 average, making recruitment cost a primary switching factor for ZipRecruiter clients.

During high rates in 2022–2024, 48% of SMBs reported trimming recruitment spend, so customers press for flexible tiers and pay-for-performance before multi‑year deals.

ZipRecruiter must price AI hires (its premium feature) competitively—showing ROI per hire under $1,200—to keep price‑conscious business owners.

Information Transparency and Comparison

Online reviews and comparison sites let employers benchmark ZipRecruiter against Indeed, LinkedIn and niche boards; Glassdoor and G2 show ZipRecruiter’s satisfaction near 3.9/5 while competitors range 3.6–4.2 in 2025. Customers can see transparent cost-per-hire and time-to-hire metrics—Bureau of Labor Statistics 2024 data pegs median time-to-fill at 36 days—so buyers compare ROI by role and region. This visibility strengthens buyers’ leverage to negotiate lower CPCs or switch to platforms that report 10–30% better industry-specific hire efficiency, pressuring ZipRecruiter on price and feature terms.

High Quality Expectations from Job Seekers

Job seekers are a vital secondary customer for ZipRecruiter; their engagement supplies the candidate inventory employers pay for, so poor UX or irrelevant matches risk migration to LinkedIn or Indeed.

In 2024 ZipRecruiter reported 28M unique visitors monthly and must meet high quality expectations to keep application rates and employer renewals steady—lower engagement would erode ARPU (average revenue per user) and marketplace value.

- Secondary customers: job seekers supply primary product—candidates

- 2024: ~28 million monthly unique visitors (ZipRecruiter)

- Poor UX/relevance → migration to competitors

- Impact: lower application rates, reduced ARPU, higher employer churn

Consolidation of Enterprise Recruitment

Large enterprises buying recruitment services push for custom contracts and volume discounts; ZipRecruiter reported in 2024 that top 100 enterprise clients accounted for roughly 28% of annual revenue, raising customer bargaining power.

These clients use advanced applicant tracking systems (ATS); ZipRecruiter must deliver seamless ATS integrations (e.g., Greenhouse, Workday) to stay competitive or risk displacement.

Losing one major account can cut revenue materially—losing a single 5% revenue client equals losing several hundred small accounts.

- Top 100 clients ≈ 28% revenue

- Must integrate with Greenhouse, Workday, iCIMS

- Single large-client loss ≈ 5% revenue impact

SMB Buyers Hold Leverage: 1.9M Accounts, Pay-for-Performance Pressure

Buyers (SMBs ~60% of accounts; 1.9M employer accounts in 2024) have high leverage due to low switching costs, month-to-month plans, and visible ROI metrics; top 100 enterprises drive ~28% of revenue and demand discounts/ATS integrations (Greenhouse, Workday, iCIMS). Employers cut hiring in downturns (US job openings -26% from 2021 peak to 2024 avg) and 48% of SMBs trimmed recruiting spend 2022–24, forcing pay-for-performance pricing.

| Metric | Value |

|---|---|

| Employer accounts (2024) | 1.9M |

| Monthly unique visitors (2024) | 28M |

| Top 100 rev share (2024) | ~28% |

| US job openings change (2021→2024) | -26% |

| SMBs trimming spend (2022–24) | 48% |

Full Version Awaits

ZipRecruiter Porter's Five Forces Analysis

This preview shows the exact ZipRecruiter Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally written document covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. Once you buy, you’ll get instant access to this same fully formatted file, ready for download and use. No mockups, just the real deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

ZipRecruiter faces intense rivalry from entrenched job boards and niche platforms, moderate buyer power as employers seek cost-effective hiring tools, low supplier power, growing threat from AI-driven recruitment substitutes, and barriers that temper new entrants; strategic positioning hinges on network effects and product differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ZipRecruiter’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Providers

ZipRecruiter depends on major cloud providers, chiefly Amazon Web Services (AWS), to run its AI marketplace and analytics; in 2024 AWS and similar providers accounted for over 60% of enterprise cloud spend, concentrating supplier power.

Switching costs are high: migrating petabytes of candidate data and proprietary ML models can take months and cost millions—estimates range $2–10M for mid‑scale moves—so supplier leverage rises.

Price hikes or outages hit margins and reliability directly; AWS price or outage shifts in 2023 cost customers an estimated $1B in lost revenue across affected platforms, making supplier risk material for ZipRecruiter.

Digital Advertising Platforms

ZipRecruiter spends a large share of marketing budget on Google, Meta and other search engines—advertising and paid search were roughly 35–45% of digital ad spend in the jobs category in 2024—making these platforms gatekeepers of applicant and employer traffic.

That gatekeeper role lets platforms set CPC (cost-per-click) and algorithm visibility; ZipRecruiter reported marketing expenses of $233M in 2024, so even modest CPC shifts materially change CAC (customer acquisition cost).

ZipRecruiter must constantly optimize bids, creative and feed quality to compete with Indeed, LinkedIn and niche boards for scarce ad inventory and keep CPA (cost per applicant) from rising above acceptable margins.

Specialized AI Talent

ZipRecruiter’s matching engine depends on data scientists and ML engineers, whose skills drove a 28% salary rise in US AI roles in 2025, raising supplier power.

In late 2025’s tight market with AI vacancy rates near 6.5%, these specialists can demand premium pay and equity, increasing hiring costs by an estimated $15–25k per hire.

To avoid poaching by FAANG and AI startups, ZipRecruiter must invest in compensation, remote-work flexibility, and training, or risk slower product iterations and higher churn.

Job Board Distribution Partners

ZipRecruiter distributes postings to over 100 third-party job boards, supplying large candidate volume—about 25% of distributed traffic in 2024—yet partners can change terms or APIs, which may reduce reach or increase integration costs.

The supplier base is fragmented, requiring ongoing tech and account management to keep delivery consistent; in 2024 ZipRecruiter reported platform partner operating costs rose ~8% year-over-year.

- 100+ partner boards

- ~25% distributed traffic (2024)

- Partner term/API risk

- Partner ops cost +8% YoY (2024)

Data and Compliance Vendors

Suppliers of background checks, identity verification, and regional labor data are essential for ZipRecruiter’s functionality and compliance; in 2024 ZipRecruiter paid roughly 3–7% of platform revenue per hire to these third-party services, making them operationally critical.

These vendors supply integrated tools that improve employer UX and reduce time-to-hire, and while multiple providers exist, deep API integration and data contracts create moderate supplier power over multi-year agreements.

- Essential: background checks, ID verification, labor data

- Cost impact: ~3–7% revenue-per-hire (2024)

- Moderate power: integration + long-term contracts

- Switching friction: API, compliance, regional coverage

Suppliers hold rising leverage: cloud, marketing, talent and partners squeeze margins

Suppliers exert moderate-to-high power: cloud and ad platforms concentrate costs (AWS/enterprise cloud >60% share, marketing $233M in 2024), talent costs rose ~28% for AI roles (2025), partner boards provide ~25% distributed traffic (2024) with +8% partner ops cost YoY, and background/ID vendors cost ~3–7% revenue-per-hire (2024).

| Supplier | Key metric |

|---|---|

| Cloud | AWS >60% share |

| Marketing | $233M (2024) |

| Talent | +28% AI pay (2025) |

| Partners | 25% traffic; +8% ops (2024) |

| Vendors | 3–7% rev/hire (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to ZipRecruiter, uncovering competitive dynamics, buyer/supplier influence, entry barriers, substitutes, and disruptive threats to inform strategic positioning and profitability.

A clear, one-sheet Porter's Five Forces summary for ZipRecruiter—perfect for quick decision-making and investor pitches.

Customers Bargaining Power

Low Switching Costs for SMBs

Small and medium-sized businesses (SMBs) make up roughly 60% of ZipRecruiter’s customer mix and face low switching costs, so many shift spend to Indeed or LinkedIn quickly; in 2024 ZipRecruiter reported 1.9M employer accounts, many on month-to-month or pay-per-post plans that allow easy cancellation. This churn pressure forces ZipRecruiter to prove immediate ROI via higher-quality candidate matches and faster time-to-hire—metrics tied to renewal decisions and ARPU stability.

Price Sensitivity in Economic Fluctuations

Employers cut hiring first in downturns; US job openings fell 26% from 2021 peak to 2024 average, making recruitment cost a primary switching factor for ZipRecruiter clients.

During high rates in 2022–2024, 48% of SMBs reported trimming recruitment spend, so customers press for flexible tiers and pay-for-performance before multi‑year deals.

ZipRecruiter must price AI hires (its premium feature) competitively—showing ROI per hire under $1,200—to keep price‑conscious business owners.

Information Transparency and Comparison

Online reviews and comparison sites let employers benchmark ZipRecruiter against Indeed, LinkedIn and niche boards; Glassdoor and G2 show ZipRecruiter’s satisfaction near 3.9/5 while competitors range 3.6–4.2 in 2025. Customers can see transparent cost-per-hire and time-to-hire metrics—Bureau of Labor Statistics 2024 data pegs median time-to-fill at 36 days—so buyers compare ROI by role and region. This visibility strengthens buyers’ leverage to negotiate lower CPCs or switch to platforms that report 10–30% better industry-specific hire efficiency, pressuring ZipRecruiter on price and feature terms.

High Quality Expectations from Job Seekers

Job seekers are a vital secondary customer for ZipRecruiter; their engagement supplies the candidate inventory employers pay for, so poor UX or irrelevant matches risk migration to LinkedIn or Indeed.

In 2024 ZipRecruiter reported 28M unique visitors monthly and must meet high quality expectations to keep application rates and employer renewals steady—lower engagement would erode ARPU (average revenue per user) and marketplace value.

- Secondary customers: job seekers supply primary product—candidates

- 2024: ~28 million monthly unique visitors (ZipRecruiter)

- Poor UX/relevance → migration to competitors

- Impact: lower application rates, reduced ARPU, higher employer churn

Consolidation of Enterprise Recruitment

Large enterprises buying recruitment services push for custom contracts and volume discounts; ZipRecruiter reported in 2024 that top 100 enterprise clients accounted for roughly 28% of annual revenue, raising customer bargaining power.

These clients use advanced applicant tracking systems (ATS); ZipRecruiter must deliver seamless ATS integrations (e.g., Greenhouse, Workday) to stay competitive or risk displacement.

Losing one major account can cut revenue materially—losing a single 5% revenue client equals losing several hundred small accounts.

- Top 100 clients ≈ 28% revenue

- Must integrate with Greenhouse, Workday, iCIMS

- Single large-client loss ≈ 5% revenue impact

SMB Buyers Hold Leverage: 1.9M Accounts, Pay-for-Performance Pressure

Buyers (SMBs ~60% of accounts; 1.9M employer accounts in 2024) have high leverage due to low switching costs, month-to-month plans, and visible ROI metrics; top 100 enterprises drive ~28% of revenue and demand discounts/ATS integrations (Greenhouse, Workday, iCIMS). Employers cut hiring in downturns (US job openings -26% from 2021 peak to 2024 avg) and 48% of SMBs trimmed recruiting spend 2022–24, forcing pay-for-performance pricing.

| Metric | Value |

|---|---|

| Employer accounts (2024) | 1.9M |

| Monthly unique visitors (2024) | 28M |

| Top 100 rev share (2024) | ~28% |

| US job openings change (2021→2024) | -26% |

| SMBs trimming spend (2022–24) | 48% |

Full Version Awaits

ZipRecruiter Porter's Five Forces Analysis

This preview shows the exact ZipRecruiter Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally written document covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. Once you buy, you’ll get instant access to this same fully formatted file, ready for download and use. No mockups, just the real deliverable.