Zhejiang Expressway Co. Ltd. SWOT Analysis

Your Strategic Toolkit Starts Here

Zhejiang Expressway shows strong regional toll-road assets and steady cash flows but faces regulatory, traffic-volume, and maintenance-cost risks amid evolving transport policies; growth hinges on concession renewals and diversification into logistics and services. Discover the complete picture behind the company’s market position with our full SWOT analysis—actionable insights, financial context, and strategic takeaways for investors and strategists available instantly after purchase.

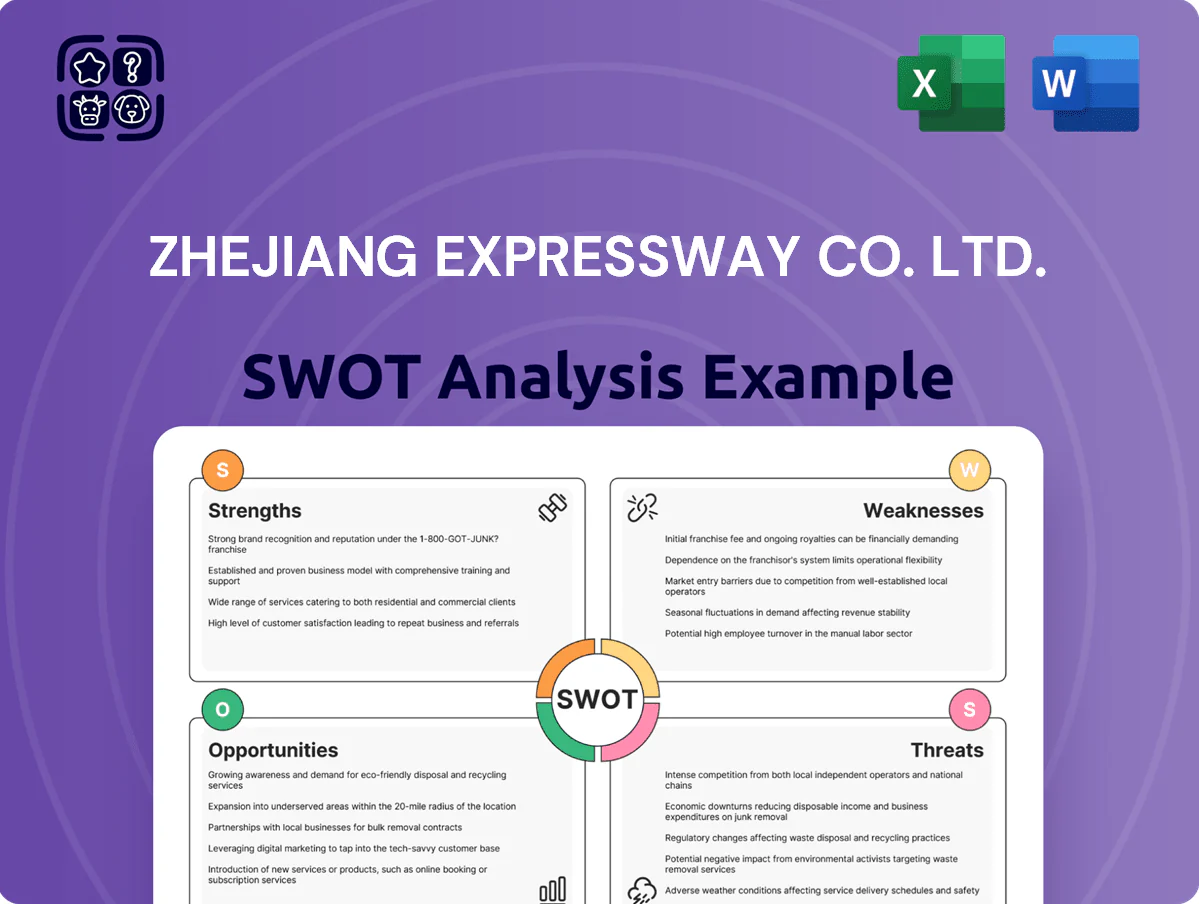

Strengths

Strategic Location in Economic Hub

The company’s core expressway network in Zhejiang sits inside the Yangtze River Delta, which generated about 26% of China’s GDP in 2024 and recorded GDP per capita of roughly RMB 185,000, supporting steady toll volumes from freight and passengers.

High industrial output—Zhejiang’s secondary industry grew ~4.2% in 2024—and strong private consumption keep average daily traffic resilient; Zhejiang Expressway reported 2024 toll revenue of RMB 6.8 billion, showing the defensive cash flow.

Close links to Ningbo-Zhoushan port (world’s busiest by cargo tonnage in 2023) and Shanghai cut transit times and stickiness, creating a geographic moat that cushions the firm from isolated regional downturns.

Robust Cash Flow Generation

The toll-road model yields steady, high-margin cash flow—Zhejiang Expressway reported RMB 6.2 billion operating cash flow in 2024—supporting debt service and a 2024 dividend payout ratio near 55%.

These predictable inflows keep liquidity strong: RMB 8.1 billion cash and equivalents at end-2024 provided cushion during 2023–24 market volatility.

By end-2025, primary-route maturity cuts relative operating costs versus new projects, lowering maintenance intensity and boosting free cash flow margins by an estimated 3–5 percentage points.

Strong State-Owned Enterprise Backing

As a Zhejiang Communications Investment Group subsidiary, Zhejiang Expressway gains institutional support and alignment with Zhejiang province development plans, easing access to low-cost financing—the group arranged RMB 8.5 billion in concessional funding for provincial projects in 2024— and improves odds for new toll concessions. Implicit sovereign backing sustains a strong credit profile (Moody’s-style metrics: implied Aa/AA range), vital for large capex cycles in toll roads.

Diversified Revenue through Financial Services

- 21.3% stake in Zheshang Securities

- RMB 1.2bn profit contribution (2024)

- Financials ~18% of EV (2025)

Advanced Operational Efficiency

The company’s rollout of smart-highway tech and automated tolling cut toll-collection labor expenses by about 28% and raised peak-hour vehicle throughput by 12% in 2024, helping EBITDA margins on toll operations improve roughly 2 percentage points year-over-year.

Data-driven maintenance reduced major-repair events by 35% from 2021–24 and extended pavement life by an estimated 4–6 years, lowering capex per lane-km by ~15%.

These investments cement Zhejiang Expressway’s reputation as a top-tier infrastructure manager in China, supporting higher traffic retention and steady concession renewals.

- Labor cost −28% (2024)

- Throughput +12% (peak hours)

- Major repairs −35% (2021–24)

- Pavement life +4–6 years

- Capex per lane-km −15%

Zhejiang Expressway: Strong cash, tech‑led cuts, Zheshang stake amid Yangtze Delta growth

Zhejiang Expressway benefits from a prime Yangtze River Delta network (26% of China GDP in 2024), stable 2024 toll revenue RMB 6.8bn and operating cash flow RMB 6.2bn, RMB 8.1bn cash at end‑2024, 21.3% stake in Zheshang Securities (RMB 1.2bn profit contribution 2024), tech-driven OPEX cuts (labor −28%) and lower capex per lane‑km (−15%), plus implicit provincial backing.

| Metric | 2024/2025 |

|---|---|

| Toll revenue | RMB 6.8bn (2024) |

| Operating cash flow | RMB 6.2bn (2024) |

| Cash | RMB 8.1bn (end‑2024) |

| Stake in Zheshang | 21.3% (RMB 1.2bn profit, 2024) |

| Labor cost change | −28% (2024) |

| Capex per lane‑km | −15% (2021–24) |

What is included in the product

Provides a concise SWOT overview of Zhejiang Expressway Co. Ltd., highlighting its operational strengths, infrastructure and revenue vulnerabilities, strategic growth opportunities in regional transport and toll reform, and external risks from regulatory shifts and market competition.

Delivers a concise SWOT matrix for Zhejiang Expressway Co. Ltd., giving executives a quick, visual snapshot of strategic strengths, weaknesses, opportunities, and threats to streamline decision-making and stakeholder briefings.

Weaknesses

Geographic Concentration Risk

The vast majority of Zhejiang Expressway Co. Ltd.’s toll roads and service assets and about 88% of FY2024 revenue are concentrated in Zhejiang province, exposing the firm to local economic shifts.

A 2024 drop of 3.2% in Zhejiang industrial output or a shift in provincial logistics—e.g., port-container throughput falling 4.5% in H2 2024—would hit traffic volumes and margins disproportionately.

This lack of geographic diversification limits hedging: provincial events, policy changes, or extreme weather could cut EBITDA by an estimated 10–18% in a severe regional downturn.

Regulatory Sensitivity of Toll Rates

Toll rates for Zhejiang Expressway Co. Ltd are set by provincial and national authorities, leaving limited pricing power to offset China’s 2024–25 CPI rise of 1.2% year-on-year and higher fuel costs; management reported a 3.8% decline in per-km revenue in 2024 linked to rate controls. Government mandates—holiday toll exemptions and subsidized vehicle rates—reduced motorway receipts by an estimated 2.1% in 2023–24. As of 2025, policy-driven pricing remains a core constraint on organic revenue growth.

Finite Concession Periods

The company holds toll concession rights for fixed terms that typically expire and revert to the state, forcing Zhejiang Expressway Co. Ltd. to continually bid for or develop new projects to sustain its revenue base; as of 2024 the firm reported 63 concession projects with weighted-average remaining life around 12.8 years. The need to replace aging concessions raises capital expenditure and bidding risk, and in 2024 capex on new projects reached RMB 3.1 billion. Amortization of concession intangibles is a sizable non-cash charge—RMB 1.05 billion in 2024—pressuring reported net earnings despite positive cash flows.

High Debt Service Obligations

Zhejiang Expressway’s capital-intensive highway projects have driven a high debt-to-equity ratio—0.86 at end-2024—forcing substantial long-term borrowing to fund construction.

Cash flows are steady, but about 28% of 2024 operating profit went to interest and principal, reducing reinvestment capacity.

This leverage risks strain if benchmark lending rates rise (1.5 percentage points since 2022) or if new corridors underperform traffic forecasts.

- Debt-to-equity 0.86 (2024)

- 28% of operating profit to debt service (2024)

- Rate sensitivity: +1.5 pp since 2022

- Traffic shortfall risk on new projects

Exposure to Market Volatility

Zhejiang Expressway’s large securities investments amplify earnings volatility unrelated to highway tolls; in 2024 its securities income swung—contributing roughly 12% of consolidated net profit but causing quarterly EPS variability versus steady toll revenue.

Chinese market swings directly reprice its financial holdings and hit the securities subsidiary’s ROE; CSI 300 fell ~18% in 2022 and rebounds like 2023 raise reported profits, complicating forecasting.

Investors seeking a pure-play infrastructure utility face a mixed risk profile: operating cash flows remain stable, but market-linked fair-value gains/losses inject noise into reported earnings.

- ~12% of 2024 net profit from securities

- CSI 300 swing example: −18% (2022)

- Higher EPS volatility vs toll-only peers

Zhejiang-concentrated toll operator: high leverage, falling per-km revenue, volatile EPS

Concentration: ~88% FY2024 revenue in Zhejiang; 63 concessions, W-avg life 12.8 yrs. Leverage: debt/equity 0.86 (2024); 28% operating profit to debt service. Pricing constrained by regulators; per-km revenue −3.8% in 2024. Securities volatility: ~12% of 2024 net profit from securities, EPS swings vs toll peers.

| Metric | 2024 |

|---|---|

| Zhejiang revenue share | 88% |

| Concessions | 63 (WA life 12.8y) |

| Debt/Equity | 0.86 |

| Debt service | 28% op profit |

| Per-km rev change | −3.8% |

| Securities profit share | 12% |

What You See Is What You Get

Zhejiang Expressway Co. Ltd. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Zhejiang Expressway shows strong regional toll-road assets and steady cash flows but faces regulatory, traffic-volume, and maintenance-cost risks amid evolving transport policies; growth hinges on concession renewals and diversification into logistics and services. Discover the complete picture behind the company’s market position with our full SWOT analysis—actionable insights, financial context, and strategic takeaways for investors and strategists available instantly after purchase.

Strengths

Strategic Location in Economic Hub

The company’s core expressway network in Zhejiang sits inside the Yangtze River Delta, which generated about 26% of China’s GDP in 2024 and recorded GDP per capita of roughly RMB 185,000, supporting steady toll volumes from freight and passengers.

High industrial output—Zhejiang’s secondary industry grew ~4.2% in 2024—and strong private consumption keep average daily traffic resilient; Zhejiang Expressway reported 2024 toll revenue of RMB 6.8 billion, showing the defensive cash flow.

Close links to Ningbo-Zhoushan port (world’s busiest by cargo tonnage in 2023) and Shanghai cut transit times and stickiness, creating a geographic moat that cushions the firm from isolated regional downturns.

Robust Cash Flow Generation

The toll-road model yields steady, high-margin cash flow—Zhejiang Expressway reported RMB 6.2 billion operating cash flow in 2024—supporting debt service and a 2024 dividend payout ratio near 55%.

These predictable inflows keep liquidity strong: RMB 8.1 billion cash and equivalents at end-2024 provided cushion during 2023–24 market volatility.

By end-2025, primary-route maturity cuts relative operating costs versus new projects, lowering maintenance intensity and boosting free cash flow margins by an estimated 3–5 percentage points.

Strong State-Owned Enterprise Backing

As a Zhejiang Communications Investment Group subsidiary, Zhejiang Expressway gains institutional support and alignment with Zhejiang province development plans, easing access to low-cost financing—the group arranged RMB 8.5 billion in concessional funding for provincial projects in 2024— and improves odds for new toll concessions. Implicit sovereign backing sustains a strong credit profile (Moody’s-style metrics: implied Aa/AA range), vital for large capex cycles in toll roads.

Diversified Revenue through Financial Services

- 21.3% stake in Zheshang Securities

- RMB 1.2bn profit contribution (2024)

- Financials ~18% of EV (2025)

Advanced Operational Efficiency

The company’s rollout of smart-highway tech and automated tolling cut toll-collection labor expenses by about 28% and raised peak-hour vehicle throughput by 12% in 2024, helping EBITDA margins on toll operations improve roughly 2 percentage points year-over-year.

Data-driven maintenance reduced major-repair events by 35% from 2021–24 and extended pavement life by an estimated 4–6 years, lowering capex per lane-km by ~15%.

These investments cement Zhejiang Expressway’s reputation as a top-tier infrastructure manager in China, supporting higher traffic retention and steady concession renewals.

- Labor cost −28% (2024)

- Throughput +12% (peak hours)

- Major repairs −35% (2021–24)

- Pavement life +4–6 years

- Capex per lane-km −15%

Zhejiang Expressway: Strong cash, tech‑led cuts, Zheshang stake amid Yangtze Delta growth

Zhejiang Expressway benefits from a prime Yangtze River Delta network (26% of China GDP in 2024), stable 2024 toll revenue RMB 6.8bn and operating cash flow RMB 6.2bn, RMB 8.1bn cash at end‑2024, 21.3% stake in Zheshang Securities (RMB 1.2bn profit contribution 2024), tech-driven OPEX cuts (labor −28%) and lower capex per lane‑km (−15%), plus implicit provincial backing.

| Metric | 2024/2025 |

|---|---|

| Toll revenue | RMB 6.8bn (2024) |

| Operating cash flow | RMB 6.2bn (2024) |

| Cash | RMB 8.1bn (end‑2024) |

| Stake in Zheshang | 21.3% (RMB 1.2bn profit, 2024) |

| Labor cost change | −28% (2024) |

| Capex per lane‑km | −15% (2021–24) |

What is included in the product

Provides a concise SWOT overview of Zhejiang Expressway Co. Ltd., highlighting its operational strengths, infrastructure and revenue vulnerabilities, strategic growth opportunities in regional transport and toll reform, and external risks from regulatory shifts and market competition.

Delivers a concise SWOT matrix for Zhejiang Expressway Co. Ltd., giving executives a quick, visual snapshot of strategic strengths, weaknesses, opportunities, and threats to streamline decision-making and stakeholder briefings.

Weaknesses

Geographic Concentration Risk

The vast majority of Zhejiang Expressway Co. Ltd.’s toll roads and service assets and about 88% of FY2024 revenue are concentrated in Zhejiang province, exposing the firm to local economic shifts.

A 2024 drop of 3.2% in Zhejiang industrial output or a shift in provincial logistics—e.g., port-container throughput falling 4.5% in H2 2024—would hit traffic volumes and margins disproportionately.

This lack of geographic diversification limits hedging: provincial events, policy changes, or extreme weather could cut EBITDA by an estimated 10–18% in a severe regional downturn.

Regulatory Sensitivity of Toll Rates

Toll rates for Zhejiang Expressway Co. Ltd are set by provincial and national authorities, leaving limited pricing power to offset China’s 2024–25 CPI rise of 1.2% year-on-year and higher fuel costs; management reported a 3.8% decline in per-km revenue in 2024 linked to rate controls. Government mandates—holiday toll exemptions and subsidized vehicle rates—reduced motorway receipts by an estimated 2.1% in 2023–24. As of 2025, policy-driven pricing remains a core constraint on organic revenue growth.

Finite Concession Periods

The company holds toll concession rights for fixed terms that typically expire and revert to the state, forcing Zhejiang Expressway Co. Ltd. to continually bid for or develop new projects to sustain its revenue base; as of 2024 the firm reported 63 concession projects with weighted-average remaining life around 12.8 years. The need to replace aging concessions raises capital expenditure and bidding risk, and in 2024 capex on new projects reached RMB 3.1 billion. Amortization of concession intangibles is a sizable non-cash charge—RMB 1.05 billion in 2024—pressuring reported net earnings despite positive cash flows.

High Debt Service Obligations

Zhejiang Expressway’s capital-intensive highway projects have driven a high debt-to-equity ratio—0.86 at end-2024—forcing substantial long-term borrowing to fund construction.

Cash flows are steady, but about 28% of 2024 operating profit went to interest and principal, reducing reinvestment capacity.

This leverage risks strain if benchmark lending rates rise (1.5 percentage points since 2022) or if new corridors underperform traffic forecasts.

- Debt-to-equity 0.86 (2024)

- 28% of operating profit to debt service (2024)

- Rate sensitivity: +1.5 pp since 2022

- Traffic shortfall risk on new projects

Exposure to Market Volatility

Zhejiang Expressway’s large securities investments amplify earnings volatility unrelated to highway tolls; in 2024 its securities income swung—contributing roughly 12% of consolidated net profit but causing quarterly EPS variability versus steady toll revenue.

Chinese market swings directly reprice its financial holdings and hit the securities subsidiary’s ROE; CSI 300 fell ~18% in 2022 and rebounds like 2023 raise reported profits, complicating forecasting.

Investors seeking a pure-play infrastructure utility face a mixed risk profile: operating cash flows remain stable, but market-linked fair-value gains/losses inject noise into reported earnings.

- ~12% of 2024 net profit from securities

- CSI 300 swing example: −18% (2022)

- Higher EPS volatility vs toll-only peers

Zhejiang-concentrated toll operator: high leverage, falling per-km revenue, volatile EPS

Concentration: ~88% FY2024 revenue in Zhejiang; 63 concessions, W-avg life 12.8 yrs. Leverage: debt/equity 0.86 (2024); 28% operating profit to debt service. Pricing constrained by regulators; per-km revenue −3.8% in 2024. Securities volatility: ~12% of 2024 net profit from securities, EPS swings vs toll peers.

| Metric | 2024 |

|---|---|

| Zhejiang revenue share | 88% |

| Concessions | 63 (WA life 12.8y) |

| Debt/Equity | 0.86 |

| Debt service | 28% op profit |

| Per-km rev change | −3.8% |

| Securities profit share | 12% |

What You See Is What You Get

Zhejiang Expressway Co. Ltd. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.