ZTO Express Porter's Five Forces Analysis

From Overview to Strategy Blueprint

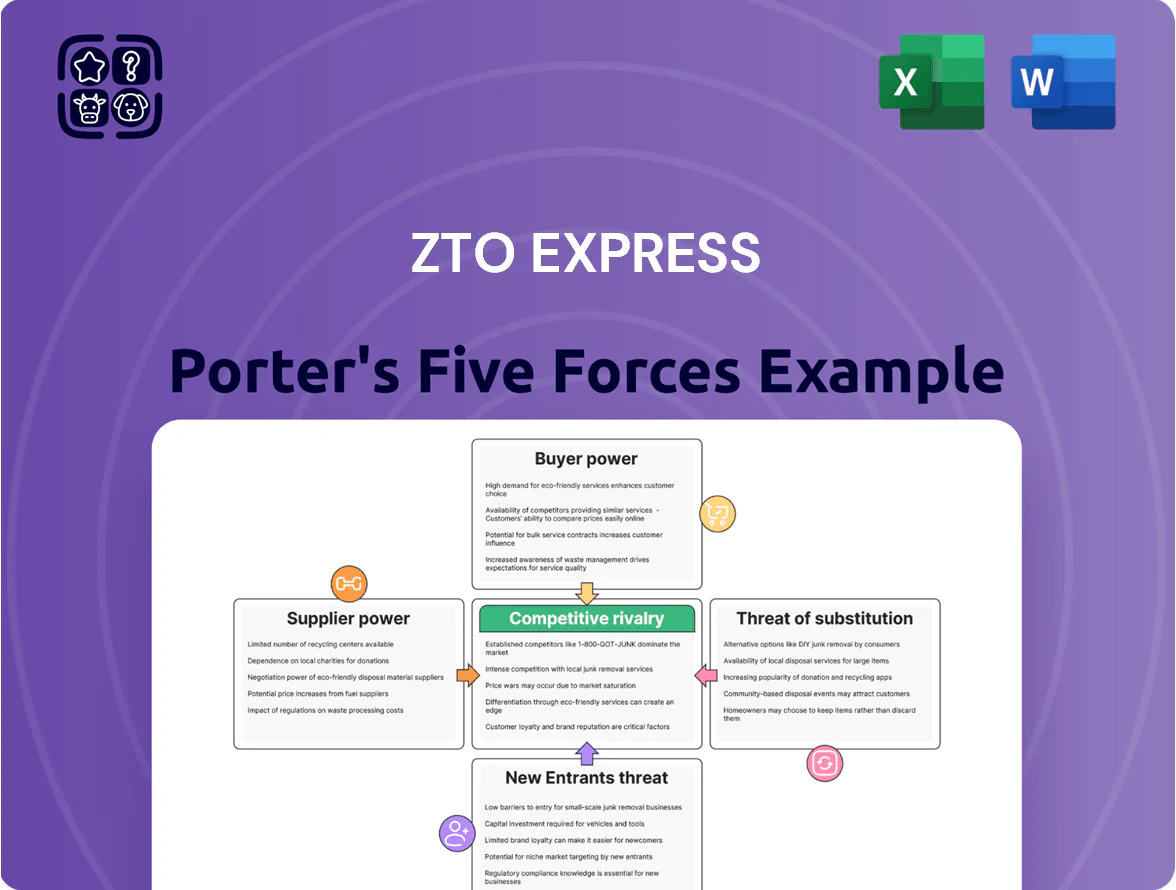

ZTO Express faces intense rivalry from domestic and international parcel carriers, moderate supplier leverage due to fuel and tech vendors, rising buyer expectations for speed and price, growing threat from digital substitutes and logistics platforms, and significant barriers for new entrants driven by scale and network effects—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ZTO Express’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and Energy Provider Influence

Dependence on Vehicle Manufacturers

ZTO depends on a few heavy‑duty truck makers and electric van suppliers to run its ~150,000‑vehicle fleet, so supplier concentration raises bargaining power despite ZTO’s large orders. ZTO’s 2024 procurement volumes—estimated at >10,000 vehicles annually—deliver price leverage, but specialized high‑capacity models limit vendor options. Tightened China emissions and NEV (new energy vehicle) rules by late 2025 will boost demand for compliant vehicles, giving manufacturers extra pricing leverage.

Labor Market Dynamics and Courier Costs

Real Estate and Warehousing Constraints

Securing land for sorting centers needs close deals with local governments and developers; in 2024 China saw industrial land availability drop by ~8% in Tier 1/2 metros, boosting landlords’ leverage over lease length and rent escalations.

ZTO offsets this by buying land-use rights for strategic hubs—owning ~12% more logistic land rights in 2023 vs 2021—reducing reliance on third-party owners and stabilizing operating costs.

- Tier 1/2 industrial land down ~8% (2024)

- Landlord/local authority pricing power high

- ZTO increased land-use rights ~12% (2021–2023)

Technology and Automation Vendors

The integration of automated sorting systems and AI logistics software is central to ZTO Express’s cost-leadership; automation cut per-parcel handling costs by an estimated 10–15% in China logistics pilots in 2024.

Multiple vendors exist, but proprietary hardware/software creates high switching costs and supplier lock-in for critical ecosystems.

ZTO builds in-house platforms to reduce dependence but still buys specialized high-tech sorters from a few manufacturers.

- Automation drives 10–15% per-parcel cost savings (2024 pilots)

- Few specialist sorter makers => concentrated supplier power

- High switching costs from proprietary ecosystems

- In-house tech reduces but does not eliminate supplier reliance

ZTO offsets supplier power with hedges, land buys, bulk fleet and 10–15% automation savings

| Factor | Key metric |

|---|---|

| Fuel | 40% diesel hedged |

| Fleet purchasing | >10,000 vehicles/yr |

| Land rights | +12% (2021–23) |

| Automation | 10–15% cost cut |

What is included in the product

Provides a concise Porter's Five Forces assessment of ZTO Express, highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and pinpointing strategic vulnerabilities and defensive advantages in the express logistics market.

A concise Porter's Five Forces snapshot for ZTO Express—quickly identify competitive pressures and strategic levers to relieve margin squeeze and route-to-market bottlenecks.

Customers Bargaining Power

Dominance of Major E-commerce Platforms

A substantial share of ZTO Express volume comes from Alibaba, Pinduoduo and Douyin, which together accounted for roughly 46% of ZTO’s e-commerce parcel volume in 2025, giving them strong bargaining power.

These platforms can push lower delivery prices by routing merchant orders to favored logistics partners or bundled services, squeezing ZTO’s unit economics and forcing promotional pricing.

By late 2025 channel diversification trimmed single-platform dependence—ZTO’s top-customer concentration fell from 52% in 2022 to ~38%—but the aggregated leverage of the giants still keeps margin pressure high.

Low Switching Costs for Individual Merchants

Small and medium merchants can switch among ZTO Express, YTO Express, and STO Express largely on price and service; surveys in 2024 showed ~68% of SME shippers prioritized cost, underscoring low switching costs.

Delivery is viewed as a commodity, so price sensitivity is high; ZTO’s 2024 gross margin for express segment fell to ~9.8%, reflecting pressure to compete on price.

ZTO must prove better reliability and speed—in 2024 its on-time rate was 92.1%—to retain merchants without starting destructive price wars.

End-Consumer Expectations for Service Quality

End-consumer satisfaction largely shapes ZTO Express’s long-term revenue despite merchants paying shipping; in 2024 surveys 68% of Chinese online shoppers said real-time tracking and flexible windows influence carrier choice, so ZTO must invest in GPS-enabled tracking, same-day slots, and streamlined returns—ZTO reported 2024 capex for IT and last-mile upgrades rose ~22% y/y—to avoid losing merchants after consumers demand alternatives for poor handling.

Volume Discounts for Corporate Clients

Large corporate shippers wield strong bargaining power at ZTO Express because their volumes—often millions of parcels monthly—justify steep volume discounts and bespoke logistics, pressuring margins; China e-commerce B2C parcel giants accounted for over 60% of industry volume in 2024, amplifying this effect.

ZTO’s scale (handled ~12.3 billion parcels in 2024) lets it absorb customization costs better than smaller rivals, yet pricing pressure persists as top 10 corporate clients can negotiate double-digit discounts.

- High-volume leverage: millions/month per client

- ZTO scale: ~12.3 billion parcels handled in 2024

- Top clients: often demand customized logistics

- Discounts: commonly double-digit, squeeze margins

- Smaller rivals: less able to match service+price

Transparency and Price Comparison Tools

Digital logistics aggregators and price-comparison tools let customers view real-time shipping rates across carriers, keeping ZTO Express from raising prices without adding clear value.

By 2025 the Chinese express market shows >80% digital quote transparency; shippers use this to pit carriers against each other and pressure margins.

For ZTO, transparency means price elasticity rises and negotiating leverage shifts to volume-sensitive clients, squeezing average yield per parcel.

- Real-time quotes reduce price opacity

- 2025 market: >80% digital price visibility

- Clients use comparisons to demand lower rates

- Pressure on ZTO yields and margin per parcel

ZTO margins squeezed as top platforms (46%) and price‑sensitive SMEs drive deep discounts

Customers—especially Alibaba, Pinduoduo, Douyin—hold strong bargaining power (≈46% of ZTO e‑commerce volume in 2025), forcing price pressure and double‑digit discounts for top clients; SME shippers (68% cost‑sensitive in 2024) switch on price, while digital quote transparency (>80% in 2025) raises elasticity, keeping ZTO’s 2024 express gross margin near 9.8% under pressure.

| Metric | Value |

|---|---|

| Top-platform share (2025) | ≈46% |

| ZTO parcels (2024) | ≈12.3bn |

| Express gross margin (2024) | ≈9.8% |

| SME cost focus (2024) | 68% |

| Price transparency (2025) | >80% |

Preview the Actual Deliverable

ZTO Express Porter's Five Forces Analysis

This preview shows the exact ZTO Express Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

ZTO Express faces intense rivalry from domestic and international parcel carriers, moderate supplier leverage due to fuel and tech vendors, rising buyer expectations for speed and price, growing threat from digital substitutes and logistics platforms, and significant barriers for new entrants driven by scale and network effects—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ZTO Express’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and Energy Provider Influence

Dependence on Vehicle Manufacturers

ZTO depends on a few heavy‑duty truck makers and electric van suppliers to run its ~150,000‑vehicle fleet, so supplier concentration raises bargaining power despite ZTO’s large orders. ZTO’s 2024 procurement volumes—estimated at >10,000 vehicles annually—deliver price leverage, but specialized high‑capacity models limit vendor options. Tightened China emissions and NEV (new energy vehicle) rules by late 2025 will boost demand for compliant vehicles, giving manufacturers extra pricing leverage.

Labor Market Dynamics and Courier Costs

Real Estate and Warehousing Constraints

Securing land for sorting centers needs close deals with local governments and developers; in 2024 China saw industrial land availability drop by ~8% in Tier 1/2 metros, boosting landlords’ leverage over lease length and rent escalations.

ZTO offsets this by buying land-use rights for strategic hubs—owning ~12% more logistic land rights in 2023 vs 2021—reducing reliance on third-party owners and stabilizing operating costs.

- Tier 1/2 industrial land down ~8% (2024)

- Landlord/local authority pricing power high

- ZTO increased land-use rights ~12% (2021–2023)

Technology and Automation Vendors

The integration of automated sorting systems and AI logistics software is central to ZTO Express’s cost-leadership; automation cut per-parcel handling costs by an estimated 10–15% in China logistics pilots in 2024.

Multiple vendors exist, but proprietary hardware/software creates high switching costs and supplier lock-in for critical ecosystems.

ZTO builds in-house platforms to reduce dependence but still buys specialized high-tech sorters from a few manufacturers.

- Automation drives 10–15% per-parcel cost savings (2024 pilots)

- Few specialist sorter makers => concentrated supplier power

- High switching costs from proprietary ecosystems

- In-house tech reduces but does not eliminate supplier reliance

ZTO offsets supplier power with hedges, land buys, bulk fleet and 10–15% automation savings

| Factor | Key metric |

|---|---|

| Fuel | 40% diesel hedged |

| Fleet purchasing | >10,000 vehicles/yr |

| Land rights | +12% (2021–23) |

| Automation | 10–15% cost cut |

What is included in the product

Provides a concise Porter's Five Forces assessment of ZTO Express, highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and pinpointing strategic vulnerabilities and defensive advantages in the express logistics market.

A concise Porter's Five Forces snapshot for ZTO Express—quickly identify competitive pressures and strategic levers to relieve margin squeeze and route-to-market bottlenecks.

Customers Bargaining Power

Dominance of Major E-commerce Platforms

A substantial share of ZTO Express volume comes from Alibaba, Pinduoduo and Douyin, which together accounted for roughly 46% of ZTO’s e-commerce parcel volume in 2025, giving them strong bargaining power.

These platforms can push lower delivery prices by routing merchant orders to favored logistics partners or bundled services, squeezing ZTO’s unit economics and forcing promotional pricing.

By late 2025 channel diversification trimmed single-platform dependence—ZTO’s top-customer concentration fell from 52% in 2022 to ~38%—but the aggregated leverage of the giants still keeps margin pressure high.

Low Switching Costs for Individual Merchants

Small and medium merchants can switch among ZTO Express, YTO Express, and STO Express largely on price and service; surveys in 2024 showed ~68% of SME shippers prioritized cost, underscoring low switching costs.

Delivery is viewed as a commodity, so price sensitivity is high; ZTO’s 2024 gross margin for express segment fell to ~9.8%, reflecting pressure to compete on price.

ZTO must prove better reliability and speed—in 2024 its on-time rate was 92.1%—to retain merchants without starting destructive price wars.

End-Consumer Expectations for Service Quality

End-consumer satisfaction largely shapes ZTO Express’s long-term revenue despite merchants paying shipping; in 2024 surveys 68% of Chinese online shoppers said real-time tracking and flexible windows influence carrier choice, so ZTO must invest in GPS-enabled tracking, same-day slots, and streamlined returns—ZTO reported 2024 capex for IT and last-mile upgrades rose ~22% y/y—to avoid losing merchants after consumers demand alternatives for poor handling.

Volume Discounts for Corporate Clients

Large corporate shippers wield strong bargaining power at ZTO Express because their volumes—often millions of parcels monthly—justify steep volume discounts and bespoke logistics, pressuring margins; China e-commerce B2C parcel giants accounted for over 60% of industry volume in 2024, amplifying this effect.

ZTO’s scale (handled ~12.3 billion parcels in 2024) lets it absorb customization costs better than smaller rivals, yet pricing pressure persists as top 10 corporate clients can negotiate double-digit discounts.

- High-volume leverage: millions/month per client

- ZTO scale: ~12.3 billion parcels handled in 2024

- Top clients: often demand customized logistics

- Discounts: commonly double-digit, squeeze margins

- Smaller rivals: less able to match service+price

Transparency and Price Comparison Tools

Digital logistics aggregators and price-comparison tools let customers view real-time shipping rates across carriers, keeping ZTO Express from raising prices without adding clear value.

By 2025 the Chinese express market shows >80% digital quote transparency; shippers use this to pit carriers against each other and pressure margins.

For ZTO, transparency means price elasticity rises and negotiating leverage shifts to volume-sensitive clients, squeezing average yield per parcel.

- Real-time quotes reduce price opacity

- 2025 market: >80% digital price visibility

- Clients use comparisons to demand lower rates

- Pressure on ZTO yields and margin per parcel

ZTO margins squeezed as top platforms (46%) and price‑sensitive SMEs drive deep discounts

Customers—especially Alibaba, Pinduoduo, Douyin—hold strong bargaining power (≈46% of ZTO e‑commerce volume in 2025), forcing price pressure and double‑digit discounts for top clients; SME shippers (68% cost‑sensitive in 2024) switch on price, while digital quote transparency (>80% in 2025) raises elasticity, keeping ZTO’s 2024 express gross margin near 9.8% under pressure.

| Metric | Value |

|---|---|

| Top-platform share (2025) | ≈46% |

| ZTO parcels (2024) | ≈12.3bn |

| Express gross margin (2024) | ≈9.8% |

| SME cost focus (2024) | 68% |

| Price transparency (2025) | >80% |

Preview the Actual Deliverable

ZTO Express Porter's Five Forces Analysis

This preview shows the exact ZTO Express Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.