Zhongyuan Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Zhongyuan Bank navigates a competitive landscape shaped by intense rivalry and evolving customer demands. Understanding the power of suppliers and the threat of new entrants is crucial for its sustained growth.

The complete report reveals the real forces shaping Zhongyuan Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on Core Deposits

Zhongyuan Bank's reliance on core deposits means suppliers, primarily depositors, hold significant bargaining power. Large corporate and institutional depositors, in particular, can leverage their funds to demand better interest rates or move to alternative investments, especially when market rates are low. This is a crucial factor, as evidenced by the slowing growth of customer deposits across the Chinese banking sector in recent periods.

Technology and Infrastructure Providers

Zhongyuan Bank's digital transformation amplifies its dependence on technology and infrastructure providers, especially for advanced AI and data analytics. Suppliers offering innovative and secure banking tech solutions can wield considerable influence due to the specialized nature and high costs of switching these critical systems.

Banks are actively investing in AI to revolutionize their operations and speed up product development, aiming to boost technological capabilities. For instance, global spending on AI in financial services was projected to reach $12.7 billion in 2024, highlighting the sector's commitment to these technologies and the resulting supplier leverage.

Human Capital and Specialized Talent

The banking industry's rapid digital evolution and increasing reliance on artificial intelligence are creating a significant demand for specialized skills in areas like fintech, data analytics, and cybersecurity. This scarcity of qualified professionals directly enhances the bargaining power of employees. For instance, a 2024 survey indicated that the average salary for a cybersecurity analyst in the financial sector saw a 12% increase year-over-year, reflecting this talent gap.

As banks like Zhongyuan Bank navigate this landscape, the competition for top-tier talent intensifies. Employees possessing these in-demand skills can command higher compensation packages and better benefits, directly impacting labor costs. By 2025, a substantial portion of bank executives, reportedly over 70%, identified revamping talent acquisition and retention strategies for an AI-driven future as a top strategic priority to mitigate this supplier power.

Interbank Market and Funding Sources

Beyond customer deposits, Zhongyuan Bank, like many regional institutions, relies significantly on the interbank market for funding. This reliance means that the bargaining power of suppliers in this context is largely dictated by the stability and liquidity of the broader financial system. During periods of market stress, or when regulatory changes impact liquidity, larger financial institutions or central banks can exert considerable influence over funding costs and availability for smaller banks.

For instance, in 2024, while interbank lending rates generally remained subdued, specific market events or shifts in monetary policy could quickly alter this dynamic. Smaller banks, including Zhongyuan Bank, have historically leveraged these lower interbank rates to manage their liquidity needs, but this also exposes them to the potential for increased supplier power when conditions tighten.

- Interbank Market Reliance: Zhongyuan Bank depends on interbank funding, making it susceptible to supplier power.

- Market Volatility Impact: Periods of market stress can empower large institutions and central banks to dictate funding terms.

- Regulatory Influence: Changes in financial regulations can also shift bargaining power in the interbank market.

- Funding Cost Sensitivity: Lower interbank rates in 2024 offered a benefit, but this can reverse, increasing supplier leverage.

Regulatory Compliance and Consulting Services

The increasingly complex and demanding regulatory landscape in China, particularly concerning financial stability initiatives, directly fuels the demand for specialized compliance and consulting services. This heightened need grants significant leverage to firms possessing in-depth knowledge of Chinese banking regulations, such as those issued by the National Financial Regulatory Administration (NFRA) and the People's Bank of China (PBOC).

Chinese regulators have made financial stability a paramount objective, continuously refining the nation's financial regulatory framework. This ongoing evolution means that banks like Zhongyuan Bank must invest more in ensuring adherence to these evolving rules, thereby strengthening the bargaining position of expert service providers.

- Increased Demand for Expertise: As of late 2024, regulatory scrutiny on financial institutions in China has intensified, leading to a greater reliance on external consultants for navigating new directives and ensuring compliance.

- Higher Consulting Fees: The specialized nature of this expertise, coupled with the critical need for accurate regulatory interpretation, allows these consulting firms to command higher fees.

- Supplier Concentration: While numerous consulting firms exist, those with proven track records in Chinese financial regulation are fewer, concentrating bargaining power among a select group.

Key Suppliers Hold Sway Over Zhongyuan Bank

Suppliers to Zhongyuan Bank, particularly depositors and technology providers, hold considerable bargaining power. Depositors, especially large ones, can negotiate better rates, while specialized tech firms offering AI and data analytics solutions benefit from high switching costs and the critical nature of their services. This dynamic is underscored by the projected $12.7 billion global spend on AI in financial services for 2024, highlighting the sector's dependence on these advanced solutions.

The bank's reliance on the interbank market for funding also exposes it to supplier power, influenced by market stability and central bank policies. In 2024, while interbank rates were generally low, shifts in monetary policy or market stress could quickly empower larger institutions to dictate funding terms, increasing Zhongyuan Bank's borrowing costs.

Furthermore, the increasing complexity of Chinese financial regulations, such as those from the NFRA and PBOC, has amplified the bargaining power of specialized compliance consulting firms. As of late 2024, the intensified regulatory scrutiny means banks must invest more in compliance, driving up demand and fees for expert advice.

| Supplier Category | Key Bargaining Power Factors | Impact on Zhongyuan Bank | Illustrative Data Point (2024) |

| Depositors (Retail & Corporate) | Ability to switch for higher rates; concentration of large deposits | Potential for increased funding costs; need to offer competitive deposit rates | Slowing growth in customer deposits across Chinese banks |

| Technology Providers (AI, Data Analytics) | Specialized, high-cost solutions; critical infrastructure dependence | Leverage in pricing and contract terms; risk of system lock-in | Projected $12.7 billion global AI spend in financial services |

| Interbank Market Lenders | Liquidity availability; influence of monetary policy and market stability | Fluctuating funding costs; vulnerability to market shocks | Historically low interbank rates, but subject to policy shifts |

| Compliance Consultants | Expertise in evolving regulations; scarcity of specialized knowledge | Higher fees for essential regulatory adherence; need for strategic partnerships | Increased regulatory scrutiny on Chinese financial institutions |

What is included in the product

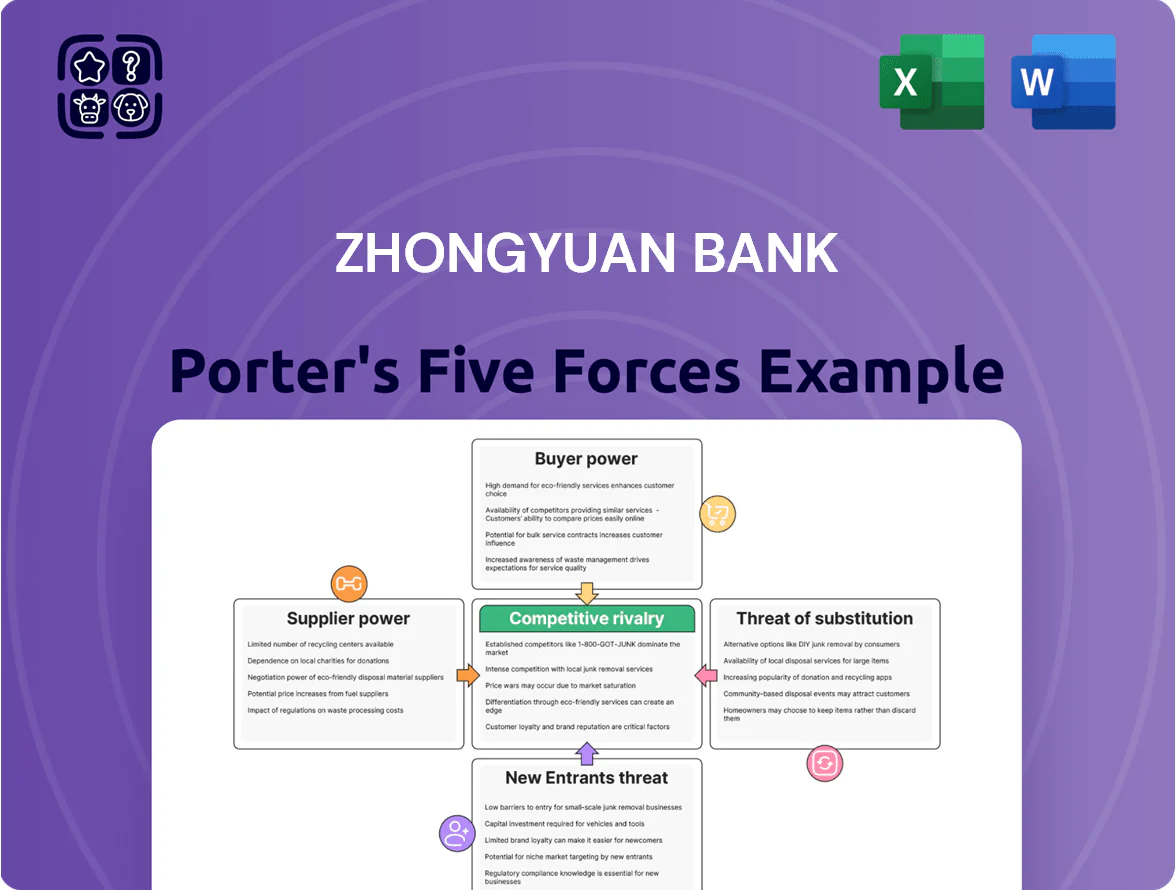

This analysis provides a comprehensive examination of the competitive forces impacting Zhongyuan Bank, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry among existing competitors.

Instantly identify and address competitive threats with a visual breakdown of Zhongyuan Bank's industry landscape.

Customers Bargaining Power

Abundance of Banking Options

Customers in Henan province and throughout China benefit from a vast selection of banking institutions. This includes major state-owned banks, national joint-stock banks, and numerous regional city and rural commercial banks, all providing comparable core financial products. This extensive choice empowers customers, allowing them to readily switch to institutions offering more favorable terms or superior services.

The banking sector's current landscape, characterized by subdued growth and lower interest rates, intensifies the pressure on banks to attract and retain their customer base. In 2023, the average net interest margin for Chinese banks saw a slight decline, underscoring the competitive environment and the critical need for customer loyalty initiatives.

Low Switching Costs for Basic Services

For basic banking services like deposits, loans, and payments, customers face minimal costs when switching banks. This is particularly true as digital banking becomes more prevalent, making it easier than ever to move accounts. This low switching cost empowers customers to actively seek out better deals, pushing banks to offer more competitive interest rates and lower fees. In 2024, the trend of improving digital platforms continues, further reducing friction for customers.

Increased Digital Sophistication and Information Access

Customers are increasingly savvy thanks to digital banking. They can easily compare rates and services from various banks, including Zhongyuan Bank, right from their devices. This ease of access to information means customers have more leverage to demand better terms and conditions.

In 2024, a significant majority of users demonstrated this digital trust. A survey revealed that over 97% of individual customers and a remarkable 99% of small and medium-sized enterprises (SMEs) reported high satisfaction with the security of digital banking platforms. This widespread confidence in digital channels further amplifies customer bargaining power by making it simpler to switch providers for more favorable deals.

Price Sensitivity in a Low Interest Rate Environment

In a persistently low interest rate environment, customers, especially those with significant deposits or corporate accounts, become acutely aware of interest rate differentials. This heightened price sensitivity compels banks like Zhongyuan Bank to engage in more aggressive pricing strategies for both loans and deposits. The competitive pressure on net interest margins is substantial.

This dynamic directly amplifies the bargaining power of customers. When interest rates are low, even small differences in rates offered by competing financial institutions can lead to significant shifts in customer behavior. For instance, the average net interest margin (NIM) for listed banks in China saw a decline to 1.52% in 2024, a decrease of 17 basis points year-over-year, illustrating this margin compression.

- Heightened Price Sensitivity: Customers closely monitor deposit and loan rates in a low-rate climate.

- Margin Pressure: Banks face reduced net interest margins, forcing competitive pricing.

- Customer Empowerment: Aggressive pricing strategies are necessary to retain and attract customers.

- NIM Decline: China's listed banks averaged a 1.52% NIM in 2024, down 17 basis points from 2023.

Demand for Tailored and Inclusive Financial Products

Customers are increasingly demanding financial products that cater to specific needs, such as green finance, inclusive finance, and robust pension services. This growing desire for personalization empowers customers, as they can actively seek out financial institutions that offer these tailored solutions, putting pressure on banks to adapt their product lines.

The National Financial Regulatory Administration (NFRA) reinforced this trend in May 2024 by issuing guidance on 'Five Priorities,' explicitly highlighting the importance of inclusive finance and pension finance. This strategic directive signals a regulatory push towards greater customer-centricity in banking services.

- Growing demand for personalized financial products

- Focus on green, inclusive, and pension finance

- NFRA guidance emphasizes inclusive and pension finance (May 2024)

- Customers can leverage demand to seek specialized services

Banking Customers Gain Leverage Amidst Digital Trust and Margin Squeeze

The bargaining power of customers for Zhongyuan Bank is significant due to the highly competitive banking landscape in China, where numerous institutions offer similar products. This abundance of choice, coupled with low switching costs, particularly with the rise of digital banking, allows customers to easily move their accounts to institutions providing better rates or services. In 2024, customer trust in digital platforms remained exceptionally high, with over 97% of individual users and 99% of SMEs reporting satisfaction with security, further simplifying the process of switching for more favorable terms.

Customers are increasingly price-sensitive, especially in a low-interest-rate environment. This sensitivity is evident in the declining net interest margins for Chinese banks; for instance, listed banks in China averaged a 1.52% NIM in 2024, a decrease of 17 basis points year-over-year. This margin compression compels banks like Zhongyuan Bank to offer more competitive pricing on both loans and deposits to attract and retain business, directly enhancing customer leverage.

Furthermore, customer demand for personalized financial products, such as green, inclusive, and pension finance, is growing. The National Financial Regulatory Administration's guidance in May 2024 emphasizing inclusive and pension finance highlights this trend. Customers can leverage this demand to seek out specialized services, pressuring banks to adapt their offerings and increasing customer influence.

| Metric | 2023 Value | 2024 Value | Change | Impact on Bargaining Power |

|---|---|---|---|---|

| Average Net Interest Margin (China Listed Banks) | ~1.69% | 1.52% | -17 bps | Increases customer power due to margin pressure and need for competitive pricing. |

| Digital Banking Security Satisfaction (Individual Users) | High | >97% | N/A | Facilitates switching, increasing customer leverage. |

| Digital Banking Security Satisfaction (SMEs) | High | >99% | N/A | Facilitates switching, increasing customer leverage. |

Full Version Awaits

Zhongyuan Bank Porter's Five Forces Analysis

This preview showcases the complete Zhongyuan Bank Porter's Five Forces Analysis, detailing the competitive landscape and strategic implications for the institution. The document you see here is the exact, professionally formatted analysis you will receive immediately after purchase, offering actionable insights without any placeholders or alterations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Zhongyuan Bank navigates a competitive landscape shaped by intense rivalry and evolving customer demands. Understanding the power of suppliers and the threat of new entrants is crucial for its sustained growth.

The complete report reveals the real forces shaping Zhongyuan Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on Core Deposits

Zhongyuan Bank's reliance on core deposits means suppliers, primarily depositors, hold significant bargaining power. Large corporate and institutional depositors, in particular, can leverage their funds to demand better interest rates or move to alternative investments, especially when market rates are low. This is a crucial factor, as evidenced by the slowing growth of customer deposits across the Chinese banking sector in recent periods.

Technology and Infrastructure Providers

Zhongyuan Bank's digital transformation amplifies its dependence on technology and infrastructure providers, especially for advanced AI and data analytics. Suppliers offering innovative and secure banking tech solutions can wield considerable influence due to the specialized nature and high costs of switching these critical systems.

Banks are actively investing in AI to revolutionize their operations and speed up product development, aiming to boost technological capabilities. For instance, global spending on AI in financial services was projected to reach $12.7 billion in 2024, highlighting the sector's commitment to these technologies and the resulting supplier leverage.

Human Capital and Specialized Talent

The banking industry's rapid digital evolution and increasing reliance on artificial intelligence are creating a significant demand for specialized skills in areas like fintech, data analytics, and cybersecurity. This scarcity of qualified professionals directly enhances the bargaining power of employees. For instance, a 2024 survey indicated that the average salary for a cybersecurity analyst in the financial sector saw a 12% increase year-over-year, reflecting this talent gap.

As banks like Zhongyuan Bank navigate this landscape, the competition for top-tier talent intensifies. Employees possessing these in-demand skills can command higher compensation packages and better benefits, directly impacting labor costs. By 2025, a substantial portion of bank executives, reportedly over 70%, identified revamping talent acquisition and retention strategies for an AI-driven future as a top strategic priority to mitigate this supplier power.

Interbank Market and Funding Sources

Beyond customer deposits, Zhongyuan Bank, like many regional institutions, relies significantly on the interbank market for funding. This reliance means that the bargaining power of suppliers in this context is largely dictated by the stability and liquidity of the broader financial system. During periods of market stress, or when regulatory changes impact liquidity, larger financial institutions or central banks can exert considerable influence over funding costs and availability for smaller banks.

For instance, in 2024, while interbank lending rates generally remained subdued, specific market events or shifts in monetary policy could quickly alter this dynamic. Smaller banks, including Zhongyuan Bank, have historically leveraged these lower interbank rates to manage their liquidity needs, but this also exposes them to the potential for increased supplier power when conditions tighten.

- Interbank Market Reliance: Zhongyuan Bank depends on interbank funding, making it susceptible to supplier power.

- Market Volatility Impact: Periods of market stress can empower large institutions and central banks to dictate funding terms.

- Regulatory Influence: Changes in financial regulations can also shift bargaining power in the interbank market.

- Funding Cost Sensitivity: Lower interbank rates in 2024 offered a benefit, but this can reverse, increasing supplier leverage.

Regulatory Compliance and Consulting Services

The increasingly complex and demanding regulatory landscape in China, particularly concerning financial stability initiatives, directly fuels the demand for specialized compliance and consulting services. This heightened need grants significant leverage to firms possessing in-depth knowledge of Chinese banking regulations, such as those issued by the National Financial Regulatory Administration (NFRA) and the People's Bank of China (PBOC).

Chinese regulators have made financial stability a paramount objective, continuously refining the nation's financial regulatory framework. This ongoing evolution means that banks like Zhongyuan Bank must invest more in ensuring adherence to these evolving rules, thereby strengthening the bargaining position of expert service providers.

- Increased Demand for Expertise: As of late 2024, regulatory scrutiny on financial institutions in China has intensified, leading to a greater reliance on external consultants for navigating new directives and ensuring compliance.

- Higher Consulting Fees: The specialized nature of this expertise, coupled with the critical need for accurate regulatory interpretation, allows these consulting firms to command higher fees.

- Supplier Concentration: While numerous consulting firms exist, those with proven track records in Chinese financial regulation are fewer, concentrating bargaining power among a select group.

Key Suppliers Hold Sway Over Zhongyuan Bank

Suppliers to Zhongyuan Bank, particularly depositors and technology providers, hold considerable bargaining power. Depositors, especially large ones, can negotiate better rates, while specialized tech firms offering AI and data analytics solutions benefit from high switching costs and the critical nature of their services. This dynamic is underscored by the projected $12.7 billion global spend on AI in financial services for 2024, highlighting the sector's dependence on these advanced solutions.

The bank's reliance on the interbank market for funding also exposes it to supplier power, influenced by market stability and central bank policies. In 2024, while interbank rates were generally low, shifts in monetary policy or market stress could quickly empower larger institutions to dictate funding terms, increasing Zhongyuan Bank's borrowing costs.

Furthermore, the increasing complexity of Chinese financial regulations, such as those from the NFRA and PBOC, has amplified the bargaining power of specialized compliance consulting firms. As of late 2024, the intensified regulatory scrutiny means banks must invest more in compliance, driving up demand and fees for expert advice.

| Supplier Category | Key Bargaining Power Factors | Impact on Zhongyuan Bank | Illustrative Data Point (2024) |

| Depositors (Retail & Corporate) | Ability to switch for higher rates; concentration of large deposits | Potential for increased funding costs; need to offer competitive deposit rates | Slowing growth in customer deposits across Chinese banks |

| Technology Providers (AI, Data Analytics) | Specialized, high-cost solutions; critical infrastructure dependence | Leverage in pricing and contract terms; risk of system lock-in | Projected $12.7 billion global AI spend in financial services |

| Interbank Market Lenders | Liquidity availability; influence of monetary policy and market stability | Fluctuating funding costs; vulnerability to market shocks | Historically low interbank rates, but subject to policy shifts |

| Compliance Consultants | Expertise in evolving regulations; scarcity of specialized knowledge | Higher fees for essential regulatory adherence; need for strategic partnerships | Increased regulatory scrutiny on Chinese financial institutions |

What is included in the product

This analysis provides a comprehensive examination of the competitive forces impacting Zhongyuan Bank, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry among existing competitors.

Instantly identify and address competitive threats with a visual breakdown of Zhongyuan Bank's industry landscape.

Customers Bargaining Power

Abundance of Banking Options

Customers in Henan province and throughout China benefit from a vast selection of banking institutions. This includes major state-owned banks, national joint-stock banks, and numerous regional city and rural commercial banks, all providing comparable core financial products. This extensive choice empowers customers, allowing them to readily switch to institutions offering more favorable terms or superior services.

The banking sector's current landscape, characterized by subdued growth and lower interest rates, intensifies the pressure on banks to attract and retain their customer base. In 2023, the average net interest margin for Chinese banks saw a slight decline, underscoring the competitive environment and the critical need for customer loyalty initiatives.

Low Switching Costs for Basic Services

For basic banking services like deposits, loans, and payments, customers face minimal costs when switching banks. This is particularly true as digital banking becomes more prevalent, making it easier than ever to move accounts. This low switching cost empowers customers to actively seek out better deals, pushing banks to offer more competitive interest rates and lower fees. In 2024, the trend of improving digital platforms continues, further reducing friction for customers.

Increased Digital Sophistication and Information Access

Customers are increasingly savvy thanks to digital banking. They can easily compare rates and services from various banks, including Zhongyuan Bank, right from their devices. This ease of access to information means customers have more leverage to demand better terms and conditions.

In 2024, a significant majority of users demonstrated this digital trust. A survey revealed that over 97% of individual customers and a remarkable 99% of small and medium-sized enterprises (SMEs) reported high satisfaction with the security of digital banking platforms. This widespread confidence in digital channels further amplifies customer bargaining power by making it simpler to switch providers for more favorable deals.

Price Sensitivity in a Low Interest Rate Environment

In a persistently low interest rate environment, customers, especially those with significant deposits or corporate accounts, become acutely aware of interest rate differentials. This heightened price sensitivity compels banks like Zhongyuan Bank to engage in more aggressive pricing strategies for both loans and deposits. The competitive pressure on net interest margins is substantial.

This dynamic directly amplifies the bargaining power of customers. When interest rates are low, even small differences in rates offered by competing financial institutions can lead to significant shifts in customer behavior. For instance, the average net interest margin (NIM) for listed banks in China saw a decline to 1.52% in 2024, a decrease of 17 basis points year-over-year, illustrating this margin compression.

- Heightened Price Sensitivity: Customers closely monitor deposit and loan rates in a low-rate climate.

- Margin Pressure: Banks face reduced net interest margins, forcing competitive pricing.

- Customer Empowerment: Aggressive pricing strategies are necessary to retain and attract customers.

- NIM Decline: China's listed banks averaged a 1.52% NIM in 2024, down 17 basis points from 2023.

Demand for Tailored and Inclusive Financial Products

Customers are increasingly demanding financial products that cater to specific needs, such as green finance, inclusive finance, and robust pension services. This growing desire for personalization empowers customers, as they can actively seek out financial institutions that offer these tailored solutions, putting pressure on banks to adapt their product lines.

The National Financial Regulatory Administration (NFRA) reinforced this trend in May 2024 by issuing guidance on 'Five Priorities,' explicitly highlighting the importance of inclusive finance and pension finance. This strategic directive signals a regulatory push towards greater customer-centricity in banking services.

- Growing demand for personalized financial products

- Focus on green, inclusive, and pension finance

- NFRA guidance emphasizes inclusive and pension finance (May 2024)

- Customers can leverage demand to seek specialized services

Banking Customers Gain Leverage Amidst Digital Trust and Margin Squeeze

The bargaining power of customers for Zhongyuan Bank is significant due to the highly competitive banking landscape in China, where numerous institutions offer similar products. This abundance of choice, coupled with low switching costs, particularly with the rise of digital banking, allows customers to easily move their accounts to institutions providing better rates or services. In 2024, customer trust in digital platforms remained exceptionally high, with over 97% of individual users and 99% of SMEs reporting satisfaction with security, further simplifying the process of switching for more favorable terms.

Customers are increasingly price-sensitive, especially in a low-interest-rate environment. This sensitivity is evident in the declining net interest margins for Chinese banks; for instance, listed banks in China averaged a 1.52% NIM in 2024, a decrease of 17 basis points year-over-year. This margin compression compels banks like Zhongyuan Bank to offer more competitive pricing on both loans and deposits to attract and retain business, directly enhancing customer leverage.

Furthermore, customer demand for personalized financial products, such as green, inclusive, and pension finance, is growing. The National Financial Regulatory Administration's guidance in May 2024 emphasizing inclusive and pension finance highlights this trend. Customers can leverage this demand to seek out specialized services, pressuring banks to adapt their offerings and increasing customer influence.

| Metric | 2023 Value | 2024 Value | Change | Impact on Bargaining Power |

|---|---|---|---|---|

| Average Net Interest Margin (China Listed Banks) | ~1.69% | 1.52% | -17 bps | Increases customer power due to margin pressure and need for competitive pricing. |

| Digital Banking Security Satisfaction (Individual Users) | High | >97% | N/A | Facilitates switching, increasing customer leverage. |

| Digital Banking Security Satisfaction (SMEs) | High | >99% | N/A | Facilitates switching, increasing customer leverage. |

Full Version Awaits

Zhongyuan Bank Porter's Five Forces Analysis

This preview showcases the complete Zhongyuan Bank Porter's Five Forces Analysis, detailing the competitive landscape and strategic implications for the institution. The document you see here is the exact, professionally formatted analysis you will receive immediately after purchase, offering actionable insights without any placeholders or alterations.