Zotefoams PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how political shifts, supply-chain pressures, and sustainability trends are shaping Zotefoams’ competitive position—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Purchase the full PESTLE analysis for a complete, actionable breakdown you can use in investor reports, pitches, or strategic plans—download instantly for immediate insights.

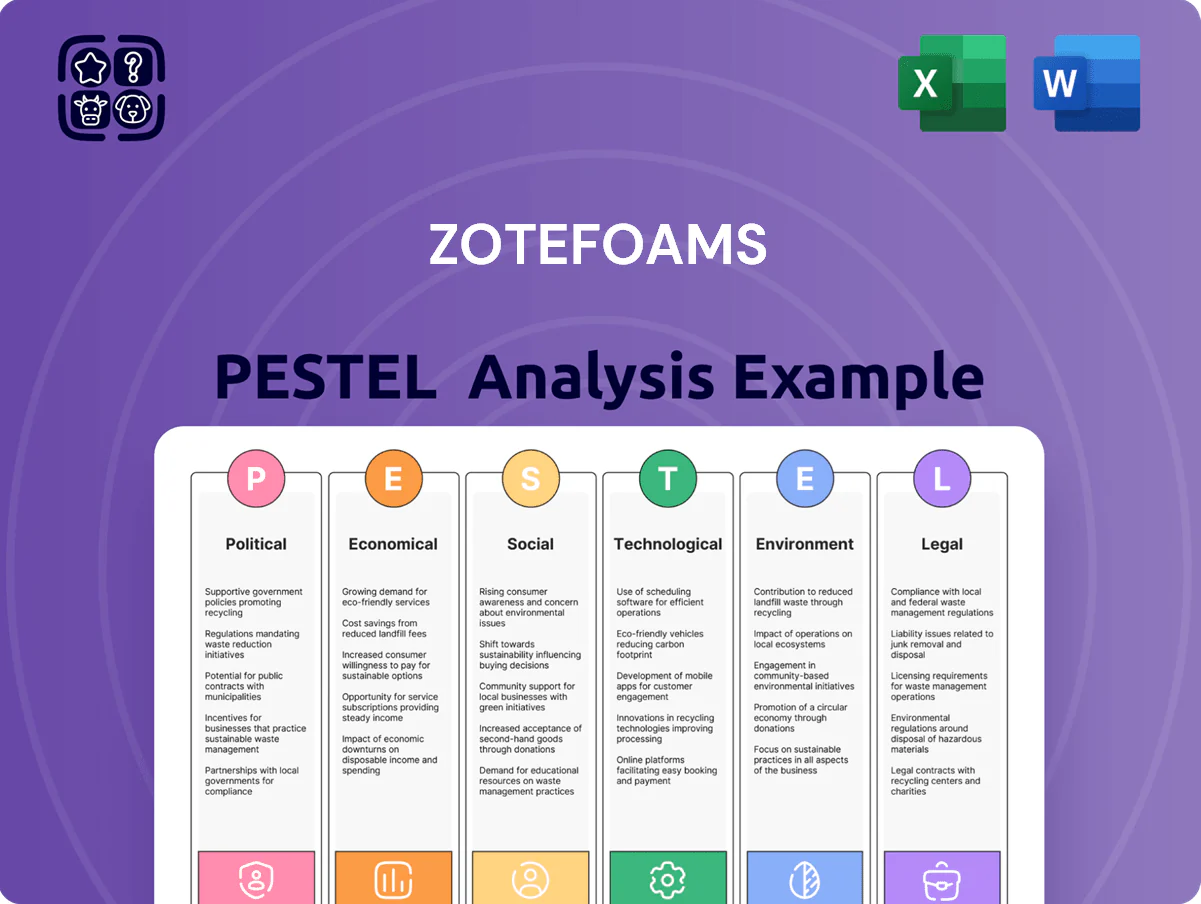

Political factors

Post-Brexit trade and regulatory alignment

Post-Brexit trade relations remained a key risk for Zotefoams through end-2025: UK-EU goods trade fell 1.4% in 2024 and customs frictions increased average transit times by 12% for UK-EU road freight, threatening timely delivery of high-performance foams to aerospace and automotive suppliers.

Government support for sustainable packaging

Political initiatives reducing single-use plastics and promoting circular economy models provide a clear tailwind for Zotefoams ReZorce technology, with EU and national roadmaps targeting 50% recyclable packaging by 2030 and extended producer responsibility expansions. By late 2025 several governments have announced subsidies/tax breaks—e.g., UK £100m+ Green Packaging Fund and EU state-aid windows—favoring monomaterial solutions, aligning with Zotefoams’ recyclability focus and supporting potential revenue uplift.

Global defense and aerospace spending

Geopolitical tensions in late 2025 prompted NATO and allied nations to raise defense budgets, with NATO defense spending hitting an estimated 2.5% of GDP on average and allied procurement increases of roughly $40–60 billion in 2025–2026; this boosts demand for Zotefoams’ lightweight, high-performance foams used in military and commercial aviation.

Industrial strategy for net zero targets

The UK and EU aim for net-zero by 2050/2040 respectively, driving tighter industrial carbon rules; Scope 1–2 reporting and ETS reforms raised compliance costs—UK emissions trading price averaged ~£80/tCO2 in 2024. Zotefoams must decarbonise operations, improve energy efficiency and reporting to retain its social licence and qualify for green finance, where green loan margins can be 10–25bps cheaper.

- Net-zero target: UK 2050, EU 2050/2040 policy debates

- ETS price ~£80/tCO2 (2024)

- Stricter Scope 1–2 reporting and energy audits required

- Green financing can reduce margins by 10–25bps

Geopolitical supply chain security

- 2022–24 logistics cost rise 8–12%

- 56% of advanced economies offered reshoring incentives (OECD, 2024)

- Potential tariff impact on inputs 3–7%

Supply frictions, green packaging & defense spend drive decarbonisation tailwinds

Post-Brexit trade frictions raised UK-EU transit times ~12% and risk timely deliveries; EU/UK packaging targets and subsidies (UK £100m+ Green Packaging Fund) favor Zotefoams ReZorce; NATO/allied defense spend +$40–60bn (2025–26) boosts aerospace demand; ETS ~£80/tCO2 (2024) and net-zero targets increase decarbonisation and green finance pressure.

| Metric | Value |

|---|---|

| UK-EU transit time rise | ~12% |

| Green Packaging Fund (UK) | £100m+ |

| Defense procurement lift | $40–60bn |

| EU/UK ETS price (2024) | ~£80/tCO2 |

What is included in the product

Explores how macro-environmental factors uniquely impact Zotefoams across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven sub-points and forward-looking insights to support scenario planning and strategy.

A concise, visually segmented PESTLE summary of Zotefoams that’s easy to drop into presentations or share across teams, helping quickly align on external risks and opportunities during strategic planning.

Economic factors

Volatile raw material and polymer pricing

The cost of polyethylene and specialized polymers, closely tied to Brent crude movements, swung by roughly 18% in 2025 as oil averaged about $82/bbl, amplifying input volatility for Zotefoams. Economic instability and supply-chain disruptions forced quarterly feedstock price shifts of up to 12%, prompting the company to adopt flexible customer pricing and short-term hedging. Preserving margins depends on passing costs to end-markets—industrial, automotive, medical—without eroding market share, given FY2024 gross margin of ~31%.

Energy cost volatility in manufacturing

The nitrogen expansion process at Zotefoams is energy-intensive, exposing margins to industrial energy price shifts; UK wholesale gas prices averaged ~42 p/th over 2024, down from 95 p/th in 2022 but still higher than pre-crisis levels.

Energy markets have stabilized vs prior years, yet the transition to renewables by end-2025 poses supply and capex risks for manufacturers reliant on consistent high-temperature heat.

Controlling energy overheads is vital to keep Zotefoams' cellular materials cost-competitive, as energy can represent 15–25% of production costs in polymer foaming processes.

Currency exchange rate fluctuations

As a UK-based firm with ~60% international sales, Zotefoams is exposed to GBP/USD/EUR swings; a 10% sterling appreciation in 2024 would reduce reported overseas revenues by roughly that magnitude in GBP terms, while a 10% depreciation inflates them.

Exchange moves also alter input costs—in 2024 imported raw material spend estimated at ~£40m could vary materially with FX shifts.

Analysts monitor FX and hedging; Zotefoams reported a 2023 FX loss of £1.2m, highlighting short-term earnings sensitivity.

Global interest rate environment

Global interest rates in late 2025 — with 10-year US Treasuries around 4.6% and ECB rates near 3.75% — raise Zotefoams’ weighted average cost of capital for expansions, increasing borrowing costs for new plants and ReZorce R&D.

Higher rates can slow capex, while a stabilizing trend (monthly US CPI easing to ~3.1% in 2025) could prompt more aggressive investment to capture demand.

- 10y US Treasury ~4.6%

- ECB deposit ~3.75%

- 2025 CPI US ~3.1%

Recovery and growth in the aviation sector

The global aerospace industry's recovery is a key driver for Zotefoams' high-margin ZOTEK products; commercial passenger traffic returned to about 90–95% of 2019 levels by end-2025, lifting OEM output to ~1,200–1,400 narrowbody deliveries in 2025 and higher cabin refurbishment demand.

This tailwind supports sustained volume growth in specialized cellular materials, with aerospace-related ZOTEK sales likely growing mid-to-high single digits as airlines invest in cabin retrofits and new fleet deliveries.

- Passenger traffic ~90–95% of 2019 by end-2025

- Narrowbody deliveries ~1,200–1,400 in 2025

- ZOTEK aerospace sales growth: mid-to-high single digits

Macro & energy shocks squeeze margins; aerospace rebound fuels ZOTEK mid–high single‑digit growth

Oil-linked polymer feedstock volatility (±18% in 2025; Brent ~$82/bbl) and energy costs (UK gas ~42 p/th in 2024) pressure margins; FX swings (10% GBP move) and ~£40m imported raw-materials amplify earnings sensitivity (2023 FX loss £1.2m). Higher rates (10y US ~4.6%, ECB ~3.75%) raise WACC and capex costs; aerospace recovery (passenger traffic 90–95% of 2019) supports mid–high single-digit ZOTEK growth.

| Metric | 2024–25 |

|---|---|

| Brent | $82/bbl |

| UK gas | 42 p/th |

| 10y US | 4.6% |

| FX loss (2023) | £1.2m |

Same Document Delivered

Zotefoams PESTLE Analysis

The preview shown here is the exact Zotefoams PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises. This file contains the same content, layout, and insights visible in the preview and will be available for immediate download upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Understand how political shifts, supply-chain pressures, and sustainability trends are shaping Zotefoams’ competitive position—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Purchase the full PESTLE analysis for a complete, actionable breakdown you can use in investor reports, pitches, or strategic plans—download instantly for immediate insights.

Political factors

Post-Brexit trade and regulatory alignment

Post-Brexit trade relations remained a key risk for Zotefoams through end-2025: UK-EU goods trade fell 1.4% in 2024 and customs frictions increased average transit times by 12% for UK-EU road freight, threatening timely delivery of high-performance foams to aerospace and automotive suppliers.

Government support for sustainable packaging

Political initiatives reducing single-use plastics and promoting circular economy models provide a clear tailwind for Zotefoams ReZorce technology, with EU and national roadmaps targeting 50% recyclable packaging by 2030 and extended producer responsibility expansions. By late 2025 several governments have announced subsidies/tax breaks—e.g., UK £100m+ Green Packaging Fund and EU state-aid windows—favoring monomaterial solutions, aligning with Zotefoams’ recyclability focus and supporting potential revenue uplift.

Global defense and aerospace spending

Geopolitical tensions in late 2025 prompted NATO and allied nations to raise defense budgets, with NATO defense spending hitting an estimated 2.5% of GDP on average and allied procurement increases of roughly $40–60 billion in 2025–2026; this boosts demand for Zotefoams’ lightweight, high-performance foams used in military and commercial aviation.

Industrial strategy for net zero targets

The UK and EU aim for net-zero by 2050/2040 respectively, driving tighter industrial carbon rules; Scope 1–2 reporting and ETS reforms raised compliance costs—UK emissions trading price averaged ~£80/tCO2 in 2024. Zotefoams must decarbonise operations, improve energy efficiency and reporting to retain its social licence and qualify for green finance, where green loan margins can be 10–25bps cheaper.

- Net-zero target: UK 2050, EU 2050/2040 policy debates

- ETS price ~£80/tCO2 (2024)

- Stricter Scope 1–2 reporting and energy audits required

- Green financing can reduce margins by 10–25bps

Geopolitical supply chain security

- 2022–24 logistics cost rise 8–12%

- 56% of advanced economies offered reshoring incentives (OECD, 2024)

- Potential tariff impact on inputs 3–7%

Supply frictions, green packaging & defense spend drive decarbonisation tailwinds

Post-Brexit trade frictions raised UK-EU transit times ~12% and risk timely deliveries; EU/UK packaging targets and subsidies (UK £100m+ Green Packaging Fund) favor Zotefoams ReZorce; NATO/allied defense spend +$40–60bn (2025–26) boosts aerospace demand; ETS ~£80/tCO2 (2024) and net-zero targets increase decarbonisation and green finance pressure.

| Metric | Value |

|---|---|

| UK-EU transit time rise | ~12% |

| Green Packaging Fund (UK) | £100m+ |

| Defense procurement lift | $40–60bn |

| EU/UK ETS price (2024) | ~£80/tCO2 |

What is included in the product

Explores how macro-environmental factors uniquely impact Zotefoams across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven sub-points and forward-looking insights to support scenario planning and strategy.

A concise, visually segmented PESTLE summary of Zotefoams that’s easy to drop into presentations or share across teams, helping quickly align on external risks and opportunities during strategic planning.

Economic factors

Volatile raw material and polymer pricing

The cost of polyethylene and specialized polymers, closely tied to Brent crude movements, swung by roughly 18% in 2025 as oil averaged about $82/bbl, amplifying input volatility for Zotefoams. Economic instability and supply-chain disruptions forced quarterly feedstock price shifts of up to 12%, prompting the company to adopt flexible customer pricing and short-term hedging. Preserving margins depends on passing costs to end-markets—industrial, automotive, medical—without eroding market share, given FY2024 gross margin of ~31%.

Energy cost volatility in manufacturing

The nitrogen expansion process at Zotefoams is energy-intensive, exposing margins to industrial energy price shifts; UK wholesale gas prices averaged ~42 p/th over 2024, down from 95 p/th in 2022 but still higher than pre-crisis levels.

Energy markets have stabilized vs prior years, yet the transition to renewables by end-2025 poses supply and capex risks for manufacturers reliant on consistent high-temperature heat.

Controlling energy overheads is vital to keep Zotefoams' cellular materials cost-competitive, as energy can represent 15–25% of production costs in polymer foaming processes.

Currency exchange rate fluctuations

As a UK-based firm with ~60% international sales, Zotefoams is exposed to GBP/USD/EUR swings; a 10% sterling appreciation in 2024 would reduce reported overseas revenues by roughly that magnitude in GBP terms, while a 10% depreciation inflates them.

Exchange moves also alter input costs—in 2024 imported raw material spend estimated at ~£40m could vary materially with FX shifts.

Analysts monitor FX and hedging; Zotefoams reported a 2023 FX loss of £1.2m, highlighting short-term earnings sensitivity.

Global interest rate environment

Global interest rates in late 2025 — with 10-year US Treasuries around 4.6% and ECB rates near 3.75% — raise Zotefoams’ weighted average cost of capital for expansions, increasing borrowing costs for new plants and ReZorce R&D.

Higher rates can slow capex, while a stabilizing trend (monthly US CPI easing to ~3.1% in 2025) could prompt more aggressive investment to capture demand.

- 10y US Treasury ~4.6%

- ECB deposit ~3.75%

- 2025 CPI US ~3.1%

Recovery and growth in the aviation sector

The global aerospace industry's recovery is a key driver for Zotefoams' high-margin ZOTEK products; commercial passenger traffic returned to about 90–95% of 2019 levels by end-2025, lifting OEM output to ~1,200–1,400 narrowbody deliveries in 2025 and higher cabin refurbishment demand.

This tailwind supports sustained volume growth in specialized cellular materials, with aerospace-related ZOTEK sales likely growing mid-to-high single digits as airlines invest in cabin retrofits and new fleet deliveries.

- Passenger traffic ~90–95% of 2019 by end-2025

- Narrowbody deliveries ~1,200–1,400 in 2025

- ZOTEK aerospace sales growth: mid-to-high single digits

Macro & energy shocks squeeze margins; aerospace rebound fuels ZOTEK mid–high single‑digit growth

Oil-linked polymer feedstock volatility (±18% in 2025; Brent ~$82/bbl) and energy costs (UK gas ~42 p/th in 2024) pressure margins; FX swings (10% GBP move) and ~£40m imported raw-materials amplify earnings sensitivity (2023 FX loss £1.2m). Higher rates (10y US ~4.6%, ECB ~3.75%) raise WACC and capex costs; aerospace recovery (passenger traffic 90–95% of 2019) supports mid–high single-digit ZOTEK growth.

| Metric | 2024–25 |

|---|---|

| Brent | $82/bbl |

| UK gas | 42 p/th |

| 10y US | 4.6% |

| FX loss (2023) | £1.2m |

Same Document Delivered

Zotefoams PESTLE Analysis

The preview shown here is the exact Zotefoams PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises. This file contains the same content, layout, and insights visible in the preview and will be available for immediate download upon checkout.