Zijin Mining PESTLE Analysis

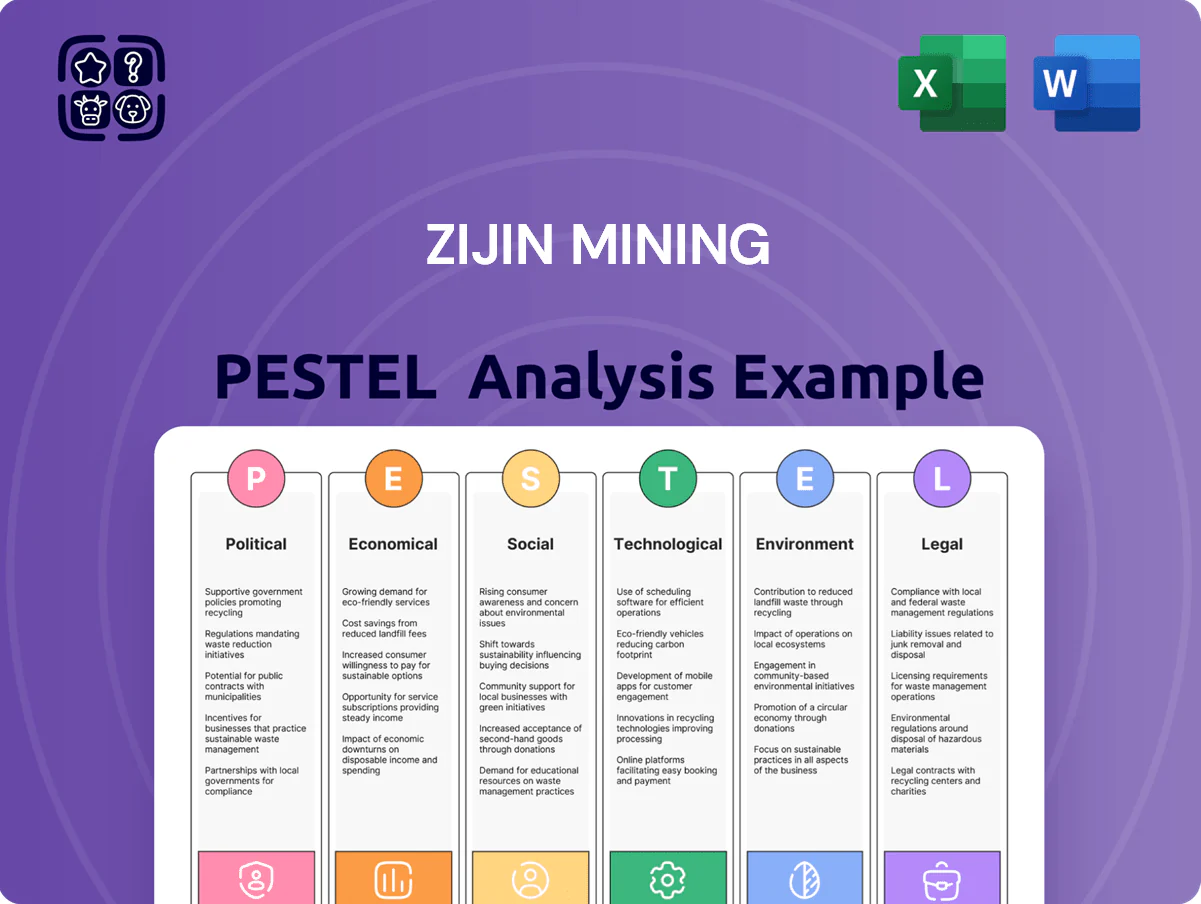

Make Smarter Strategic Decisions with a Complete PESTEL View

Zijin Mining faces regulatory scrutiny, commodity price volatility, and rising ESG expectations that reshape operations and growth opportunities; our concise PESTLE highlights these forces and their strategic implications. Purchase the full PESTLE to access actionable risk assessments, scenario-ready insights, and ready-to-use slides for investors and strategists.

Political factors

Geopolitical Risk and Resource Nationalism

Zijin Mining operates across 20+ countries where political instability and resource nationalism threaten asset security and continuity, notably in parts of Africa and South America.

By end-2025, several host states have proposed higher royalties or compulsory state stakes—estimates suggest potential revenue reallocation of 5–15% for affected projects.

Heightened regulatory scrutiny and renegotiation risks could affect Zijin’s EBITDA margins on exposed assets unless mitigated.

Robust risk mitigation—joint-venture frameworks, political risk insurance, and intensified government engagement—remains critical to preserve long-term operations.

Strategic Alignment with National Interests

Zijin Mining’s strategic alignment with China’s push for critical minerals secures preferential access to state-backed financing—China Development Bank and policy banks supported deals totaling over $5bn for overseas copper and lithium projects in 2023–2025—facilitating major acquisitions and project capex.

Domestic political support reduces funding costs and regulatory friction for expansion, but ties to Beijing increase exposure to sanctions, export controls and scrutiny from the US, EU and Australia that tightened foreign investment reviews in 2024–25.

Geopolitical risks have already delayed or reshaped several deals, forcing Zijin to enhance transparency, local partnerships and ESG compliance to meet host-country requirements and mitigate trade-barrier impacts.

The firm must balance its role as a national champion with global corporate governance norms to sustain access to Western markets and downstream customers amid rising supply-chain security policies.

International Trade Policy and Sanctions

Global trade dynamics and sanctions targeting Chinese firms have strained Zijin Mining's supply chain, with 2024 export controls and tariffs raising compliance costs that risk disrupting shipments of refined copper and gold, which made up over 58% of 2024 metal revenues. The company must track evolving trade agreements and protectionist measures that could limit exports or imports of specialized equipment—affecting capital expenditure that reached US$2.3 billion in 2024. By 2025, regionalized supply chains push Zijin toward localized procurement and sales in Asia-Pacific and Africa to reduce transit risk. Strategic market diversification into Southeast Asia and Europe mitigates localized political friction and preserves access to key smelters and customers.

Host Country Regulatory Stability

Predictability of regimes in Serbia, Colombia and the DRC is critical for Zijin’s capital-intensive projects; political risk flags rose in 2024 with Serbia’s regulatory reviews, Colombia’s 2024 mining tax debates and DRC permitting backlogs delaying projects by months.

Zijin spends tens of millions yearly on government relations and community programs to anticipate policy shifts and protect permits; sudden populist moves have historically prompted mining code revisions and occasional license suspensions.

Zijin maintains formal neutrality while funding local infrastructure—roads, schools, clinics—to reduce social friction and increase government goodwill, a strategy that helped secure extensions or approvals in 2023–2025.

- Key markets: Serbia, Colombia, DRC — high regulatory volatility

- Annual GR/community spend: tens of millions USD

- Delays: permit backlogs causing multi-month project slowdowns

- Strategy: neutrality + local infrastructure to secure legal operating rights

Global Security and Conflict Zones

Operating in conflict-prone regions forces Zijin to deploy advanced security measures and pay rising insurance premiums—global political risk insurance rates rose ~18% in 2024–25—raising per-project up-front security costs by an estimated 5–12% in frontier markets.

Zijin faces ethical/logistical pressures to align operations with UN Guiding Principles on Business and Human Rights while managing evacuations, contractor vetting, and protective infrastructure to limit workforce exposure.

Robust crisis management, local community integration and grievance mechanisms have reduced stoppage days by up to 30% at some high-risk sites; failure increases capital-at-risk and operational disruption probabilities.

- 2024–25 security/insurance hike ~18%

- Per-project security cost rise 5–12%

- Stoppage days cut up to 30% with strong community programs

Zijin faces rising resource-nationalism, higher PRI and multi-month permit delays

Zijin faces heightened resource-nationalism and export controls that risk reallocating 5–15% of project revenues and raised political risk insurance ~18% in 2024–25, increasing per-project security costs 5–12%; state-backed Chinese financing (>$5bn 2023–25) lowers funding costs but raises Western scrutiny; key markets Serbia, Colombia, DRC show high regulatory volatility and permit backlogs causing multi-month delays; mitigation: JVs, PRI, local infrastructure spending (tens of millions USD/yr).

| Metric | Value |

|---|---|

| Revenue reallocation risk | 5–15% |

| PRI rate change 2024–25 | +~18% |

| Per-project security cost rise | 5–12% |

| China-backed financing 2023–25 | >$5bn |

| Annual GR/community spend | Tens of millions USD |

What is included in the product

Explores how macro-environmental factors uniquely affect Zijin Mining across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Concise PESTLE summary of Zijin Mining that’s visually segmented for quick meetings, easily drop‑in to slides or reports, editable for regional/context notes, and structured to aid rapid risk assessment and cross‑team alignment.

Economic factors

Commodity Price Volatility

The financials of Zijin Mining are highly sensitive to gold, copper and zinc prices, with metals accounting for over 80% of revenue; copper demand remained robust through late 2025 amid the energy transition, supporting average LME copper prices near USD 9,000/ton in 2025, while gold averaged about USD 1,900/oz as an inflation hedge. Price swings drove EBIT volatility—Zijin reported 2024 attributable profit down 12% YoY—requiring disciplined cost control. The company employs strategic hedging and a diversified portfolio across China, Kyrgyzstan and Serbia to stabilize cash flows, with hedges covering a portion of production and lowering realized price exposure.

Global Inflation and Operating Costs

Persistent inflation in 2024–25 pushed energy, labor and input costs up 6–12% y/y in major mining regions, raising Zijin’s unit cash costs and squeezing margins.

Zijin must optimize supply chains and efficiency—targeting lower AISC—to retain low-cost producer status amid cost inflation and weaker ore grades.

Higher global real rates have raised cost of capital, slowing new mine capex decisions and prioritizing projects with IRRs above rising hurdles.

Focusing on high-grade assets and automation (e.g., mill upgrades, remote operations) aims to offset inflationary erosion and protect margins.

Currency Exchange Rate Fluctuations

With operations across China, Africa, Asia-Pacific and Central Asia, Zijin faces currency risk across CNY, USD and multiple local currencies; in 2024 foreign exchange losses contributed to a RMB 1.2 billion swing in net profit for Chinese miners industry-wide. Exchange-rate moves alter the RMB value of overseas assets and increase USD-denominated debt servicing costs, especially after 2023–24 USD strength. Zijin uses forwards, cross-currency swaps and natural hedges—matching revenue/cost currencies—to mitigate volatility. A stronger yuan or weaker host-country currencies compresses consolidated revenue and reported profitability on RMB financial statements.

Demand Driven by the Green Energy Transition

The global shift to renewables and EVs has driven structural demand for copper and lithium, with copper demand for clean energy estimated to grow 6–8% CAGR to 2030 and lithium demand forecast to rise ~20% CAGR to 2025.

Zijin has expanded its lithium portfolio via acquisitions and JV stakes, targeting >100 kt LCE capacity by 2025 to capture battery supply growth and enhance valuation.

Scaling production by 2025 is a primary driver of Zijin’s market multiple; emerging-market GDP growth and urbanization sustain base-metal demand for infrastructure.

- copper & lithium structural demand rising (6–20% CAGRs)

- Zijin targeting >100 kt LCE by 2025

- production scale = valuation catalyst

- EM growth supports base-metal demand

Access to Capital and Credit Markets

Maintaining a strong balance sheet is essential for Zijin to fund its acquisition and expansion strategy; the company generated RMB 72.4 billion operating cash flow in 2024 and carried net debt/EBITDA around 1.9x, supporting deal activity.

Zijin finances global operations via internal cash flow, bank loans and equity placements; in 2024 it arranged $2.1 billion in syndicated loans and raised ~RMB 8.3 billion through equity and convertible instruments.

Global interest rate shifts and tighter credit availability raise borrowing costs and can delay capital-intensive projects—every 100bp rise in rates increases annual interest expense materially given Zijin’s ~RMB 90 billion total borrowings by 2024.

By end-2025 Zijin targets high credit ratings to secure competitive access to international capital markets, aiming to keep net debt/EBITDA under 2.0x and maintain investment-grade equivalent borrowing terms.

- 2024 operating cash flow: RMB 72.4bn

- Net debt/EBITDA ~1.9x (2024)

- Syndicated loans in 2024: $2.1bn; equity raised ~RMB 8.3bn

- Total borrowings ~RMB 90bn (2024); target net debt/EBITDA <2.0x by end-2025

Zijin: Metal-price driven cash flows, deleveraging to <2x and >100kt LCE by 2025

Zijin’s earnings are highly metal-price sensitive (c.80% revenue), with 2024 operating cash flow RMB72.4bn and net debt/EBITDA ~1.9x; 2025 copper ~USD9,000/t and gold ~USD1,900/oz supported revenues while input inflation (+6–12% y/y) raised AISC. The company targets >100kt LCE by 2025, hedges FX/price exposure, arranged $2.1bn loans and RMB8.3bn equity in 2024, and aims net debt/EBITDA <2.0x by end-2025.

| Metric | 2024/2025 |

|---|---|

| Op. cash flow | RMB72.4bn (2024) |

| Net debt/EBITDA | ~1.9x (2024); target <2.0x |

| Copper price | ~USD9,000/t (2025) |

| Gold price | ~USD1,900/oz (2025) |

| Borrowings | ~RMB90bn (2024) |

| Liquidity raises | $2.1bn loans; RMB8.3bn equity (2024) |

| Lithium target | >100kt LCE by 2025 |

Full Version Awaits

Zijin Mining PESTLE Analysis

The preview shown here is the exact Zijin Mining PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Zijin Mining faces regulatory scrutiny, commodity price volatility, and rising ESG expectations that reshape operations and growth opportunities; our concise PESTLE highlights these forces and their strategic implications. Purchase the full PESTLE to access actionable risk assessments, scenario-ready insights, and ready-to-use slides for investors and strategists.

Political factors

Geopolitical Risk and Resource Nationalism

Zijin Mining operates across 20+ countries where political instability and resource nationalism threaten asset security and continuity, notably in parts of Africa and South America.

By end-2025, several host states have proposed higher royalties or compulsory state stakes—estimates suggest potential revenue reallocation of 5–15% for affected projects.

Heightened regulatory scrutiny and renegotiation risks could affect Zijin’s EBITDA margins on exposed assets unless mitigated.

Robust risk mitigation—joint-venture frameworks, political risk insurance, and intensified government engagement—remains critical to preserve long-term operations.

Strategic Alignment with National Interests

Zijin Mining’s strategic alignment with China’s push for critical minerals secures preferential access to state-backed financing—China Development Bank and policy banks supported deals totaling over $5bn for overseas copper and lithium projects in 2023–2025—facilitating major acquisitions and project capex.

Domestic political support reduces funding costs and regulatory friction for expansion, but ties to Beijing increase exposure to sanctions, export controls and scrutiny from the US, EU and Australia that tightened foreign investment reviews in 2024–25.

Geopolitical risks have already delayed or reshaped several deals, forcing Zijin to enhance transparency, local partnerships and ESG compliance to meet host-country requirements and mitigate trade-barrier impacts.

The firm must balance its role as a national champion with global corporate governance norms to sustain access to Western markets and downstream customers amid rising supply-chain security policies.

International Trade Policy and Sanctions

Global trade dynamics and sanctions targeting Chinese firms have strained Zijin Mining's supply chain, with 2024 export controls and tariffs raising compliance costs that risk disrupting shipments of refined copper and gold, which made up over 58% of 2024 metal revenues. The company must track evolving trade agreements and protectionist measures that could limit exports or imports of specialized equipment—affecting capital expenditure that reached US$2.3 billion in 2024. By 2025, regionalized supply chains push Zijin toward localized procurement and sales in Asia-Pacific and Africa to reduce transit risk. Strategic market diversification into Southeast Asia and Europe mitigates localized political friction and preserves access to key smelters and customers.

Host Country Regulatory Stability

Predictability of regimes in Serbia, Colombia and the DRC is critical for Zijin’s capital-intensive projects; political risk flags rose in 2024 with Serbia’s regulatory reviews, Colombia’s 2024 mining tax debates and DRC permitting backlogs delaying projects by months.

Zijin spends tens of millions yearly on government relations and community programs to anticipate policy shifts and protect permits; sudden populist moves have historically prompted mining code revisions and occasional license suspensions.

Zijin maintains formal neutrality while funding local infrastructure—roads, schools, clinics—to reduce social friction and increase government goodwill, a strategy that helped secure extensions or approvals in 2023–2025.

- Key markets: Serbia, Colombia, DRC — high regulatory volatility

- Annual GR/community spend: tens of millions USD

- Delays: permit backlogs causing multi-month project slowdowns

- Strategy: neutrality + local infrastructure to secure legal operating rights

Global Security and Conflict Zones

Operating in conflict-prone regions forces Zijin to deploy advanced security measures and pay rising insurance premiums—global political risk insurance rates rose ~18% in 2024–25—raising per-project up-front security costs by an estimated 5–12% in frontier markets.

Zijin faces ethical/logistical pressures to align operations with UN Guiding Principles on Business and Human Rights while managing evacuations, contractor vetting, and protective infrastructure to limit workforce exposure.

Robust crisis management, local community integration and grievance mechanisms have reduced stoppage days by up to 30% at some high-risk sites; failure increases capital-at-risk and operational disruption probabilities.

- 2024–25 security/insurance hike ~18%

- Per-project security cost rise 5–12%

- Stoppage days cut up to 30% with strong community programs

Zijin faces rising resource-nationalism, higher PRI and multi-month permit delays

Zijin faces heightened resource-nationalism and export controls that risk reallocating 5–15% of project revenues and raised political risk insurance ~18% in 2024–25, increasing per-project security costs 5–12%; state-backed Chinese financing (>$5bn 2023–25) lowers funding costs but raises Western scrutiny; key markets Serbia, Colombia, DRC show high regulatory volatility and permit backlogs causing multi-month delays; mitigation: JVs, PRI, local infrastructure spending (tens of millions USD/yr).

| Metric | Value |

|---|---|

| Revenue reallocation risk | 5–15% |

| PRI rate change 2024–25 | +~18% |

| Per-project security cost rise | 5–12% |

| China-backed financing 2023–25 | >$5bn |

| Annual GR/community spend | Tens of millions USD |

What is included in the product

Explores how macro-environmental factors uniquely affect Zijin Mining across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Concise PESTLE summary of Zijin Mining that’s visually segmented for quick meetings, easily drop‑in to slides or reports, editable for regional/context notes, and structured to aid rapid risk assessment and cross‑team alignment.

Economic factors

Commodity Price Volatility

The financials of Zijin Mining are highly sensitive to gold, copper and zinc prices, with metals accounting for over 80% of revenue; copper demand remained robust through late 2025 amid the energy transition, supporting average LME copper prices near USD 9,000/ton in 2025, while gold averaged about USD 1,900/oz as an inflation hedge. Price swings drove EBIT volatility—Zijin reported 2024 attributable profit down 12% YoY—requiring disciplined cost control. The company employs strategic hedging and a diversified portfolio across China, Kyrgyzstan and Serbia to stabilize cash flows, with hedges covering a portion of production and lowering realized price exposure.

Global Inflation and Operating Costs

Persistent inflation in 2024–25 pushed energy, labor and input costs up 6–12% y/y in major mining regions, raising Zijin’s unit cash costs and squeezing margins.

Zijin must optimize supply chains and efficiency—targeting lower AISC—to retain low-cost producer status amid cost inflation and weaker ore grades.

Higher global real rates have raised cost of capital, slowing new mine capex decisions and prioritizing projects with IRRs above rising hurdles.

Focusing on high-grade assets and automation (e.g., mill upgrades, remote operations) aims to offset inflationary erosion and protect margins.

Currency Exchange Rate Fluctuations

With operations across China, Africa, Asia-Pacific and Central Asia, Zijin faces currency risk across CNY, USD and multiple local currencies; in 2024 foreign exchange losses contributed to a RMB 1.2 billion swing in net profit for Chinese miners industry-wide. Exchange-rate moves alter the RMB value of overseas assets and increase USD-denominated debt servicing costs, especially after 2023–24 USD strength. Zijin uses forwards, cross-currency swaps and natural hedges—matching revenue/cost currencies—to mitigate volatility. A stronger yuan or weaker host-country currencies compresses consolidated revenue and reported profitability on RMB financial statements.

Demand Driven by the Green Energy Transition

The global shift to renewables and EVs has driven structural demand for copper and lithium, with copper demand for clean energy estimated to grow 6–8% CAGR to 2030 and lithium demand forecast to rise ~20% CAGR to 2025.

Zijin has expanded its lithium portfolio via acquisitions and JV stakes, targeting >100 kt LCE capacity by 2025 to capture battery supply growth and enhance valuation.

Scaling production by 2025 is a primary driver of Zijin’s market multiple; emerging-market GDP growth and urbanization sustain base-metal demand for infrastructure.

- copper & lithium structural demand rising (6–20% CAGRs)

- Zijin targeting >100 kt LCE by 2025

- production scale = valuation catalyst

- EM growth supports base-metal demand

Access to Capital and Credit Markets

Maintaining a strong balance sheet is essential for Zijin to fund its acquisition and expansion strategy; the company generated RMB 72.4 billion operating cash flow in 2024 and carried net debt/EBITDA around 1.9x, supporting deal activity.

Zijin finances global operations via internal cash flow, bank loans and equity placements; in 2024 it arranged $2.1 billion in syndicated loans and raised ~RMB 8.3 billion through equity and convertible instruments.

Global interest rate shifts and tighter credit availability raise borrowing costs and can delay capital-intensive projects—every 100bp rise in rates increases annual interest expense materially given Zijin’s ~RMB 90 billion total borrowings by 2024.

By end-2025 Zijin targets high credit ratings to secure competitive access to international capital markets, aiming to keep net debt/EBITDA under 2.0x and maintain investment-grade equivalent borrowing terms.

- 2024 operating cash flow: RMB 72.4bn

- Net debt/EBITDA ~1.9x (2024)

- Syndicated loans in 2024: $2.1bn; equity raised ~RMB 8.3bn

- Total borrowings ~RMB 90bn (2024); target net debt/EBITDA <2.0x by end-2025

Zijin: Metal-price driven cash flows, deleveraging to <2x and >100kt LCE by 2025

Zijin’s earnings are highly metal-price sensitive (c.80% revenue), with 2024 operating cash flow RMB72.4bn and net debt/EBITDA ~1.9x; 2025 copper ~USD9,000/t and gold ~USD1,900/oz supported revenues while input inflation (+6–12% y/y) raised AISC. The company targets >100kt LCE by 2025, hedges FX/price exposure, arranged $2.1bn loans and RMB8.3bn equity in 2024, and aims net debt/EBITDA <2.0x by end-2025.

| Metric | 2024/2025 |

|---|---|

| Op. cash flow | RMB72.4bn (2024) |

| Net debt/EBITDA | ~1.9x (2024); target <2.0x |

| Copper price | ~USD9,000/t (2025) |

| Gold price | ~USD1,900/oz (2025) |

| Borrowings | ~RMB90bn (2024) |

| Liquidity raises | $2.1bn loans; RMB8.3bn equity (2024) |

| Lithium target | >100kt LCE by 2025 |

Full Version Awaits

Zijin Mining PESTLE Analysis

The preview shown here is the exact Zijin Mining PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.